Cisco Systems, Inc. (NASDAQ: CSCO) had a not-so-impressive start to the fiscal year and lost significant market value after it issued below-consensus earnings estimate for the second quarter and warned of a decline in revenues. While the network gear maker is preparing for another quarterly release, analysts are not very optimistic about the top-line performance.

The report is scheduled for release on February 12 at 4:05 pm ET. The revenue estimate for the January-quarter is $11.98 billion, down from $12.4 billion reported in the prior-year period. Meanwhile, earnings are seen growing 4% annually to $0.76 per share, which is above the management’s projection.

Headwinds

Performance of the Infrastructure Platforms segment will likely be hurt by growing competition and unstable demand conditions, though the market’s response to the high-performance Catalyst 9000 and Nexus 9K switching platforms remains positive.

The weak estimates point to a possible stock selloff during the post-earnings trading session. That, however, might not affect the company’s long-term prospects, given its strong fundamentals and sustainable business model. Currently, the majority of the analysts recommend buying the stock.

Emerging Area

The cybersecurity segment is expected to have registered solid growth this time – continuing the recent trend – leveraging the growing demand from enterprise customers. Also, offerings from the AppDynamics and Jasper businesses might contribute to revenues growth, as they did in the previous quarters.

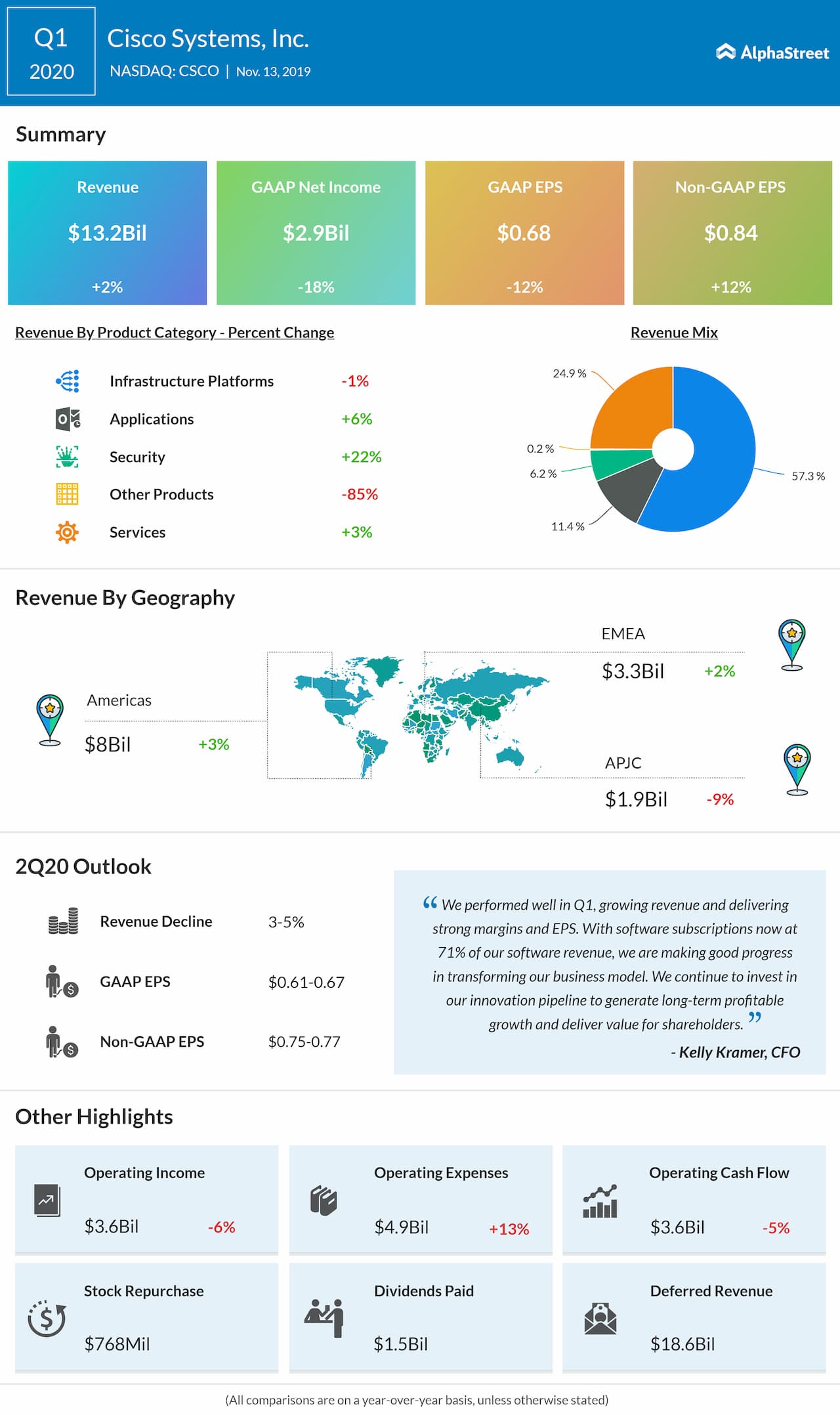

Q1 Results

In the first quarter, the ongoing slowdown in Infrastructure Platforms, Cisco’s core business, restricted revenue growth to 2%. Earnings, adjusted for non-recurring items, rose 12% to $0.84 per share and surpassed the consensus estimate.

Also read: Juniper Networks Q3 2019 Earnings Snapshot

Cisco has been executing its reorganization plan with focus on strategic buyouts as it seeks to transform into a software-led service provider. While retaining the leadership position in its core business, the company is also diversifying into other areas such as cybersecurity and analytics.

Competitors

Analysts’ sentiment for Cisco’s competitor VMWare (VMW), which is expected to publish fourth-quarter results on February 27 after the closing bell, has been positive. They are looking for a 10% year-over-year increase in earnings to $2.17 per share.

After the post-earnings sell-off in November, the downtrend in Cisco’s shares continued in the following weeks and it slipped to a one-year low. Though the shares pared most of the losses towards the end of 2019 and early this year, they lost momentum in recent weeks.