Shares of Delta Air Lines (NYSE: DAL) turned red in midday trade on Wednesday after gaining earlier in the day, following the company’s announcement of its earnings results for the first quarter of 2024, in which revenue and profits beat estimates. The airline witnessed strong demand for travel during the March quarter and it is seeing this momentum continue into the June quarter.

Better-than-expected results

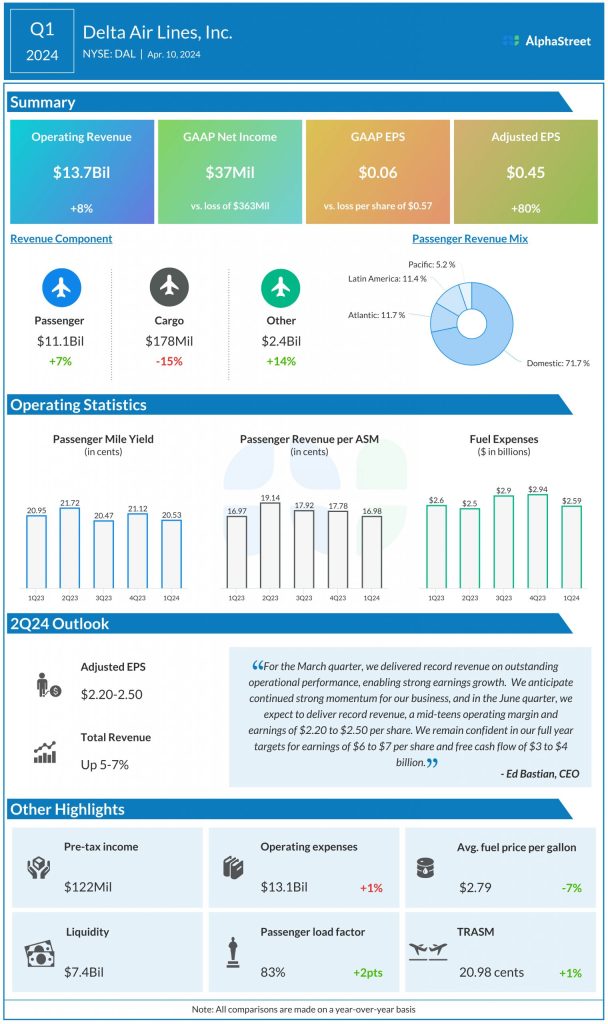

Delta delivered operating revenue of $13.7 billion for the first quarter of 2024, which was up 8% year-over-year and ahead of estimates. Adjusted operating revenue rose 6% to $12.5 billion. On a GAAP basis, the company delivered a net income of $37 million, or $0.06 per share, compared to a net loss of $363 million, or $0.57 per share, last year. Adjusted EPS jumped 80% to $0.45, beating expectations.

Business performance

Delta benefited from strength in demand for travel, both domestic and international. Domestic passenger revenue grew 5% while international passenger revenue was up 12% year-over-year. Demand for corporate travel also witnessed a pickup during the quarter. In its report, the airline said that based on a recent corporate survey, 90% of companies expect their travel volumes to increase or stay the same in the June quarter and beyond.

In Q1, passenger revenue increased 7% while cargo decreased 15%. Other revenue rose 14%. Total revenue per available seat mile (TRASM) was up 1% year-over-year while passenger revenue per available seat mile (PRASM) remained flat. Passenger load factor was 83%. Cost per available seat mile (CASM) decreased 6% during the quarter. Average price per fuel gallon was $2.79, down 7%.

Diversified revenue streams, including Loyalty, Premium, Cargo, and MRO made up 57% of total revenues in the first quarter. Premium revenue grew 10% YoY, while Loyalty revenue increased 12%, driven by co-brand spend growth and increasing premium card mix.

Outlook

Delta is seeing strong demand for travel continue into the June quarter. It expects revenue for Q2 2024 to be up 5-7% from the same period last year, with TRASM ranging from flat to down 2%.

The company expects unit revenue for all its geographic entities to remain relatively flat in Q2 compared to last year, with the exception of Latin America, where it is projected to decline in the double-digits.

For the second quarter of 2024, EPS is expected to range between $2.20-2.50 while for the full year of 2024, EPS is estimated to be $6-7.