In its six years as a public-listed company, Facebook (FB) has never had such a tortuous run as it had in 2018. The stock, battered by back-to-back data breach scandals, is down about 17% so far this year. In the past 52-week period also, the stock is in red, down as much as 11%.

With numerous regulatory watchdogs tightening their grip on the social media giant, revenue growth could possibly take a hit. The initial hints of the company’s future performance trajectory will be revealed as it reports third-quarter earnings on Tuesday, October 30.

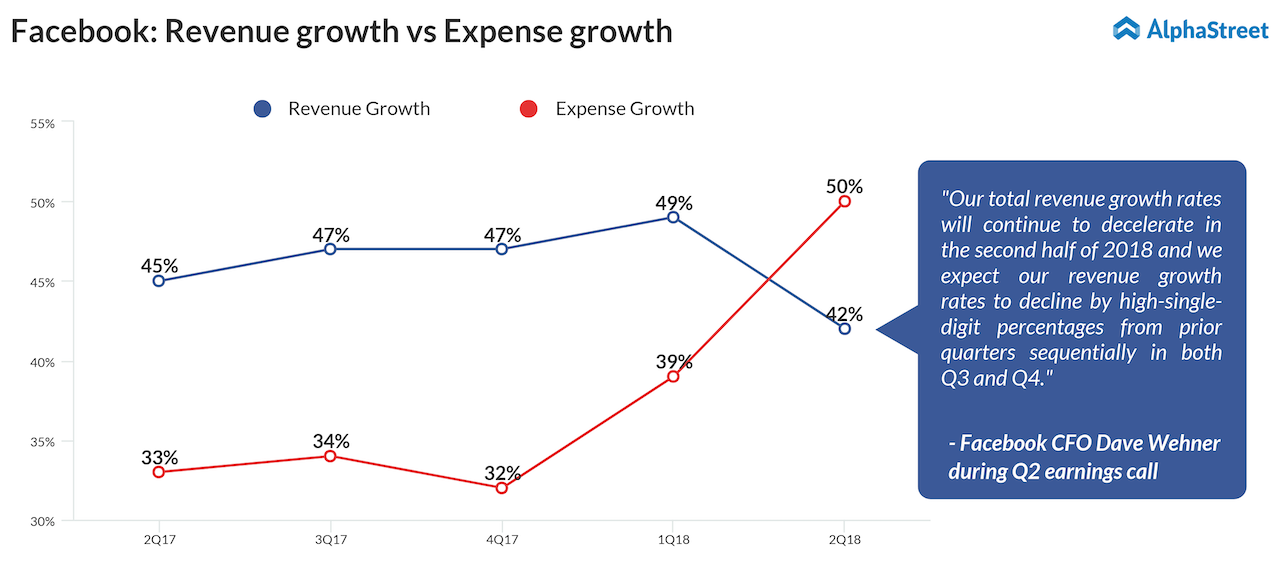

Analysts predict the company’s EPS to be $1.46 in the third quarter, down over 8% from last year, weighed down the higher expenses it is expected to incur to establish better data security. During the past three quarters, Facebook’s expenses have been on a steady rise, and this trend is likely to continue in Q3.

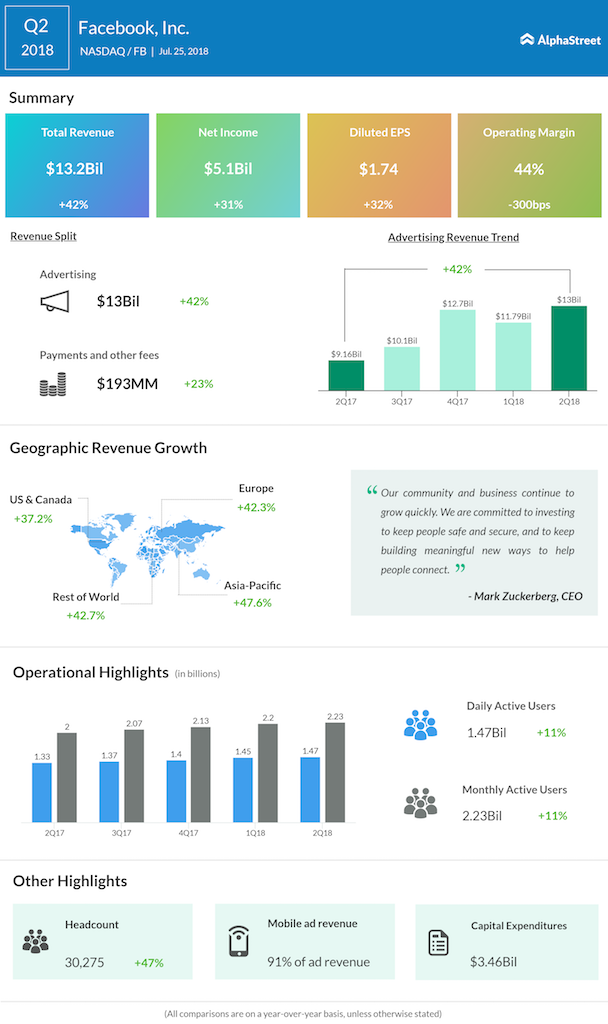

Yet, revenue is anticipated to jump around 38% to $14.29 billion as it continues to benefit from the boost in digital advertising. Though the growth rate is pretty impressive as such, it is still slower than what the company is used to reporting. In Q2 and Q1 of this year, revenue grew 42% and 49% respectively.

But some of these concerns are offset by Facebook’s dominant status in the digital ad market. According to a recent report by eMarketer, the social media giant is expected to hold over a fifth of the total US digital advertising market this year, only behind Google (GOOGL).

Adding to that is the company’s planned expansion into video streaming, which would establish additional areas of advertising revenues. Peer firm Twitter (TWTR) reporting a growth in ad revenue during its quarterly results this week cements the optimism in FB stock as well.

Top Facebook investors ask for Mark Zuckerberg’s removal as chairman

So is Facebook an acceptable risk ahead of earnings? It appears to be so.

First, the stock is cheap and currently trading at a 30% discount from its record high of $217.5 on July 25 this year. Second, a slowdown in user base growth is organically offset by an increase in average revenue per user (ARPU). In the US and Canada, ARPU is projected to grow to $30.31 during the third quarter, from $21.20 in the prior-year period.

Complementing this increase would be an expected double-digit jump in monthly active users in the Asia-Pacific region to 922.50 million in Q3.

It’s true that Facebook’s operating margins are getting squeezed by the higher privacy requirements. Separately the risks associated with data breaches and related fines are far from over. But meriting the stock based on its current trading price, it wouldn’t be such a bad idea to take advantage of the situation. As long as Facebook continues to grow in digital ad revenue, it holds some promise and, in turn, upside.