Shares of Dollar Tree, Inc. (NASDAQ: DLTR) were down over 1% on Monday. The stock has gained 34% year-to-date. The discount store chain is scheduled to report its earnings results for the third quarter of 2025 on Wednesday, December 3, before the market opens. Here’s a look at what to expect from the earnings report:

Revenue and earnings forecast

Dollar Tree has guided for adjusted earnings per share in the third quarter of 2025 to be comparable to the same period a year ago. Analysts are estimating earnings of $1.08 per share on revenue of $4.7 billion for Q3 2025. This compares to adjusted EPS of $1.12 and revenue of $7.57 billion reported in Q3 2024. Sales from continuing operations are likely to see growth from the previous year.

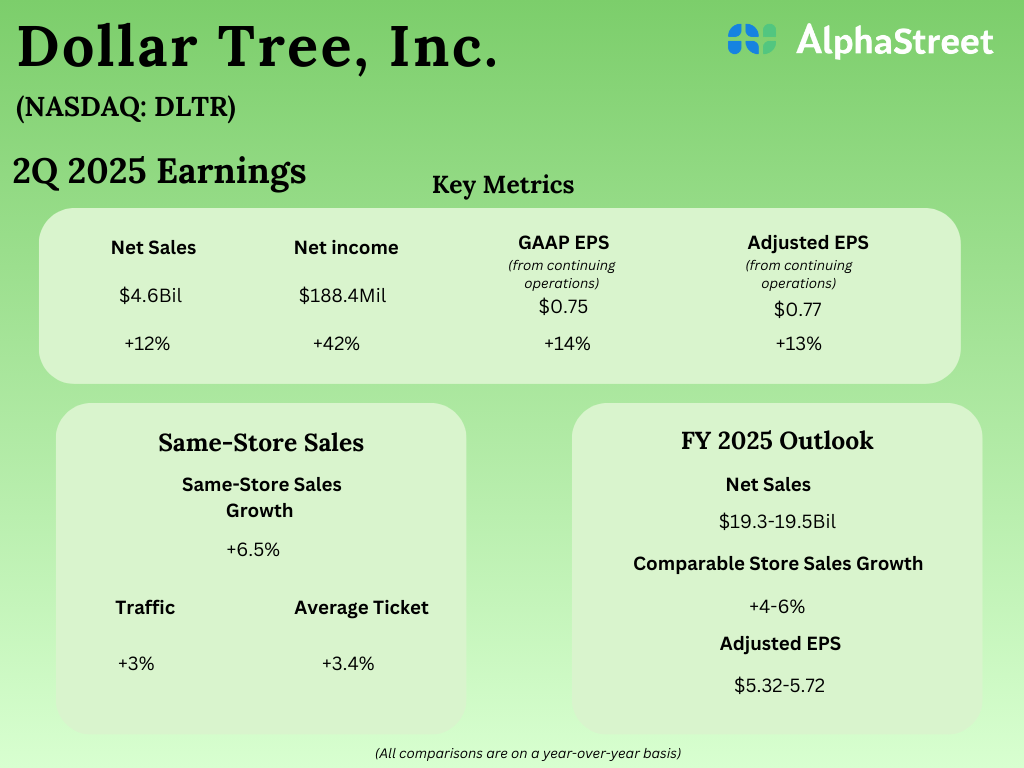

In the second quarter of 2025, net sales from continuing operations increased 12.3% to $4.6 billion and adjusted EPS rose 13.2% to $0.77 on a year-over-year basis.

Points to note

At its Investor Day in October, Dollar Tree said its Q3 2025 quarter-to-date comparable same-store sales growth was approx. 3.8%. In the second quarter, same-store sales grew 6.5%, driven by increases in traffic and average ticket.

The discount retailer is expected to continue to benefit from its expanded assortment and affordable pricing, which continues to bring in customers from all income cohorts. Last quarter, the growth in traffic and ticket was driven substantially by middle and high-income customers.

In addition to the strength in the consumables category, DLTR saw significant growth in the discretionary category last quarter, despite the lack of any major holidays during the period. Discretionary comps were up 6.1% in Q2. This growth was driven by a strong assortment and value. The company also saw margins expand due to the mix shifting from certain low-margin consumable categories.

Dollar Tree’s multi-price strategy, which allows it to offer a large number of products at modest price points, is expected to yield benefits. The company continues to convert more stores to the multi-price format and it anticipates turning approx. 5,000 stores by year-end. The retailer’s efforts in revamping its store fleet through remodels and renovations are expected to improve its fleet productivity.