Shares of The Estée Lauder Companies Inc. (NYSE: EL) were up over 4% on Monday. The stock has dropped 9% over the past one month. The beauty giant has been facing several operating headwinds which led to a disappointing performance in its most recent quarter as well as a bleak outlook for the upcoming one. Here’s a look at how the company is planning on tackling these challenges:

Drivers of lower sales and profits

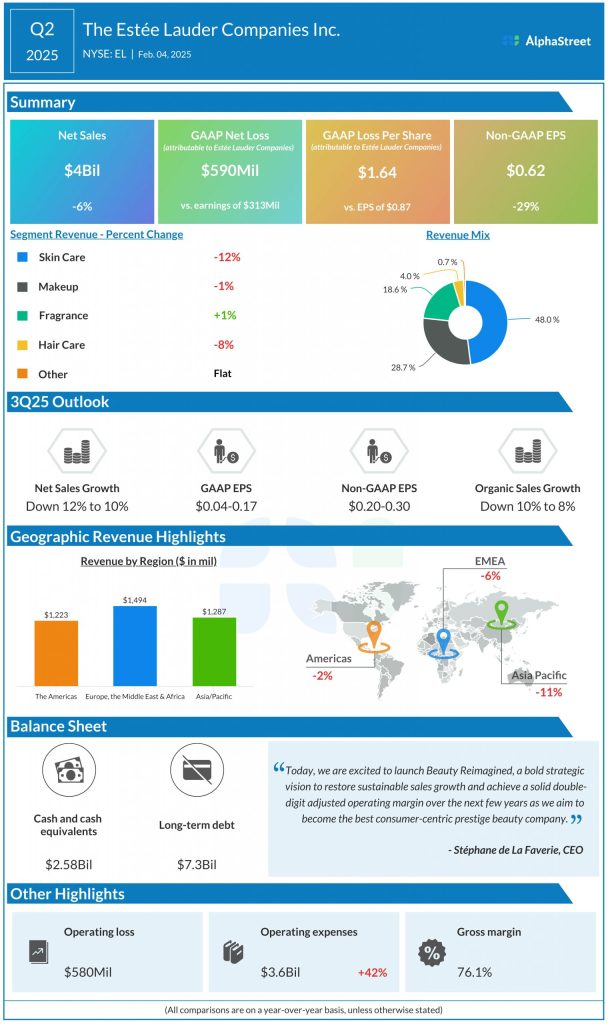

In the second quarter of 2025, Estee Lauder saw sales decline 6% year-over-year to $4 billion on a reported and organic basis. Adjusted earnings per share fell 29% YoY to $0.62.

During the quarter, the company saw sales decrease across all its product categories, barring Fragrance, and across all its geographic regions. EL’s business performance was mainly impacted by headwinds in the Asia travel retail business and weak consumer sentiment in China.

The subdued consumer sentiment in China took a heavy toll on the prestige beauty industry, and given its strong share in the prestige beauty market, EL took a hard hit from this trend. The company’s focus on fewer markets and channels prevented it from benefiting from the strength in prestige beauty around the world, particularly North America. Its failure to pursue higher growth opportunities and attract new customers coupled with slower innovation and lower sales in high-margin areas negatively impacted the business.

Beauty Reimagined plan

Through its Beauty Reimagined initiative, Estee Lauder aims to restore sales growth and boost margins. Under this initiative, the company plans to expand its portfolio across channels, markets and price tiers within prestige beauty that are attractive to consumers and have high growth potential.

In terms of geography, EL sees opportunity for expansion in the US, UK, and emerging markets and by channel, it sees potential for diversification across the travel retail channel in Western markets as well as online platforms, specialty, and pharmacies in Europe.

The company is focusing on product innovation in certain sub-categories where there is high demand. It sees opportunities for its brands to enter or expand in sub-categories such as body within Skin Care and multi-benefit lip products within Makeup. It is also working on restructuring its price tiers in order to roll out products at price points that will attract new customers.

In addition, EL plans to increase its advertising, drive efficiencies through its Profit Recovery and Growth Plan (PRGP), and simplify its organization.

Outlook

Estee Lauder anticipates continued pressure on its Asia travel retail business due to weak consumer sentiment in China and Korea. It expects a double-digit decline in sales in its global travel retail business during the second half of fiscal year 2025. At the same time, retail sales trends, excluding travel retail, are anticipated to see a significant improvement in the third quarter of 2025, with an increase in consumer-facing investments.

For the third quarter of 2025, EL expects reported sales to decrease 10-12% and organic sales to decrease 8-10% YoY. GAAP EPS is expected to range between $0.04-0.17, representing a decline of 81-96%. Adjusted EPS is estimated to be $0.20-0.30, representing a decrease of 69-79%.