Shares of Costco Wholesale Corporation (NASDAQ: COST) were down on Tuesday. The stock has dropped 14% year-to-date and 11% over the past 12 months. Last week, the company delivered first quarter 2023 earnings results that were below market expectations. There is a mixed sentiment surrounding Costco, with some analysts seeing good long-term opportunity while others advising caution based on the headwinds and tailwinds ahead of the company. Here are a few points to keep in mind if you have an eye on this stock:

Sales

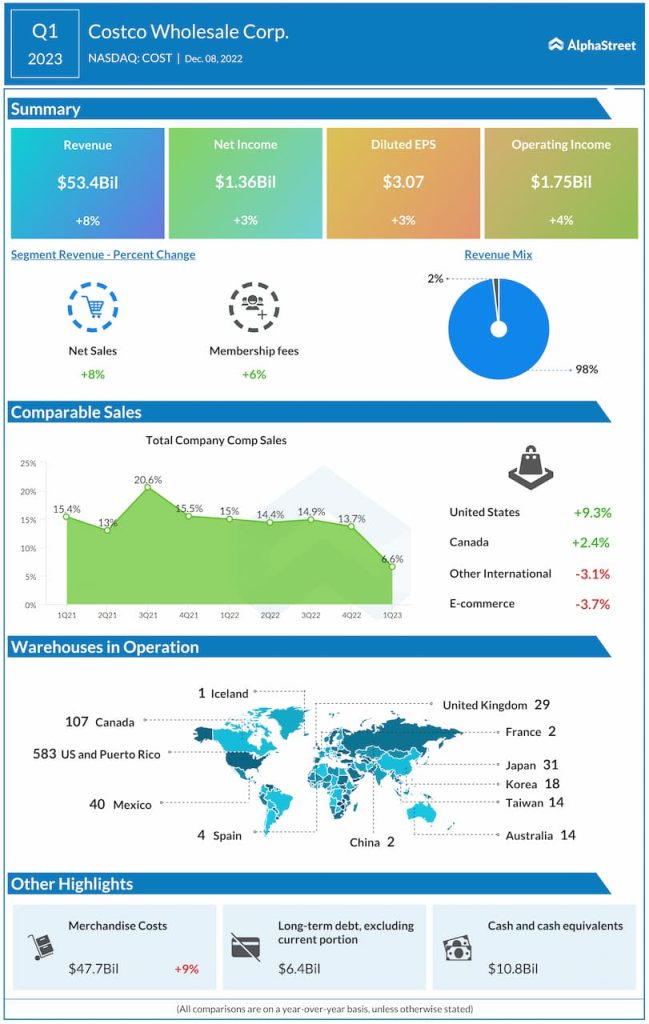

Costco continues to see its sales increase but its sales growth rate is slowing down. Net sales increased 8.1% to $53.4 billion in Q1 2023 while comparable sales rose 6.6%. This is lower than the 15% increase in net sales and 14% increase in comp sales reported in Q4 2022. In Q1, comp sales were up 9.3% in the US and 2.4% in Canada. Other International comps were down 3.1%.

During the quarter, Costco saw a 3.9% increase in traffic worldwide with a 2.6% growth in average transaction size. In the US, traffic was up 2.2% while average transaction size increased 6.9%. Ecommerce sales were down 3.7% in Q1.

On its quarterly conference call, Costco said that ecommerce growth had benefited mainly from big-ticket items like electronics and furniture earlier but these categories are now seeing some weakness which is in turn impacting ecommerce. The company still sees long-term growth opportunity in ecommerce.

Membership income

Membership fees comprise a significant part of Costco’s income. In Q1, membership fee income rose 5.7% year-over-year to $1 billion. Renewal rates in the US and Canada stood at 92.5% at the end of the quarter while the worldwide rate stood at 90.4%.

Costco ended the quarter with 66.9 million paying household members and 120.9 million cardholders, both up 7% versus last year. Paid executive memberships stood at 30 million at the end of Q1. Executive members currently make up 45% of paid memberships and just under 73% of worldwide sales.

Warehouse expansion plan

Costco plans to open 24 units in fiscal year 2023. In Q1, the company opened seven new warehouses. Of these, four were in the US and the remaining three were in Korea, New Zealand, and Sweden. The company plans to open three units in Q2, four in Q3, and 10 in Q4. Of the planned 24 units, 15 will be in the US.