Ever since the earnings season kicked off earlier this month, the market has been closely following the events looking for cues on how the pandemic situation is evolving. On Thursday, Apple, Inc. (NASDAQ: AAPL) said that sales were affected by the chip shortage and production delays in the most recent quarter. The gadget giant’s top-line missed estimates for the first time in around four years.

The lower-than-expected sales numbers caused a stock selloff despite strong year-over-year growth. The persistent supply chain disruption is cited as the main reason behind the weak performance, raising concerns that the business world’s recovery from the pandemic — supported by the vaccination drive and market reopening — would take longer than initially estimated.

Read management/analysts’ comments on quarterly reports

Is AAPL a Buy?

But the post-earnings slump should be temporary as the current target price shows Apple’s stock is poised to grow in double-digits. New product launches and widespread 5G adoption are expected to catalyze growth going forward, thereby making the stock more attractive. Also, the recent dip offers an entry point to those looking for long-term engagement.

Beating the Crisis

Meanwhile, statistics show that, in general, the pandemic-induced production disruption has eased in recent months. But Apple is banking on its product upgrades to overcome the unfavorable market conditions – the new versions of the company’s popular gadgets were launched last month amid much fanfare. Besides, it keeps innovating, especially through the effective integration of hardware and software.

Across the board, teams at Apple continue to drive unmatched innovation through the seamlessly integrated hardware, software experience we’ve long prided ourselves on. iOS 15 and iPadOS 15 have created more ways than ever to stay productive, whether choosing Focus to avoid distractions or Quick Note to capture a thought. macOS Monterey offers new ways to connect with friends and family, get more done, and work fluidly across Apple devices.

Tim Cook, chief executive officer of Apple

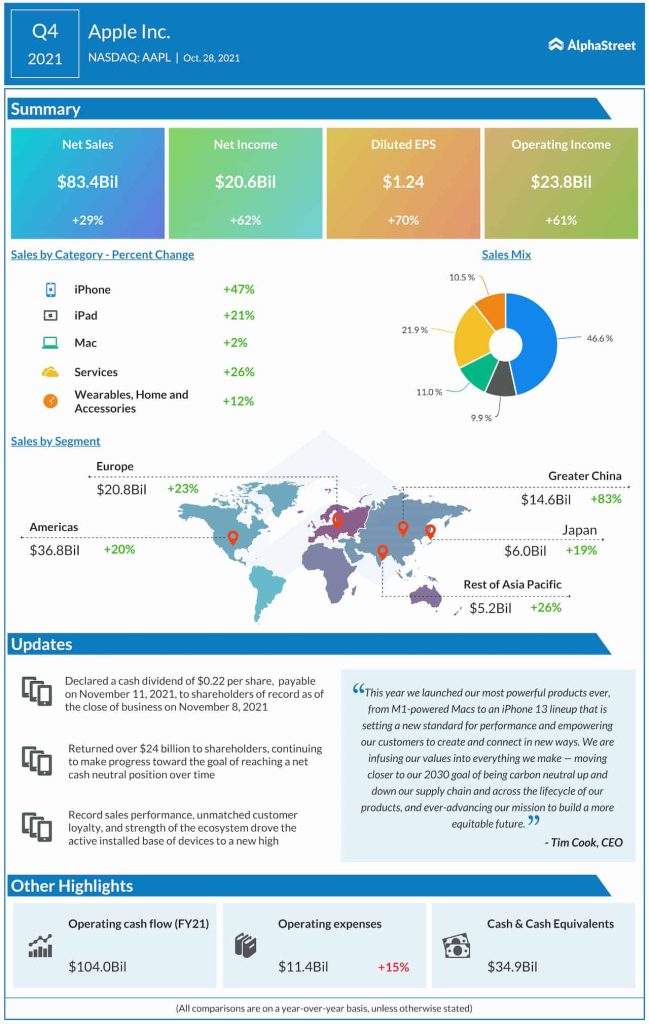

In the fourth quarter, the top-line grew at a weaker-than-expected pace, which is attributable to the continuing supply chain crisis that is estimated to have had a $6-billion impact on the company’s finances. At $83.4 billion, net sales were up 29% year-over-year, with iPhone sales and the services segment growing in double digits. Meanwhile, Mac lagged behind others in terms of sales, registering only 2% growth. Earnings grew 70% to $1.24 per share ad matched estimates. It is worth noting that the bottom-line had topped expectations in every quarter since early 2018.

Road Ahead

The management is optimistic about achieving strong revenue growth in the current quarter, even though supply chain issues are expected to linger and cause a bigger impact than in the September quarter. iPhone 13, the latest version of Apple’s popular smartphone, has been eliciting significant interest and that is going to have a positive effect on sales. Also, the services business, which includes licensing, video subscription, and App Store, is rapidly emerging as a key growth driver.

Alphabet nears $2-trillion valuation. Is the stock a good long-term bet?

On Friday, Apple’s shares opened at $147.21, which is around 3.5% below the previous close. The stock has gained 35% in the past twelve months.