Shares of Campbell Soup Company (NYSE: CPB) were green on Monday. The stock has dropped 25% year-to-date. The food company is slated to report its fourth quarter 2023 earnings results on Thursday, August 31, before market open. Here’s a look at what to expect from the earnings report:

Revenue

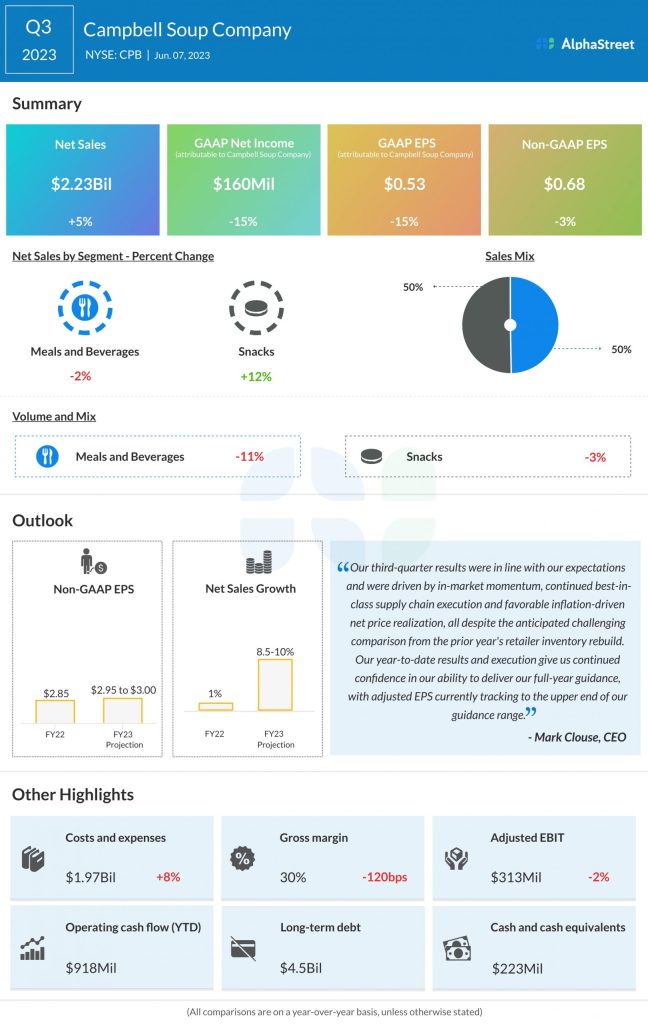

Analysts are projecting revenue of $2.06 billion for the fourth quarter of 2023, which would represent a growth of over 3% from the same period last year. In the third quarter of 2023, net sales rose 5% year-over-year to $2.2 billion.

Earnings

The consensus estimate for EPS in Q4 2023 is $0.50, which compares to EPS of $0.56 reported in the year-ago quarter. In Q3 2023, adjusted EPS fell 3% YoY to $0.68.

Points to note

Sales in the third quarter benefited from inflation-driven net price realization but this was partly offset by a decline in volumes due to elasticities. These trends are likely to continue into the fourth quarter.

The Meals & Beverages segment saw sales decline in Q3 due to lower volumes and higher competition. The soup business saw sales drop by 11% in the third quarter. On the other hand, the Snacks business witnessed strong growth, driven by gains in cookies, crackers, salty snacks and pretzels. Brands like Goldfish, Lance, Kettle, and Cape Cod performed well during the quarter. Volume declines offset price realization gains in both segments.

Campbell continues to deal with higher cost inflation and increased expenses. Despite benefits from price realization and supply chain productivity improvements, these could take a toll on margins. In Q3, gross profit margin dipped to 30% from 31.2% in the year-ago period.

For the full year of 2023, Campbell expects net sales to increase 8.5-10% year-over-year, on a reported and organic basis. Adjusted EPS is expected to be $2.95-3.00.