Shares of the Home Depot (NYSE: HD) were down over 1% on Tuesday. The stock has gained 18% over the past three months. The home improvement retailer is scheduled to report its fourth quarter 2023 earnings results on Tuesday, February 20, before market open. Here’s a look at what to expect from the earnings report:

Revenue

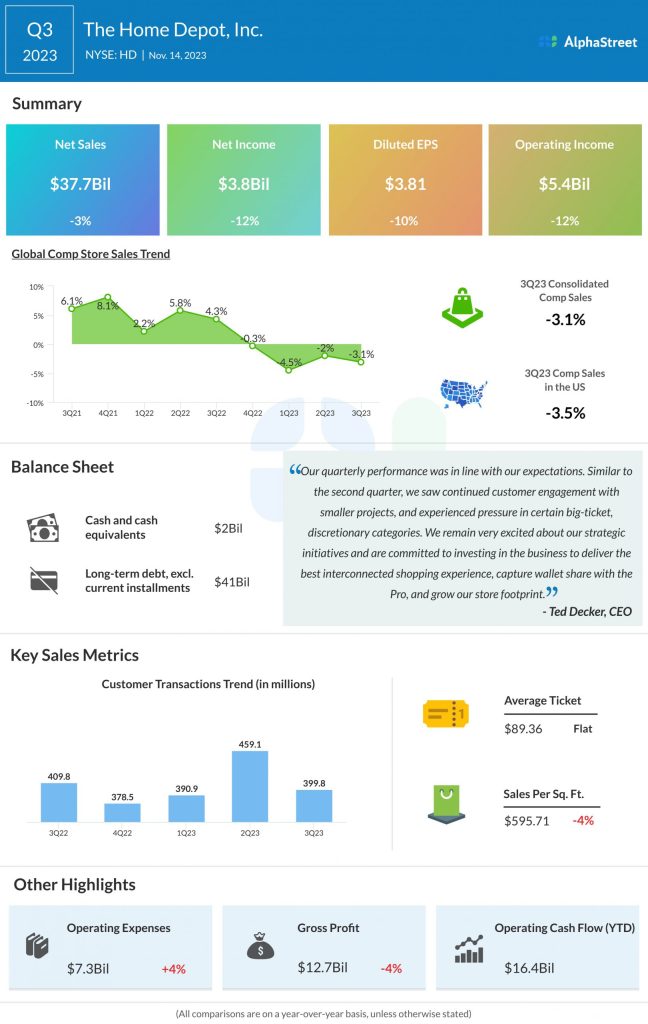

Analysts are projecting revenues of $34.6 billion for the fourth quarter of 2023, which would imply a decrease of 3% from the same quarter a year ago. In the third quarter of 2023, revenues declined 3% year-over-year to $37.7 billion.

Earnings

The consensus estimate for EPS in Q4 2023 is $2.76, which compares to EPS of $3.30 in the prior-year quarter. In Q3 2023, EPS fell 10% to $2.81.

Points to note

Home Depot has been facing challenges such as slow demand in big-ticket, discretionary categories, and lumber and copper wire deflation. Customers have been opting for smaller projects over bigger renovations due to a tough economic environment. Despite this, the company has remained relatively resilient, providing optimism over its prospects.

The Pro customer segment has remained steady, outperforming the DIY customer segment. Although Pro backlogs appear to be lower than last year’s levels, they are still reportedly healthy and higher compared to historical norms. The stability in this segment is likely to benefit the results in the fourth quarter.

The investments that Home Depot is making in order to improve its product assortment, fulfillment and operations are also expected to benefit the company. Its efforts to enhance its digital capabilities are also expected to prove beneficial. Home Depot sees significant opportunity in the Pro market and it has been taking several steps to improve the shopping experience of its Pro customers. All this is expected to have a positive impact on its business performance.