Shares of The Campbell’s Company (NASDAQ: CPB) were down 1% on Wednesday. The stock has dropped 15% over the past three months. The branded food company is slated to report its earnings results for the third quarter of 2025 on Monday, June 2, before market open. Here’s a look at what to expect from the earnings report:

Revenue

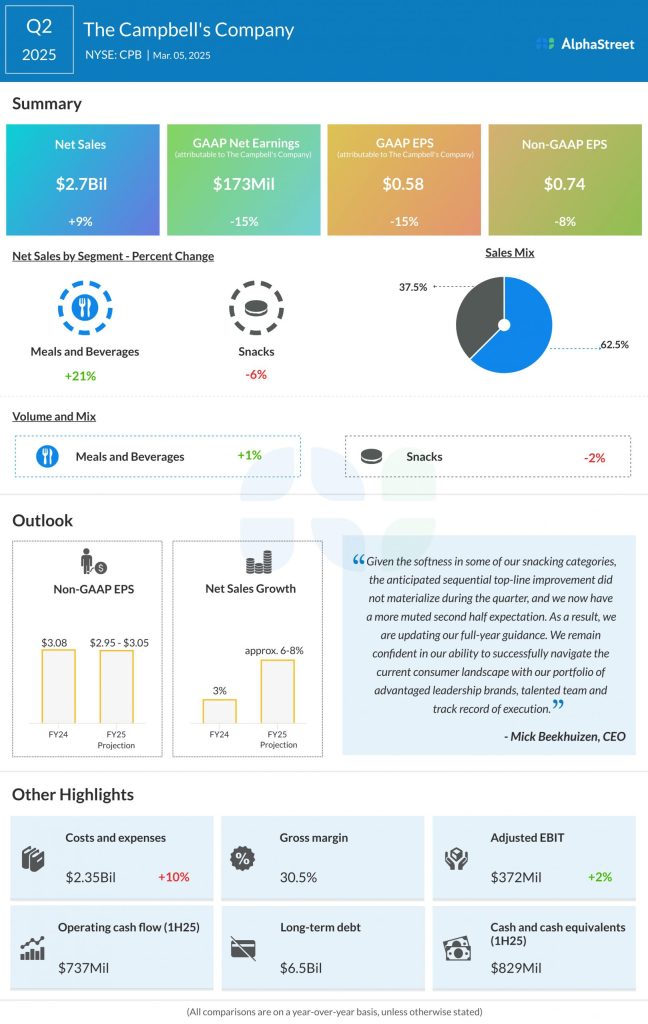

Analysts are projecting revenue of $2.43 billion for Campbell’s in the third quarter of 2025, which indicates a growth of over 2% from the same period a year ago. In the second quarter of 2025, net sales increased 9% year-over-year to $2.7 billion.

Earnings

The consensus estimate for earnings per share in Q3 2025 is $0.66. This compares to adjusted EPS of $0.75 reported in Q3 2024. In Q2 2025, adjusted EPS decreased 8% YoY to $0.74.

Points to note

Campbell’s is expected to benefit from the strength of its brand portfolio, the momentum it is seeing in its Meals & Beverages division, and from the addition of Sovos Brands. Its soup portfolio is anticipated to continue to benefit from the trend of consumers cooking more meals at home, with gains in brands like Chunky and Pacific.

The Rao’s and Prego brands have been performing well and this momentum is expected to continue in the third quarter. While the broth category has been seeing continued growth benefiting from softness in private label, an anticipated recovery in private label during the second half of the year may pressure this growth.

The company continues to see weakness in its Snacks division due to a dynamic consumer environment and tough competition. A weaker-than-expected recovery in its snacking categories led it to lower its outlook for the full year. Margins in this segment decreased in Q2 due to higher promotional investments and supply chain costs. CPB anticipates margins in the Snacks segment to improve sequentially throughout Q3 and Q4 compared to Q2.

Campbell’s is also expected to benefit from the cost savings and productivity initiatives that it has been undertaking to help ease pressure on its bottom line.