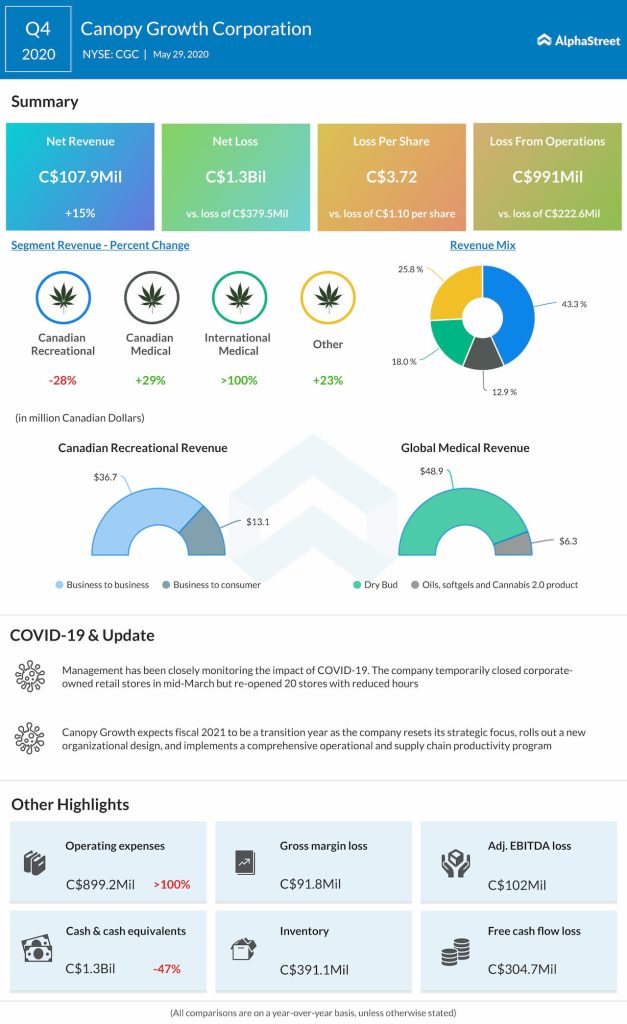

The latest quarterly performance of Canopy Growth Corporation (NYSE: CGC) was nothing short of a disaster, with the cannabis firm incurring a whopping C$1-billion loss in the final months of fiscal 2020. The shareholders are once again left speculating about the future of the company, after the short-lived relief that followed the recent recovery.

To everyone’s surprise, the American cannabis industry witnessed a marked uptick after the COVID-19 outbreak – unlike the other sectors that struggle to stay afloat – due to the inclusion of cannabis products in the ‘essential commodities’ category in several regions. Currently, the company is reopening its corporate-owned stores which were closed early March. But the overall outlook for the business is not very encouraging.

[irp posts=”61607″]

It seems Canopy Growth is suffering due to its unfavorable product mix, though the aggressive product launches in recent months have brightened hopes of a recovery. Still, the company’s extensive vape portfolio calls for caution.

In an unusually candid statement, CEO David Klein told analysts during the earnings conference call this week, “The company became less agile, siloed, and was burning too much cash. We’ve already taken decisive actions to bring some much-needed focus. We designed a new operating model that will focus on the consumer and will increase our speed and agility as an organization.”

Cash Burn

The capital spending strategy of the weed producer has often raised questions about the sustainability of the model, though the executives claim to have reduced spending and streamlined operations in certain markets, as part of shifting to an “asset-light” model. If the company continues the cash burn at the current rate, it might face a liquidity crisis by year-end.

It also shows that Klein is still putting things in order after taking over the reins from Bruce Linton, who had an unceremonious exit last year after being blamed for the company’s poor financial performance. Yet, since it is the first earnings report after the new CEO took charge, it won’t be fair to judge him solely on the basis of the latest performance. Meanwhile, an encouraging aspect of the balance sheet is the moderate debt.

Q4 Revenue up 15%

Revenues grew about 15% during the three-month period, as a double-digit fall in the core recreational business segment was more than offset by growth in the other segments, but missed expectations by a wide margin. On the other hand, elevated operating expenses continued to weigh on margins, and the company registered a wider loss of C$3.72 per share for the quarter.

The results indicate that the efforts to reorganize the business by exiting non-performing markets and scaling down production are yet to yield the desired results. The company is all set to hold a virtual investor meeting on June 22 to provide more updates.

“Simply put, we missed opportunities. But the good news is we are making changes to our operations and supply chain, some of which have already been announced. But for now, let me reassure you we are focused on improving our agility and cost structure so that we can improve execution across our supply chain and deliver on the margin commitments to our shareholders.”

Mike Lee, chief financial officer of Canopy Growth

Definitely, this is not the right time to buy Canopy Growth because there is no clarity as to where the stock is headed. Despite the recent fall, the stock looks quite expensive relative to earnings. The current target price points to a further contraction in market value in the coming months.

Investing in CGC

However, the optimists among investors can take a cue from the goals set by the management to turn profitable in the near term, while suspending the full-year guidance issued earlier. Also, the sector as a whole performed better than Canopy Growth in the most recent quarter, which can be inspiring to those looking for long-term investment.

[irp posts=”54384″]

The recovery of Canopy Growth’s shares, after slipping to a multi-year low in March, was hampered by the dismal fourth-quarter performance. They closed the last session down 20% and continued to lose early Monday before business started. The stock has lost 14% since the beginning of the year and 57% in the past twelve months amid the pandemic-related selloff.