Adobe (NASDAQ: ADBE) is like the grandfather in the US software industry, with many interesting stories to its credit. It was launched as a specialized publishing software 1982 and soon after, resisted a takeover attempt by Steve Jobs. Adobe also entered history books becoming the first Silicon Valley member to turn profitable in its first year.

This achievement is of profound importance in this era where technology firms shell out millions on investments, and yet struggle to turn profitable for many years. Of course, some of these firms are projecting high annual revenue growth trends to attract investors like moths to a flame. But ultimately, there comes a point when investors start questioning these firm’s ability to make money.

Also read: $1,000 invested in ADBE 2010 would be worth $14,600 today

Adobe’s capacity to adapt quickly – including the transition from licensed software to a cloud-based subscription model – shows the software-as-a-service firm has one among the best management in Silicon Valley. Since Shantanu Narayen took over as the CEO of the firm in 2007, the stock has jumped from $40 to $400 on a relatively consistent track.

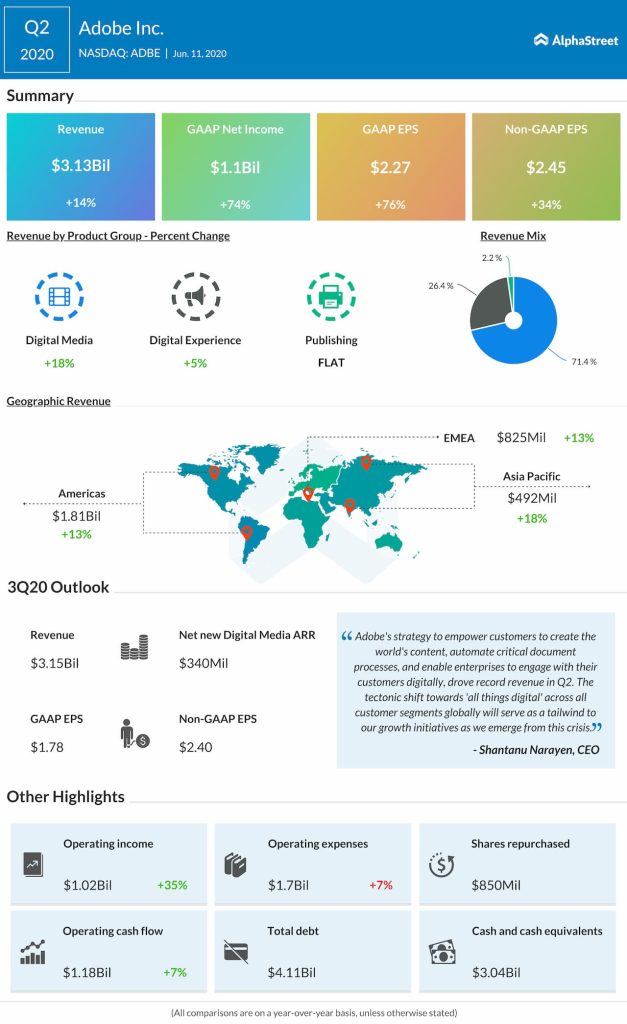

When Adobe reported second-quarter earnings on Thursday, it was a mixed bag. Post-earnings stock movement reflected this as investors were confused about how to play the stock, given SaaS companies were generally benefited by the global lockdowns.

Related: Adobe Q2 2020 Earnings Call Transcript

What happened in Q2?

Adobe also experienced tailwinds from the increased digitization driven by the pandemic, which is evident from the strong growth in contract revenues during the quarter. More importantly, annual recurring revenue from its largest segment – Digital Media – came in at $9.17 billion, better than analysts’ expectation of $9.11 billion. This is a clear indication that the San Jose, California-based firm’s ability to generate revenues from subscriptions is built on strong fundamentals.

Meanwhile, the revenue miss that worried investors was driven by Adobe’s decision to wind down its transaction business. Though it was under consideration for some time, it was fast-tracked during the quarter to streamline resource allocation during the lockdown period. In the words of CEO Narayen:

“It was the transaction business, which is very resource-intensive and that one we had always signaled that we were going to be reducing that business, but we certainly used pandemic as a catalyst to say let’s make a change right now, so we can double down our resources on what really represent durable, long-term opportunities.”

Eliminating the Advertising Cloud

transaction-driven offerings has pumped up the bottom-line by expanding the

overall margin. The transaction business was a low-margin unit that has been

weighing heavily on the bottom-line so far.

So why is the EPS outlook for Q3 weaker than Wall Street projection? Well, for one, Q3 has been seasonally Adobe’s weakest quarter. Second, the company is expected to get back on track with hiring and other marketing activities with this quarter, which should increase the operational expenses as compared to the pandemic period. Apart from these, small and medium businesses are expected to take longer to recover from the impact of COVID-19, and that is also apparently factored into the outlook. Narayen said during the recent earnings conference call:

“I think we’re factoring in normal seasonality. We’re not assuming that things will get better as it relates to the small and medium business. But overall, whether it’s the Document Cloud or the Creative Cloud, we continue to feel good.“

Valuation concerns

Of course one should not forget the valuation. With a 16.5% enterprise value-to-sales ratio and comparatively high PE ratio, investors may be put off by the slow top-line growth rates. It’s quite tempting to go for peers such as Splunk (NASDAQ: SPLK) or Okta (NASDAQ: OKTA), which has been generating higher annual growth rates.

However, Adobe’s ability to grow profits consistently will stand above these stocks to value investors. Remember that the company enjoys abundant brand loyalty among multimedia professionals around the world, despite the onslaught of many new competitors over the past few years. Adobe’s line of products including Photoshop, Illustrator, Lightroom, Premiere Pro and After Effects have enjoyed “Should Have” tags for longer periods than most software.

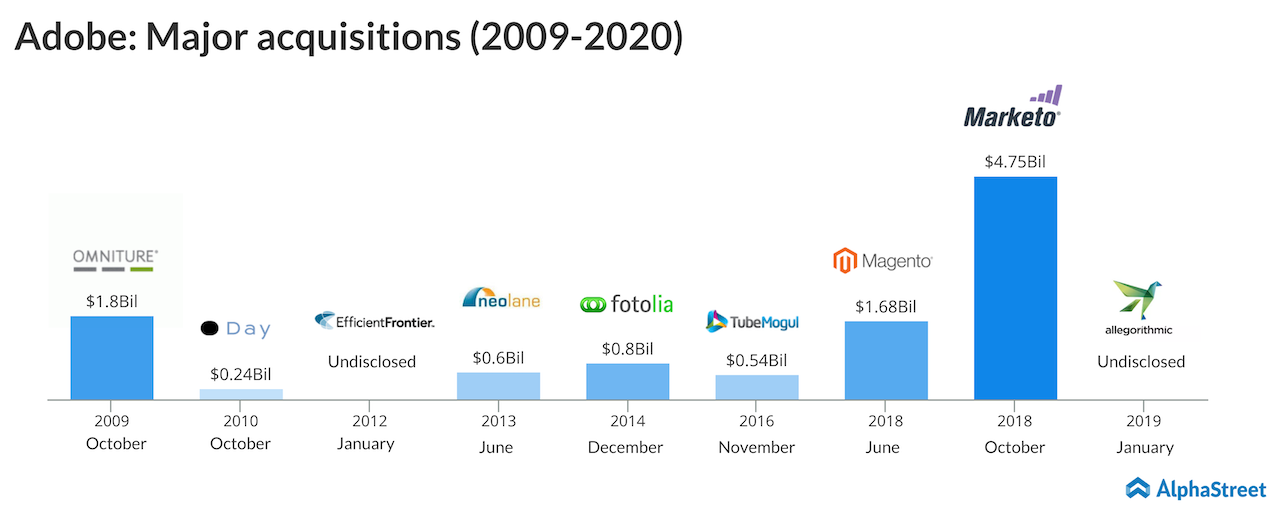

One should also not forget that the firm has been highly active in the acquisition and divestment space. It has acquired over 50 companies in the past 30 years, bringing under its umbrella products and services that could add value to its line up; and more importantly, quash potential rivals.

These reasons make it a darling among long-term investors, even in the current valuations.

____

For more insights about Adobe, read its latest earnings transcript here.