Shares of General Mills, Inc. (NYSE: GIS) were down over 2% on Wednesday after the company delivered mixed results for the third quarter of 2025 and lowered its outlook for the fiscal year. Sales and profits for the quarter declined versus the prior-year period, and the company expects the challenges seen in Q3 to persist for the remainder of the year.

Mixed results

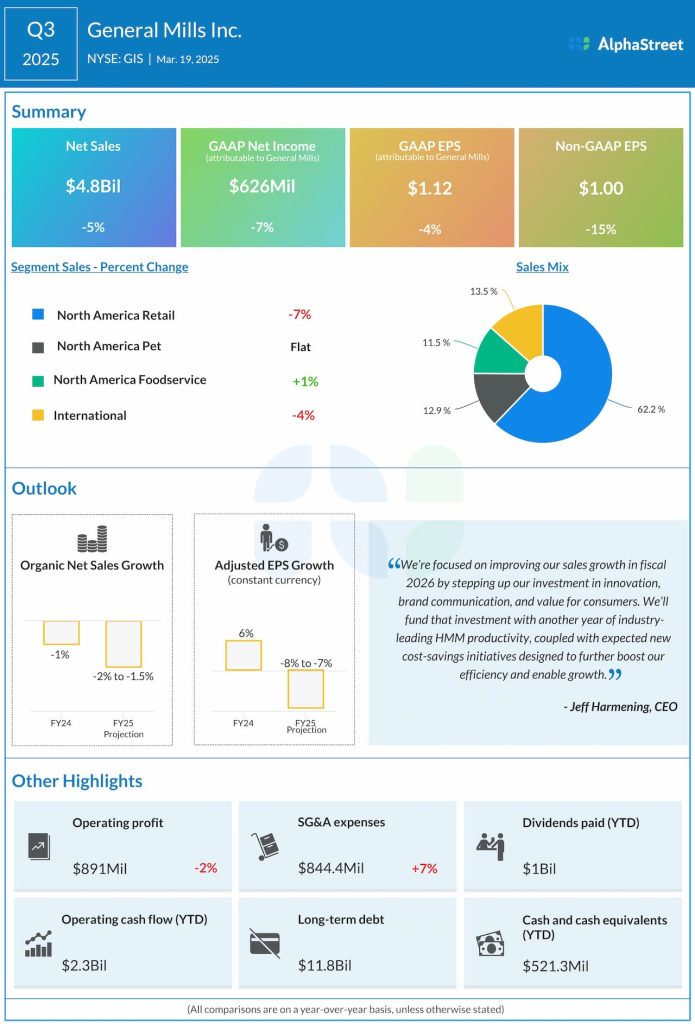

General Mills’ net sales decreased 5% year-over-year to $4.84 billion in Q3 2025, missing estimates of $4.96 billion. Organic sales also dropped 5%, mainly due to retailer inventory headwinds, a slowdown in snacking categories, and slower demand in US away-from-home channels. GAAP earnings per share was down 4% to $1.12. Adjusted EPS of $1.00 decreased 15% YoY but surpassed projections of $0.97.

Business performance

General Mills saw sales decline or remain flat across most of its segments during the third quarter, with the exception of North America Foodservice, which rose 1%. The highest decline of 7% was in the North America Retail segment, where gains in Pillsbury refrigerated dough and Totino’s hot snacks were offset by a slowdown in key US snacking categories. Sales declined across US Morning Foods, US Snacks, and US Meals & Baking Solutions.

Net sales in the Pet segment remained flat, with mid-single-digit increases in wet pet food and pet treats, and a mid-single-digit decline in dry pet food. The Foodservice segment saw a slowdown in away-from-home sales but benefited from gains in K-12 schools, healthcare, and college and university channels. Sales in the International segment fell 4%, with declines in China and Brazil, partly offset by growth in Europe & Australia.

Lowered outlook

General Mills expects its sales trends in Q4 2025 to look similar to Q3, excluding the impact of retailer inventory and other timing factors. The company expects macroeconomic uncertainty to persist in the fourth quarter. It also plans to make certain commercial investments in Q4.

Based on these assumptions, GIS lowered its guidance for fiscal year 2025. The company now expects organic sales to be down 1.5-2.0% compared to the previous expectation of flat to up 1%. Adjusted EPS is now expected to be down 7-8% in constant currency.