Shares of Alaska Air Group Inc. (NYSE: ALK) stayed green on Tuesday. The stock has dropped 19% year-to-date. The airline company is scheduled to report its third quarter 2023 earnings results on Thursday, October 19, before market open. Here’s a look at what to expect from the earnings report:

Revenue

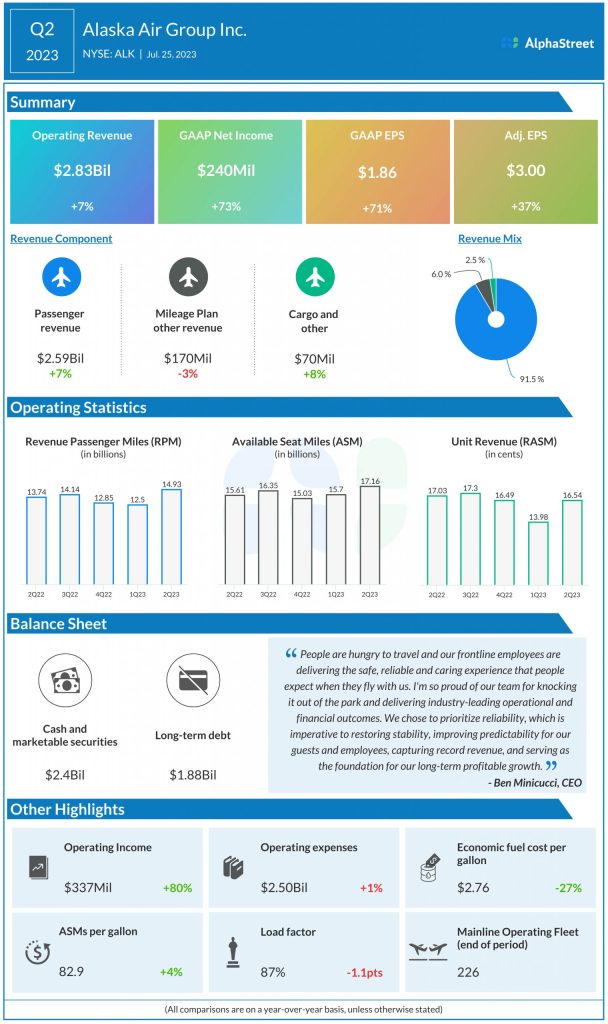

Alaska expects total revenue for Q3 2023 to increase 1-2% from the same period a year ago. Analysts are projecting revenue of $2.87 billion for the third quarter, which would reflect a year-over-year growth of 1.7%. In Q2 2023, operating revenues increased 7% YoY to $2.83 billion.

Earnings

The consensus estimate is for EPS of $1.86 which would represent a decline of 26% from the prior-year period. In Q2 2023, adjusted EPS was $3.00.

Points to note

Alaska is expected to benefit from the strong demand for travel, as favorable trends continue in leisure travel. Last quarter, the company saw an unprecedented surge in international travel demand. It believes this pent-up demand had the effect of a larger pull from would-be domestic travelers thereby causing a disproportionate impact on realized domestic fares which could affect the top line performance in Q3.

The airline now expects capacity for the third quarter to be up around 13% from the prior-year period versus its previous outlook for up 10-13%. In Q2, capacity was up 10% YoY. Alaska now expects CASMex to be down 1-2% in Q3 versus the prior expectation of down 0-2%. In Q2, CASMex was up 2% YoY.

A continued increase in fuel prices led Alaska to lower its expectations for adjusted pre-tax margin. The company now expects economic fuel cost per gallon to be approx. $3.15-3.25 versus the previous range of $2.70-2.80. Adjusted pre-tax margin is now expected to be 10-12% versus the prior outlook of 14-16%.