Shares of Dollar General Corp. (NYSE: DG) have gained 20% over the past 12 months and 13% over the past one month. The company met expectations on its fourth quarter 2021 results and provided an upbeat outlook for the upcoming year. DG has a number of strategic initiatives in place to drive growth for its business over the long term. Here’s a look at a few of these plans and expectations:

Sales and profitability

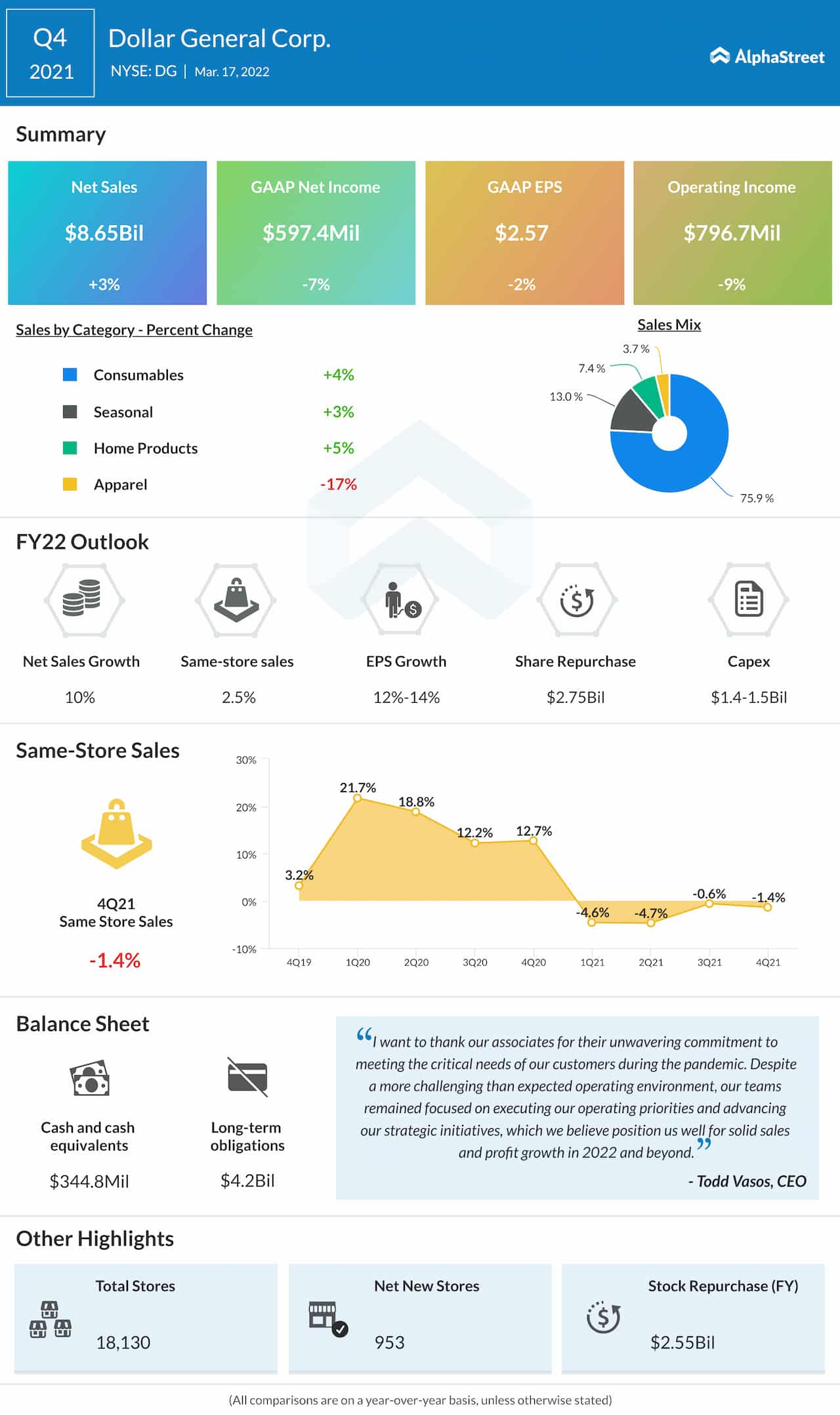

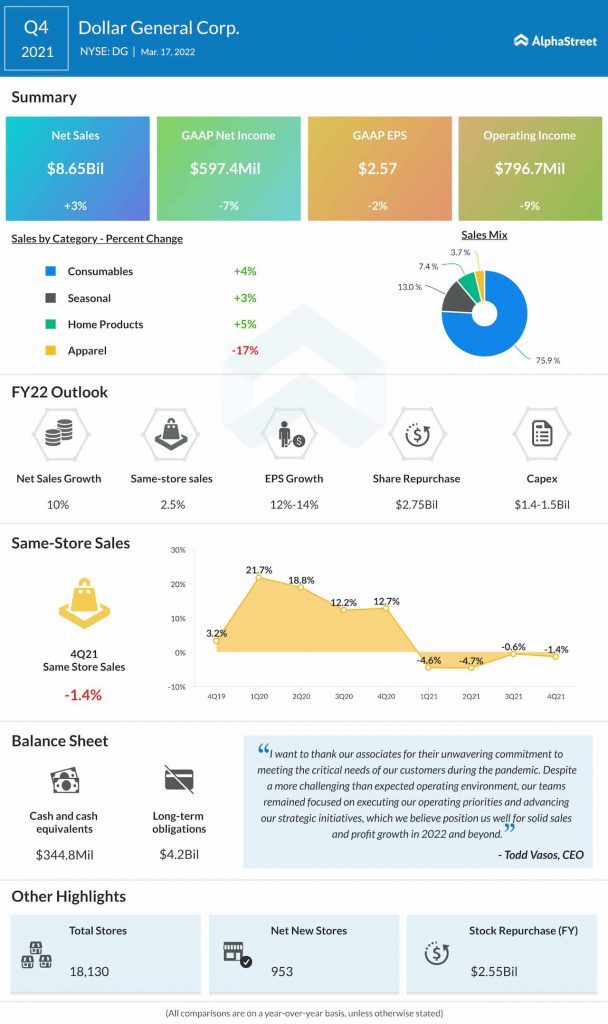

In Q4 2021, net sales increased 2.8% year-over-year to $8.7 billion. Same-store sales fell 1.4% YoY but was up 11.3% on a two-year stack basis. The topline results were impacted by lower customer traffic but this was largely offset by growth in average basket size.

Net earnings for the quarter decreased 1.9% to $2.57. Gross profit, as a percentage of sales, was 31.2%, down by 131 basis points mainly due to a higher LIFO provision, higher transportation distribution costs and a larger proportion of sales coming from the lower-margin consumables category.

For fiscal year 2022, the company expects net sales growth of approx. 10%, including an estimated benefit of approx. 2 percentage points from the 53rd week. Same-store sales are expected to grow around 2.5%. EPS is estimated to grow around 12-14%, including an estimated benefit of approx. 4 percentage points from the 53rd week. For the first quarter of 2022, comp sales are expected to decline 1-2% while EPS is estimated to range between $2.25-2.35.

Store fleet and strategic initiatives

During FY2021, Dollar General completed 2,902 real estate projects, including 1,050 new stores, 1,752 remodels and 100 relocations. For FY2022, the company plans to execute nearly 3,000 real estate projects in total, including 1,110 new stores, 1,750 remodels and 120 store locations.

The discount retailer expects around 800 of its new stores to be in the larger 8,500 square foot store format allowing for expanded assortment and room for future growth. Average sales per square foot at its larger format stores are about 15% higher than the average traditional store.

Dollar General’s non-consumables initiative (NCI) was available in more than 11,700 stores at the end of 2021. NCI consists of a new and expanded assortment in key non-consumable categories such as home, domestics, housewares and party.

The company’s NCI stores outperformed its non-NCI stores in both average ticket and customer traffic, driving an incremental 2.5% increase in total comp sales on average at NCI stores along with a meaningful improvement in gross margin rate. DG expects to realize ongoing sales and margin benefits from NCI in 2022 and it remains on track to complete the rollout across almost the entire chain by the end of the year.

Dollar General continues to be pleased with the results from its new store concept pOpshelf, which targets the more suburban customer. In Q4, the company opened 25 new pOpshelf locations, bringing the total number of stores to 55. In 2022, DG plans to triple its pOpshelf store count which would bring the total to more than 150 standalone pOpshelf locations.

Shareholder returns

Dollar General increased its quarterly dividend by 31% to $0.55 per share. The company also plans to repurchase approx. $2.75 billion in common stock this year.

Click here to read the full transcript of Dollar General’s Q4 2021 earnings conference call