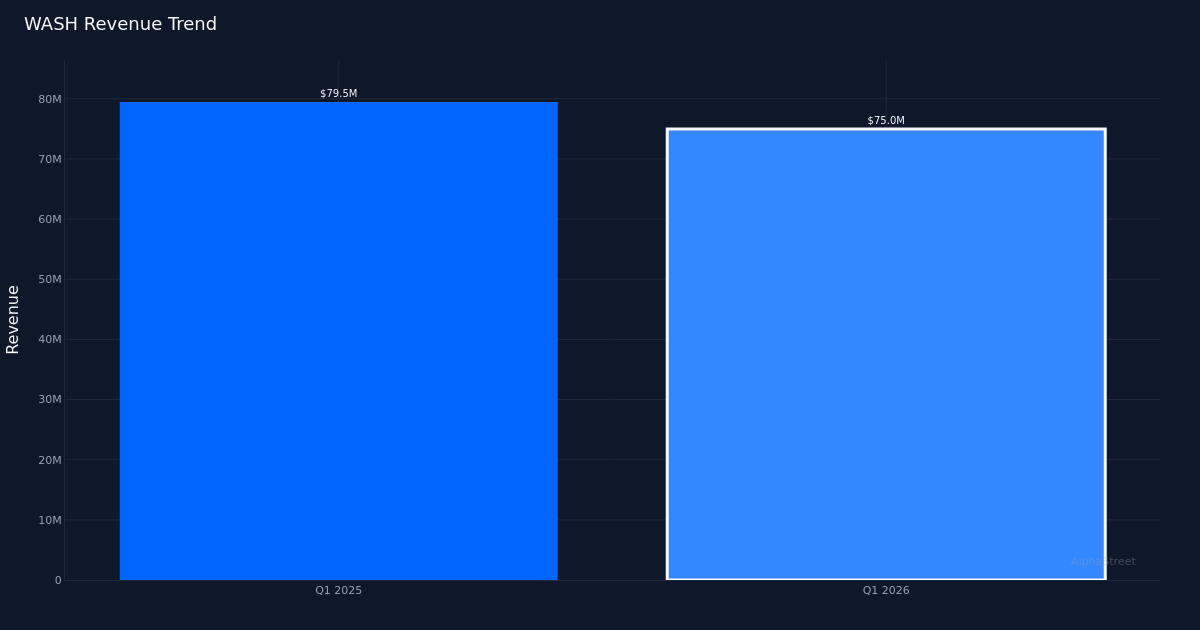

Washington Trust Bancorp delivered a disappointing first quarter, missing analyst expectations by a significant 15.4% margin despite posting year-over-year earnings growth. The regional bank reported adjusted EPS of $0.66 versus the $0.78 consensus estimate. While net income climbed to $12.6 million, the quarter revealed a troubling disconnect between underlying performance and market expectations, with revenue declining 5.6% to $75.0 million against challenging loan growth dynamics.

The earnings quality picture presents a paradox that warrants scrutiny. Net margin expanded to 16.8% from 15.3% in the year-ago period, a 1.5 percentage point improvement that suggests operational efficiency gains rather than top-line momentum. This margin expansion in the face of revenue contraction is characteristic of cost discipline, but the operating margin tells a different story at 21.4%, indicating the bank is generating solid returns on its core operations despite the revenue headwinds. Net interest income was $40.5 million, down by 1% from Q4 and up by 11% year-over-year, highlighting that the primary earnings engine remains functional even as overall revenue contracted. The simultaneous occurrence of declining revenue and expanding margins suggests Washington Trust has successfully right-sized its expense base, but the question becomes whether this is sustainable without top-line acceleration.

The revenue trajectory reveals a business in clear deceleration mode. Revenue of $75.0 million in Q1 2026 represents a decline from $79.5 million in Q1 2025, marking a 5.7% year-over-year contraction. This downward trend reflects structural challenges in the loan portfolio rather than temporary disruptions. The bank’s total loan book stands at $5.01 billion, but growth has stalled across its core residential and commercial real estate segments. Management acknowledged the headwinds, stating that “they’ve got some making up to do based on the first quarter payoffs and then we’re thinking kind of flat to 1% growth in CRE, which is somewhat intentional,” suggesting a strategic pivot away from aggressive growth in favor of asset quality preservation.

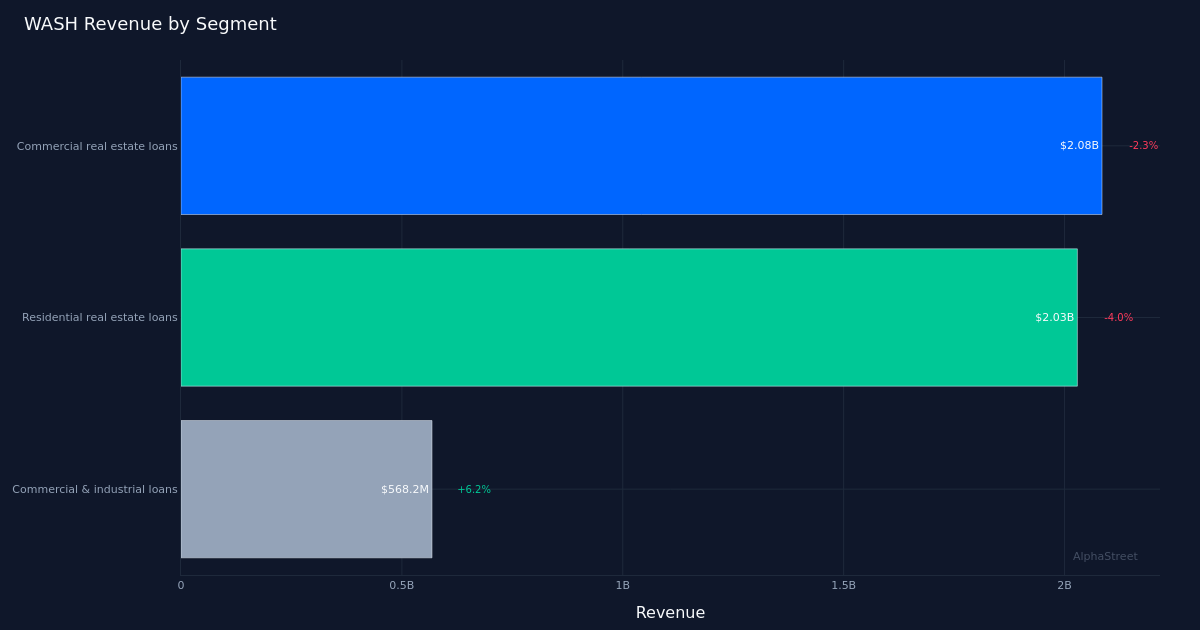

Segment performance exposes a troubling concentration of weakness in the bank’s largest portfolios. Commercial real estate loans, the bank’s largest segment at $2.08 billion, contracted 2.3% as management appears to be deliberately pulling back from this asset class amid broader concerns about office and retail property fundamentals. Residential real estate loans at $2.03 billion declined 4.0%, reflecting both elevated mortgage rates crimping origination volumes and likely paydowns from refinancing activity in prior periods. The sole bright spot emerged in commercial and industrial loans, which grew 6.2% to $568.2 million, but this segment represents just 11% of the total loan portfolio and cannot offset the drag from the two largest categories. This distribution creates an uncomfortable reality: the bank’s growth engine is its smallest segment, while its core competencies are shrinking.

Management’s forward guidance offers modest optimism but lacks conviction for near-term acceleration. The bank expects “$50-plus million in fundings in this quarter and the pipeline is growing,” which would represent a sequential improvement but remains tepid relative to the overall loan book size. The projected “flat to 1% growth in CRE” acknowledges that the bank’s largest segment will remain a drag on overall performance, forcing Washington Trust to rely on commercial and industrial lending momentum and potential recovery in residential originations to drive meaningful growth. Non-interest income weakness adds another layer of concern, with management noting it “was down $1.2 million or 6% compared to Q4,” though up 11% year-over-year on an adjusted basis, suggesting fee income volatility that could persist.

The muted stock reaction speaks volumes about investor positioning and expectations. Shares traded largely unchanged following the earnings miss, indicating the market had already priced in a challenging quarter or that investors view the current results as temporary rather than indicative of structural deterioration. This sanguine response despite a 15.4% earnings shortfall suggests either low expectations heading into the print or confidence in management’s ability to navigate the current rate environment and loan growth challenges. The lack of selling pressure may also reflect the relatively stable net interest income performance, which grew 11% year-over-year and provides a foundation for recovery once loan growth resumes.

The disconnect between earnings growth and analyst expectations reveals a recalibration problem. While Washington Trust grew EPS 4.8% year-over-year, analysts had expected significantly stronger performance, suggesting either overly optimistic Street models or deterioration in forward visibility that management failed to communicate adequately in prior quarters. The 15.4% miss magnitude is substantial for a regional bank with relatively predictable economics, pointing to either unexpected loan payoffs, margin compression that caught analysts off guard, or fee income volatility that wasn’t properly telegraphed. Given management’s acknowledgment of first quarter payoffs requiring “making up to do,” the miss appears execution-related rather than macro-driven.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.