Shares of American Express Company (NYSE: AXP) dropped over 3% on Friday after the company delivered mixed results for the second quarter of 2024. Profits beat expectations while revenue came below estimates. The company also raised its earnings guidance for the full year of 2024. Here are the main points from the report:

Earnings beat, revenue miss

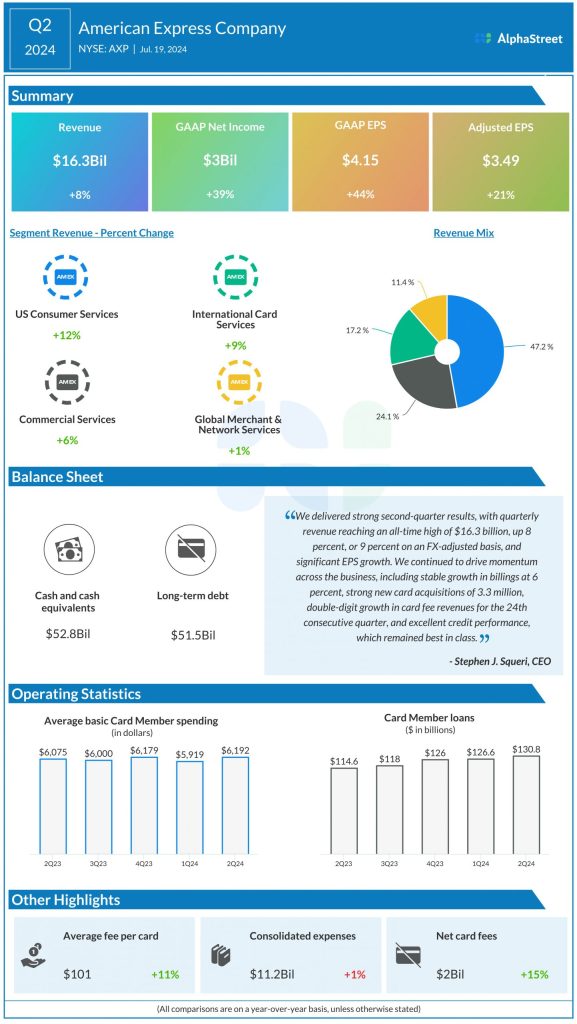

AXP’s consolidated revenues, net of interest expense, increased 8% year-over-year to $16.3 billion in Q2 2024, but missed the estimates of $16.5 billion. The revenue growth was driven mainly by higher net interest income, increased Card Member spending, and strong card fee growth. GAAP EPS increased 44% to $4.15. Adjusted EPS rose 21% to $3.49, beating the consensus target of $3.23.

Business performance

In Q2, AXP’s billed business grew 5% YoY to $388.2 billion. New card acquisitions grew 10% to 3.3 million. Average basic Card Member spending was up 2% while average fee per card rose 11% in the quarter.

Net card fees grew 15% to $2 billion in the second quarter, driven mainly by growth in premium card portfolios. Total non-interest revenues grew 5% to $12.6 billion while net interest income rose 20% to $3.7 billion.

Consolidated expenses rose 1% to $11.3 billion, reflecting higher variable customer engagement costs driven by higher Card Member spending and usage of travel-related benefits, and increased marketing investments. Consolidated provisions for credit losses were $1.3 billion, up 6% from a year ago, due to higher net write-offs.

American Express saw revenue growth across all its segments in Q2. Total revenues, net of interest expense, in the US Consumer Services segment increased 12% YoY to $7.7 billion during the quarter. Commercial Services revenue grew 6% to $3.9 billion. International Card Services revenue rose 9% to $2.8 billion while revenue from Global Merchant and Network Services inched up 1% to $1.8 billion.

Raised guidance

American Express raised its EPS guidance for full-year 2024 to $13.30-13.80 from the prior range of $12.65-13.15. The company continues to expect revenue growth of 9-11% for the year.

“Based on the strong performance of our core business, we believe we can increase our marketing investments by around 15 percent over last year without using any of the transaction gain, while still delivering exceptional earnings results this year. As a result, we have made the decision to drop the entire gain to the bottom line and are raising our full-year EPS guidance to $13.30 – $13.80 from $12.65 – $13.15 previously. We continue to expect revenue growth in line with the guidance range of 9 percent to 11 percent that we set at the beginning of the year.” – Stephen J. Squeri, CEO