Shares of Chewy, Inc. (NYSE: CHWY) stayed red on Thursday. The stock has dropped 2% over the past three months. The pet products company ended fiscal year 2024 on a strong note with solid results for the fourth quarter and full year. It also made significant progress on its strategic priorities. Chewy expects this momentum to continue in the coming year as well. Here’s a look at its key growth drivers:

Sales and earnings growth

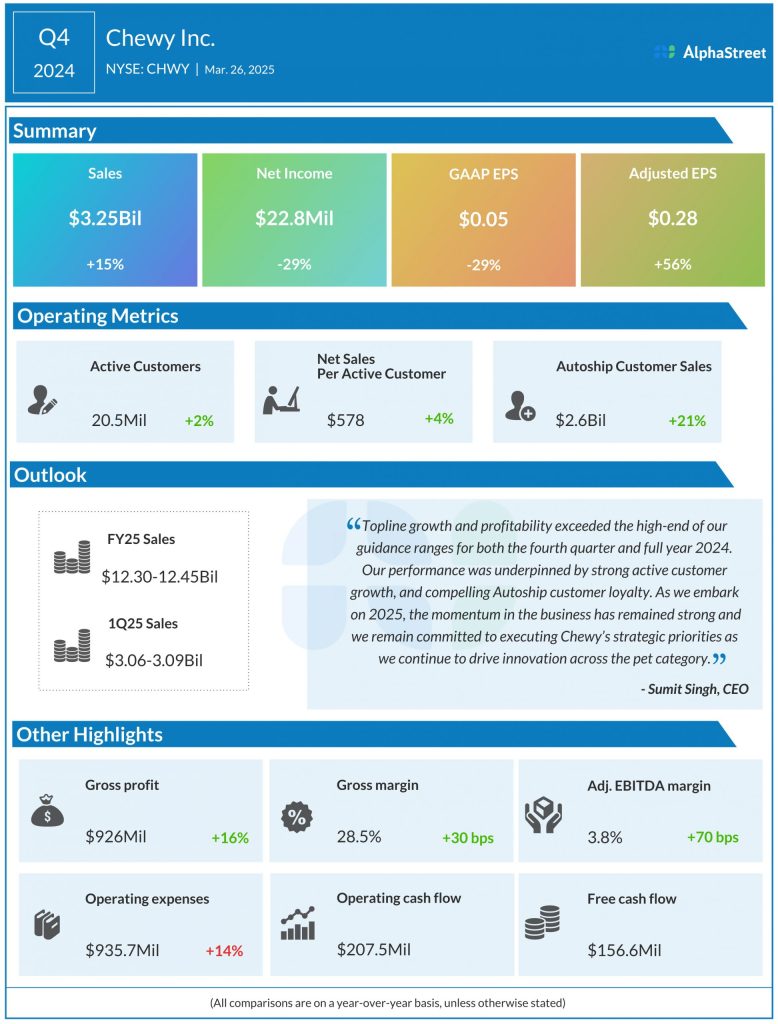

Chewy saw strong growth in sales and earnings for the fourth quarter and full year of 2024. Net sales increased nearly 15% year-over-year to $3.25 billion in Q4, driven by an increase in active customers, a return to growth in hard goods merchandise, and Autoship customer loyalty across the consumables, and health and wellness categories. Full-year 2024 sales grew 6.4% YoY to $11.86 billion.

The top line also benefited from an extra week in fiscal year 2024, which added approx. $227 million in sales to both the quarter and the year. Excluding the impact of the 53rd week, sales grew nearly 7% in Q4 and over 4% in FY2024.

Adjusted earnings per share grew more than 50% YoY for both the quarter and the year, amounting to $0.28 in Q4 2024 and $1.04 in FY2024.

Strong business performance

During the fourth quarter, Chewy saw strong performance across its business with growth in all its key metrics. Autoship customer sales increased 21% YoY to $2.62 billion in Q4. The Autoship program, which accounted for nearly 81% of net sales in the fourth quarter, provides a predictable recurring revenue stream to the company.

Chewy ended the fourth quarter with 20.5 million active customers, reflecting a YoY increase of 2.1%. The company’s efforts in improving its assortment, on-site and mobile app capabilities, and marketing helped drive growth in new customers and reactivations, along with an improvement in gross churn. Chewy believes its active customer growth has reached an inflection point and it expects to deliver growth in this metric in 2025. The company also saw growth in net sales per active customer, which rose 4.1% YoY to $578 in Q4.

Chewy’s gross margin expanded 30 basis points YoY to 28.5% in Q4. This improvement was driven mainly by gains in its sponsored ads business as well as a shift in product mix to premium categories.

CHWY’s network of Chewy Vet Care (CVC) clinics continues to yield benefits in terms of customer acquisition and engagement. The company is seeing rising engagement from both new and existing customers. It opened eight CVC locations, reaching the upper end of its annual target range of 4-8 openings. The pet supplies provider plans to open 8-10 new clinics in FY2025, as it expands its reach over the approx. $25 billion vet services market.

Encouraging outlook

Chewy has provided an encouraging outlook for fiscal year 2025. As the pet industry continues to see normalization, the company believes it is on track to deliver growth and margin expansion in the coming year.

Net sales are expected to range between $3.06-3.09 billion for the first quarter of 2025 and between $12.30-12.45 billion for the full year of 2025. This represents a YoY growth of approx. 6-7% for both the quarter and the year, when adjusted to exclude the impact of the 53rd week in FY2024.

Sales growth is expected to be driven by growth in active customers and net sales per active customer, as well as minimal price inflation. Based on the current environment, the company is optimistic that it will be able to deliver YoY active customer growth in the low single-digit range with the level of net additions broadly consistent throughout the course of the year.

For the first quarter of 2025, Chewy expects adjusted EPS to range between $0.30-0.35.