Shopify Inc. (NYSE: SHOP) delivered an impressive financial performance in the first half of fiscal 2024, navigating a mixed consumer spending environment. The e-commerce firm looks poised to maintain the momentum for the rest of the year, leveraging continued growth in its subscription business and increasing market share. The company’s main strength is its unique business model that allows merchants to use the platform by paying fees.

Shopify’s stock has yet to regain momentum after withdrawing from its peak about three years ago, losing almost half its value. SHOP closed the last trading session above its long-term average of $72.64. The ongoing expansion into new markets and introduction of new services are expected to translate into long-term shareholder returns.

Shopify has a good track record of beating the market’s earnings and revenue estimates, a trend that has continued for over two years. Wall Street’s earnings expectation for the third quarter ending September 2024 is $0.37 per share. A year ago, the company earned $0.32 per share in the comparable quarter. It is estimated that the company generated revenues of $2.95 billion in Q3. The report is slated for publication on Tuesday, November 12, at 7:00 am ET.

Streamlining

The Shopify leadership is on a drive to strengthen margins and improve profitability by striking an optimal balance between growth and operational leverage. It expects third-quarter operating expenses to be 41-42% of revenue, which represents a 300-400 basis-point improvement from the prior-year period. Last year, the company reduced workforce by 20% and sold its logistics arm to streamline operations and focus more on the core business.

From Shopify’s Q2 2024 earnings call:

“What makes Shopify so powerful is how seamlessly all parts of the product work together, reducing complexity at every stage of a merchant’s journey. We understand that starting a business is hard and expanding into new markets adds even more complexity. As our merchants grow, Shopify tackles these challenges so they don’t have to. So, one of the coolest things we rolled out at this edition was Markets. What used to be Markets and Markets Pro are now streamlined into cross border products, international selling and managed markets respectively.”

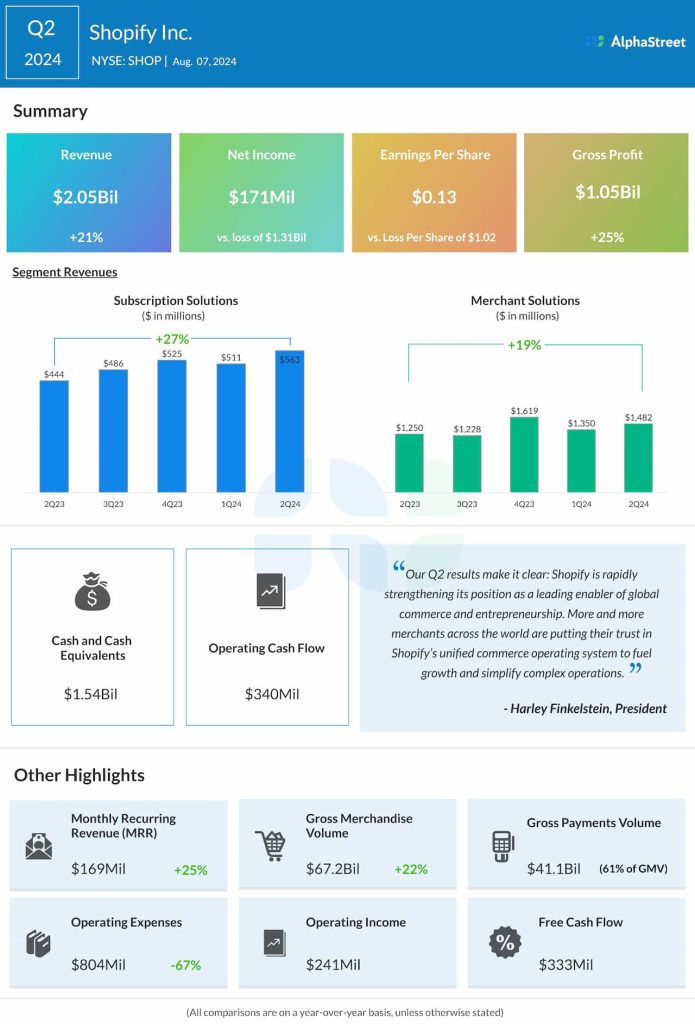

Subscription Leads

In the June quarter, the top line climbed 21% from last year to $2.05 billion, with Subscription Solutions and Merchant Solutions sales growing 27% and 19% respectively. The company reported net income of $171 million or $0.13 per share for the second quarter, compared to a loss of $1.31 billion or $1.02 per share in the prior-year period. Gross merchandise volume, an important metric that represents the total dollar value of orders facilitated through the Shopify platform, grew 22% to $67.2 billion in Q2.

The company’s stock opened slightly above $85 on Friday and traded higher for the most of the session. The shares have grown more than 10% so far this year.