Adobe Inc. (NASDAQ: ADBE) has contributed significantly to the ongoing digital expansion, offering tools and platforms designed for performing almost every creative task. Through its data-driven business model and continued innovation, the design software maker looks well-positioned to lead the next phase of digital transformation.

Adobe’s stock has been declining since the beginning of the year, extending the weakness experienced in the final weeks of 2021. At present, prospective buyers would be weighing the pros and cons of investing in Adobe ahead of the upcoming earnings. Having lost around 32% since the November peak, the stock has become much cheaper, creating a rare opportunity for those looking for an entry point.

Buy ADBE?

A market leader like Adobe is unlikely to disappoint investors, thanks to its strong balance sheet. The company ended the last fiscal year with a cash balance of $3.8 billion, while maintaining debt at sustainable levels. Experts are of the view that the stock is likely to breach the $650-mark in the next twelve months. Moreover, the company has an impressive capital return program, with more than $13 billion of authority remaining in its share buyback program at the end of 2021.

Read management/analysts’ comments on Adobe’s Q4 earnings

More than a decade after its launch, the adoption of Creative Cloud remains strong. The trend is expected to continue in the coming years, driving significant revenue growth for the company. It is worth noting that subscriptions accounted for more than 90% of total revenues last year. There is more room for expanding market share and growing the subscriber base.

Innovation

The product portfolio has witnessed continued improvement over the years, and the recent launch of Creative Cloud Express is among the latest innovations. It allows mobile users to create and manage multimedia content with ease and is considered a new chapter in creation and collaboration online. The other major additions include Frame.io and Adobe Workfront.

From Adobe’s Q4 2021 earnings conference call:

“We win by creating enduring technology platforms, from Sensei to the Adobe Experience Platform, they are the foundation for product innovation and our industry-leading applications and services. Since transitioning Creative Cloud to a subscription model 10 years ago, we have continued to innovate our business models, building applications, services, and platforms, to bring value to market faster, better serve new customers, and leverage new monetization models. It would be impossible to do all this alone.”

Q1 Earnings on Tap

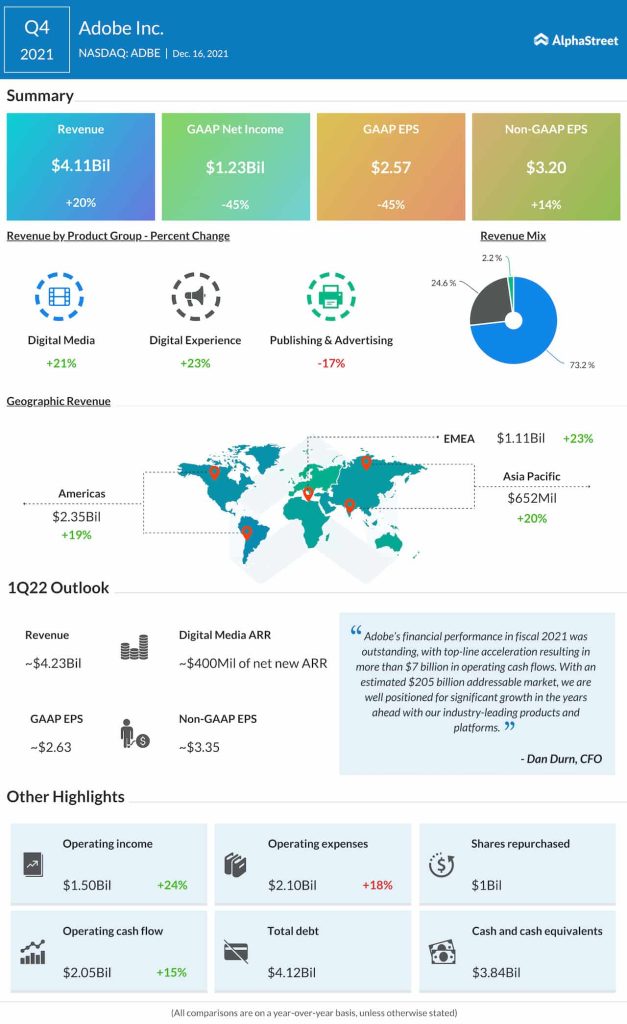

In the final three months of fiscal 2021, Adobe’s net profit increased 14% year-over-year to $3.20 per share and matched analysts’ forecast. Quarterly earnings have topped expectations consistently over the past several years. At $4.11 billion, fourth-quarter revenues are up 20% from the year-ago period, with most of that coming from the core digital media segment.

Infographic: All you need to know about Autodesk’s Q4 results

The company is scheduled to release first-quarter earnings on March 22 after the closing bell, amid expectations for a 6% increase in adjusted earnings to $3.34 per share. Revenue is estimated to have risen to $4.24 billion.

In the past six months, Adobe’s stock lost about 30% and is currently trading below its 52-week average. The stock traded slightly higher on Tuesday afternoon.