Of late, Applied Materials, Inc. (NASDAQ: AMAT) has been focusing its strategy and investments on advanced technology for growing capabilities in areas like the Internet of Things and artificial intelligence. The semiconductor technology company effectively navigated the recent market slump aided by stable demand from the automotive, communications, and IoT industries.

In recent months, Applied Materials’ stock maintained a steady uptrend and stayed above its long-term average. It has gained 54% since the beginning of the year and looks on track to breach the all-time highs of last year. AMAT got a fresh boost after last week’s earnings report as the market responded positively to the better-than-expected third-quarter results. The stock has mostly outperformed the S&P 500 index this year.

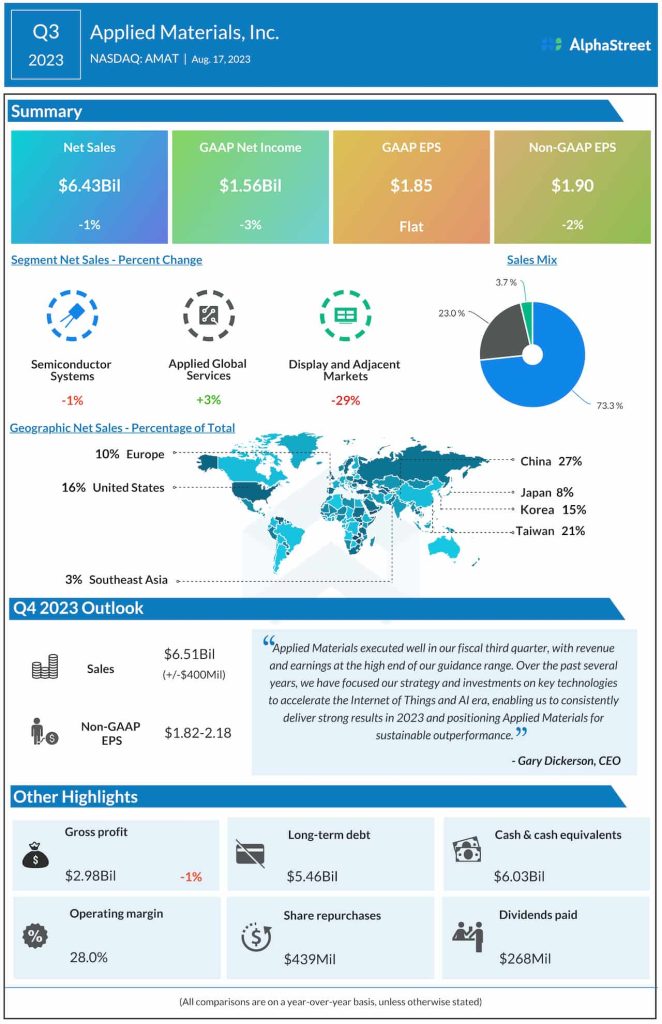

Outlook

The continued slowdown in the PC and smartphone markets would remain a drag on the broad semiconductor industry in the near term. Some of the challenges that drove the industry into a crisis last year — disruption caused by geopolitical tensions and COVID-driven demand slowdown — have continued this year, but the long-term outlook on the sector looks bright. In the near term, growth will be driven mainly by growing chip demand in areas like communications, IoT, and automotive.

Applied Materials CEO Gary Dickerson said at the Q3 earnings call, “We view IoT and AI computing as two sides of the same coin. At the edge, consumer devices, vehicles, buildings, factories, and infrastructure are all getting smarter and more capable. Our customers that serve these IoT, Communications, Auto, Power, and Sensors markets or ICAPS are growing and represent the largest portion of wafer fab equipment sales in 2023. Increasingly, intelligent Edge devices are fueling an explosion of data generation that can then be then transmitted and combined to create very large datasets for training AI models.”

Key Metrics

In the third quarter, adjusted earnings dropped to $1.90 per share from $1.94 per share in the same period of 2022. Net income, including special items, was $1.56 billion or $1.85 per share in the July quarter, compared to $1.61 billion or $1.85 per share last year. There was a 1.5% decrease in net sales to $6.43 billion during the three-month period, mainly reflecting weakness in the core Semiconductor Systems segment.

The top line and earnings exceeded analysts’ estimates, as they did in each of the trailing four quarters. For the final three months of the fiscal year, the management expects sales of around $6.51 billion, and adjusted EPS between $1.82 and $2.18.

Shares of the company closed the last trading session higher, continuing the post-earnings momentum. The stock is up 8% since the third-quarter report.