Best Buy Co., Inc. (NYSE: BBY) has stayed largely unaffected by the virus-induced disruption as demand conditions remained stable, though the market witnessed a mass shift from physical stores to online platforms. The electronics store chain has taken advantage of its improved multichannel capabilities and competitive pricing to beat the pandemic woes.

Investing in BBY

After the recent gains, it seems shares of the Minnesota-based retailer do not have much room to grow in the near term. However, the stock looks fairly valued though it gained steadily and outperformed the market most of this year. Those who own BBY may keep holding it, while new investors can consider owning it.

Read management/analysts’ comments on Best Buy’s Q4 report

Besides ramping up its e-commerce capabilities, the company lured customers with low prices that often beat those of bigger rivals like Amazon (NASDAQ: AMZN) and Walmart (NYSE: WMT). Adapting quickly to the change in people’s shopping behavior, Best Buy enhanced its digital presence during the crisis and included facilities like curbside pickup and fast delivery. Such measures helped it perform better than most physical store operators.

Online Sales Surge

In the final months of fiscal 2021, online transactions accounted for 43% of total domestic sales — growing around 90% year-over-year to $6.7 billion. The company’s extensive store network doubled up as fulfillment centers to meet the delivery requirements.

The merchandise category — electronics and home appliances — is such that most customers would want to make purchases in-person rather than visiting e-commerce sites. But, the shift to the digital space is expected to continue beyond COIVD, which calls for continued innovation to attract customers to the stores.

Our research indicates our customers look to Best Buy to serve four shopping needs: inspiration, research, convenience, and support. And customers expect to be able to seamlessly interact with physical and digital channels. We must be ready to serve all of these needs at all times in all channels. We are building all of our experiences around meeting these needs as we move from being a big-box retailer with a strong omnichannel presence to an omnichannel retailer with a large store footprint for support and fulfillment.

Corie Barry, chief executive officer of Best Buy

Q1 Report Due

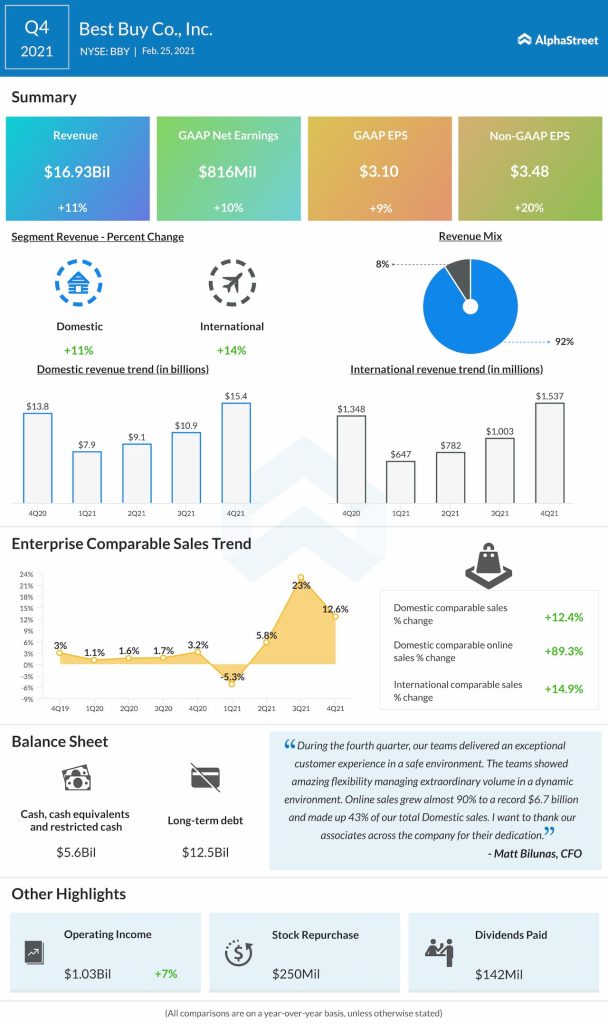

The release of first-quarter earnings is due on May 27 when the company is widely expected to report earnings of $1.31 per share, which is double the prior-year value. Revenues are seen growing 25.30% year-over-year to $10.2 billion. In the fourth quarter, both domestic and international revenues grew and bounced back to the pre-COVID levels, while total comparable-store sales growth eased from the previous quarter. At $17 billion, total revenue was up 11%. That translated into a 20% rise in earnings to $3.48 per share.

Target Corp. Q1 Earnings: Key financials and quarterly highlights

Extending the recent rally, the company’s stock climbed to a record high last week, reversing last month’s dip. It closed the last trading session lower, after gaining 17% since the beginning of the year.