Cisco Systems, Inc. (NASDAQ: CSCO) had a positive start to the year, carrying forward its transformation plan with strategic buyouts as the hardware maker seeks to evolve into a networking service provider. While retaining its leadership position in the core business, the San Jose-based firm has been diversifying into other promising areas such as cybersecurity and analytics.

After the early gains, the stock started losing steam mid-year and has dropped 22% in the last six months. The weak guidance issued by the management in the trailing two quarters spurred selloffs that dented the tech firm’s market share significantly.

Another reason for the market’s concern is the back-to-back executive departures, which can also cast a shadow over the company’s growth targets. Frank Palumbo, SVP of global data center sales, left the company last week to join a tech startup headed by former Cisco CEO John Chambers. Customer Transformation head Guillermo Diaz will be stepping down in February next year.

Reorganization

The company recently embarked on an operational overhaul, under which the enterprise and data center networking units were clubbed and the server computing products were integrated into the cloud business. As part of the reorganization, some of the leadership positions were rejigged.

Shareholder Value

The management recently reaffirmed its commitment to increase shareholder value by generating long-term profitable growth through investments in the innovation pipeline. However, it guided second-quarter earnings and revenues below the Street view, disappointing shareholders.

Time to Buy?

After retreating from the recent multiyear highs, Cisco shares are bound to return to the growth path in the coming days. The fact that the stock has become a little more affordable now makes it attractive to investors. Moreover, the steady growth of subscription and license revenues and the company’s prospects in the multi-cloud space position it to shift to growth mode in the near term. While the consensus rating on the stock is moderate-buy currently, more analysts are likely to recommend buy in the coming weeks. The 12-month price target of about $52 represents an 18% upside.

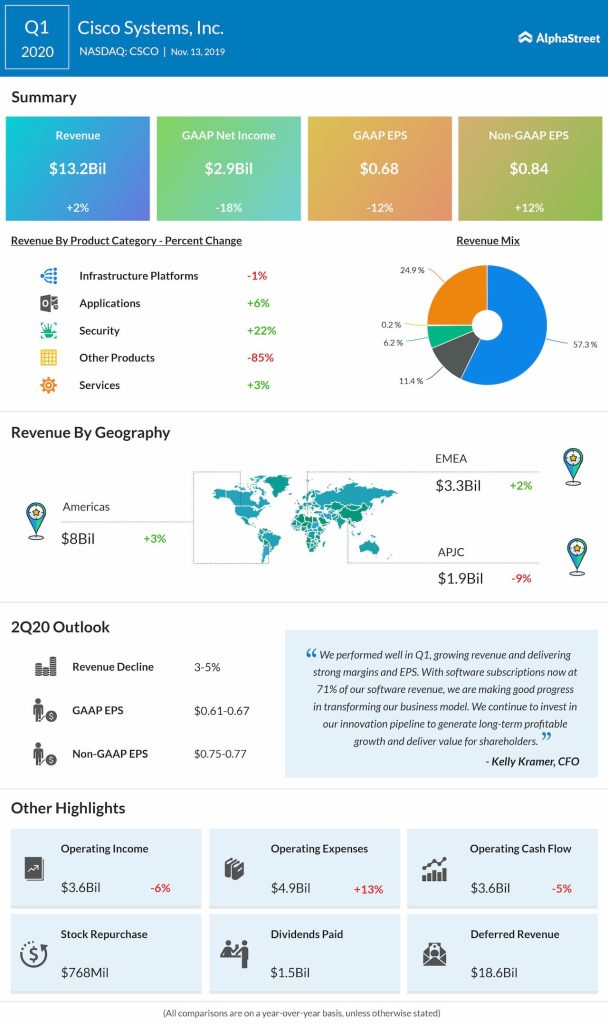

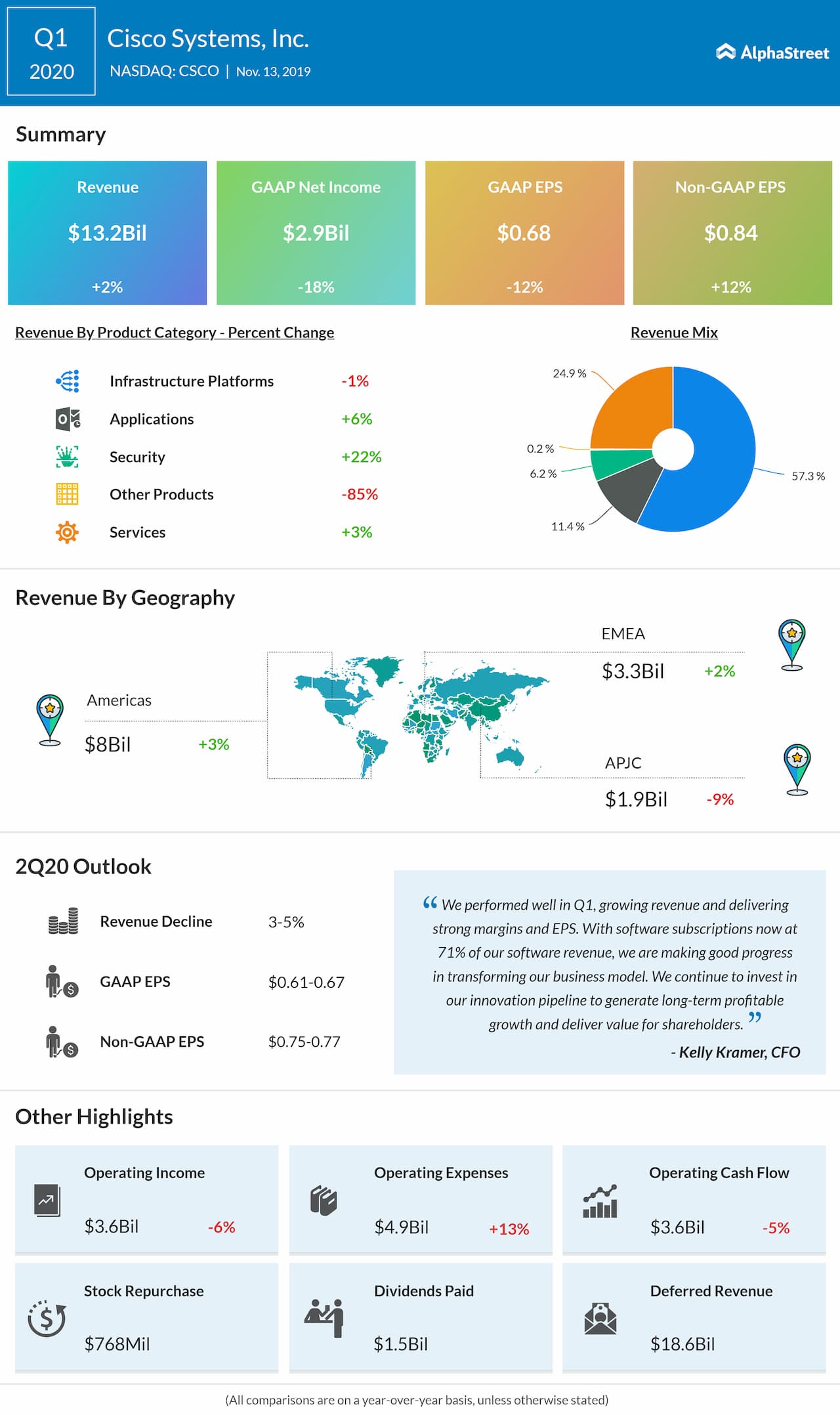

Cisco earned 84 cents per share in the first quarter, representing a 12% annual growth, even as revenues rose modestly to about $13 billion. Subscriptions accounted for about two-thirds of software revenues, reflecting the effective implementation of the new business model.