For Chipotle Mexican Grill, Inc. (NYSE: CMG), fiscal 2023 has been a strong year, thanks to growing customer traffic, higher menu prices, and stable gross margins. The restaurant chain is on a drive to enhance customer experience by ramping up its digital capabilities and optimizing throughput.

CMG is one of the most expensive Wall Street stocks and it has been trading above the long-term average for more than two months. The shares reached an all-time high last month but dropped slightly since then. After the year-long rally, the stock looks overvalued, especially when compared to competitors like McDonald’s. However, the company’s resilient performance amid inflationary pressures, growing market share, and positive outlook justify the price. Moreover, Chipotle has an impressive track record of delivering good shareholder returns.

Buy CMG?

The burrito chain is unlikely to disappoint investors who look for long-term engagement. It targets a specific demographic and enjoys strong customer loyalty, a trend that is expected to continue. The company has launched many initiatives to drive restaurant traffic, such as the introduction of new menu offerings, creative games to connect with guests, and digital makeline, an automated system designed to create bowls and salads.

Chipotle has surpassed 700 Chipotlanes — its mobile order pickup windows — in the most recent quarter and is on track to meet the target of opening 255-285 new restaurants in the near term and 285-315 units next year. Menu prices were hiked recently in response to elevated inflation — the fourth increase in two years — after higher food costs offset the benefits of previous hikes. The company bets on its brand power to attract customers, despite the persistent strain on spending power.

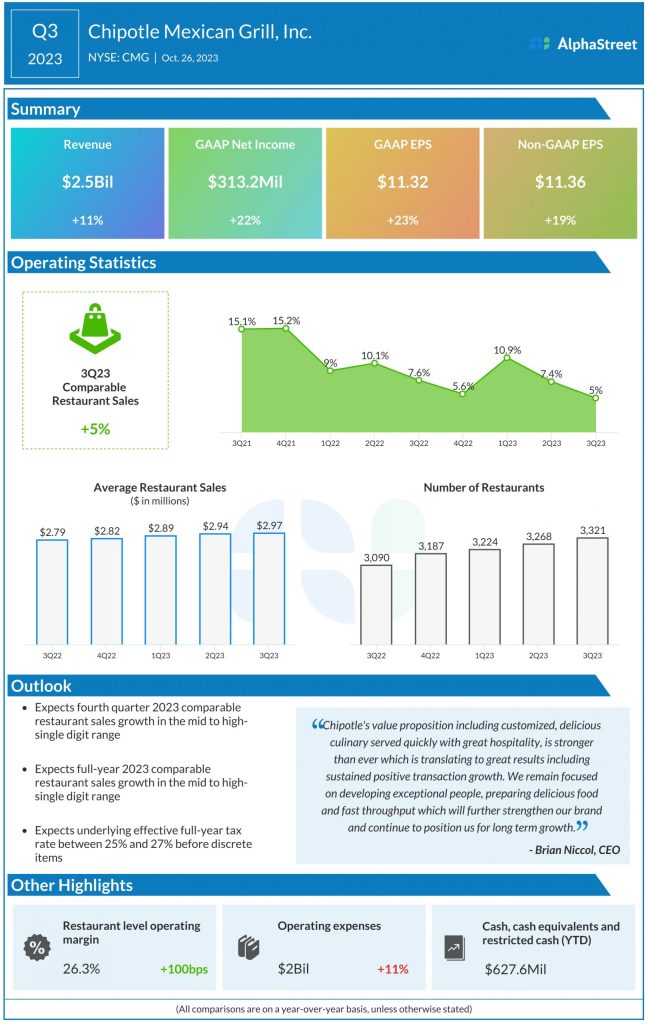

Key Numbers

In recent years, the casual dining specialist’s quarterly earnings beat estimates almost regularly, and the trend continued in the third quarter when revenues also topped expectations. At $2.5 billion, Q3 revenues were up 11% and that translated into a 19% growth in adjusted earnings to $11.36 per share. Comparable restaurant sales growth, a key measure of customer traffic, decelerated for the second straight quarter. The management is looking for mid-to-high single-digit comps growth for the fourth quarter, suggesting a rebound.

“We have two key initiatives that we recently rolled out that we believe will drive further improvement. The first is adjusting the cadence of digital orders to better balance the deployment of labor, eliminating the need to pull a crew member from the front make-line to help the digital make line during peak periods. And the second is a renewed focus on throughput training in our restaurants by bringing back a coaching tool that we had in place prior to the pandemic,” said Chipotle’s CEO Brian Niccol at the Q3 earnings call.

Earnings

Chipotle will be reporting fourth-quarter results on February 6, after the closing bell. It is widely expected to report earnings of $9.68 per share, which represents a 17% year-over-year increase. Revenues are expected to grow 14% annually to $2.48 billion.

The stock traded slightly lower early Wednesday after closing the previous session lower. It has gained a whopping 60% in the past twelve months.