Shares of Home Depot (NYSE: HD) were up over 1% on Wednesday. The stock has gained 15% over the past three months. The company delivered better-than-expected earnings results for the third quarter of 2024 and raised its guidance for the full year on the back of hurricane-related demand. However, larger-scale projects still remain pressured by macroeconomic uncertainty. Here are a few points of note on the Q3 performance:

Revenue and profits

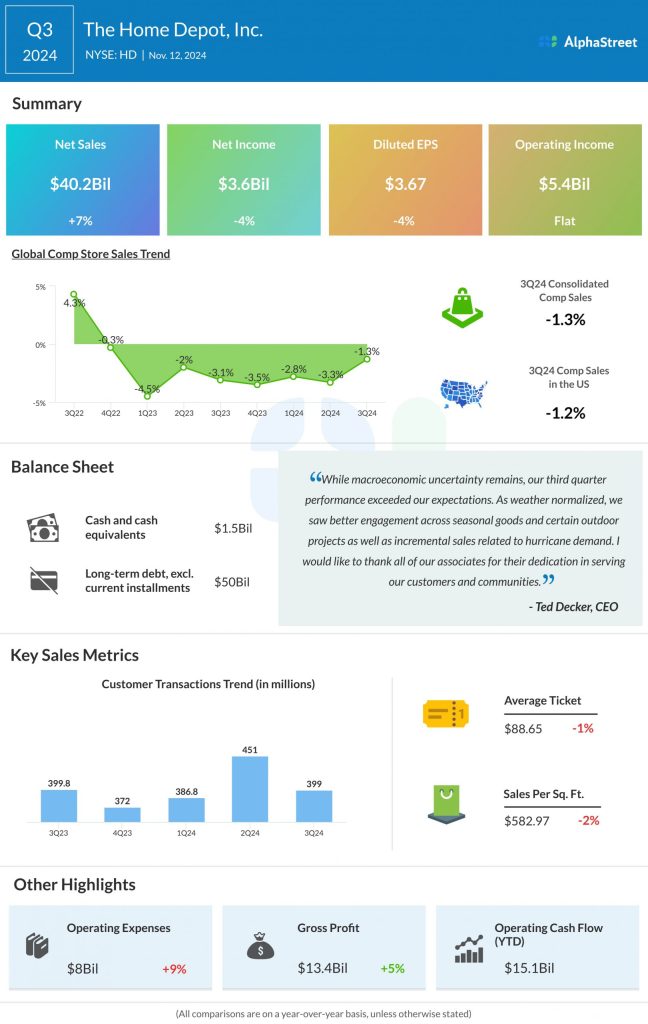

Home Depot generated sales of $40.2 billion in the third quarter of 2024, up 6.6% from the same period a year ago. The top line surpassed estimates. The company’s performance varied heavily across its divisions as some of its regions were impacted by storms while others benefited from favorable weather, which drove demand for seasonal goods and outdoor projects.

Comparable sales decreased 1.3% overall, and in the US, they fell 1.2%. Comps remained negative through August and September before turning positive in October. The shift in comps was mainly driven by hurricane-related sales, which amounted to around $200 million.

HD’s GAAP earnings decreased approx. 4% YoY to $3.67 per share in Q3 while adjusted EPS dropped around 2% to $3.78. Despite the decline, the bottom line exceeded expectations.

Weakness in larger projects

Home Depot continued to see softness in large-scale remodeling projects during the third quarter, due to higher interest rates and macroeconomic uncertainty. Comp transactions were down 0.6% while comp average ticket was down 0.8% in Q3. Big-ticket comp transactions, or those over $1,000, fell 6.8% YoY. Demand for larger discretionary projects such as kitchen and bath remodels remained soft during the quarter.

Pro Ecosystem

During the third quarter, sales in the professional, or Pro, customer category remained positive, surpassing the do-it-yourself, or DIY, customer category. HD is making progress on developing its Pro Ecosystem capabilities, which are focused on Pros working on large, complex projects. The Pro Ecosystem is now available in 17 US markets. The company continues to invest in improving its on-shelf availability as well as its processes and systems to help drive a seamless customer experience for its Pro customers.

The acquisition of SRS provides Home Depot the opportunity to expand sales to specialty trade Pro customers, who require specialized capabilities for their projects. This acquisition also provides cross-sale opportunities for the home improvement retailer as it brings SRS’ unique products under its umbrella. SRS is on track to contribute $6.4 billion in sales for fiscal year 2024.

Raised guidance

Home Depot raised its guidance for fiscal year 2024 based on its performance in Q3 and incremental hurricane-related sales. The company now expects sales to increase approx. 4% and comps to decline approx. 2.5% in FY2024. GAAP EPS is expected to decrease around 2% while adjusted EPS is expected to decline around 1%.

The company’s previous expectations were for sales growth of 2.5-3.5%, comps decline of 3-4%, GAAP EPS decline of 2-4% and adjusted EPS decline of 1-3%.