Shares of Dollar Tree Inc. (NASDAQ: DLTR) were down over 1% on Wednesday, a day after the company reported earnings results for the third quarter of 2022. Revenue and earnings beat estimates and the company raised its sales outlook for the full year. Here’s a look at the discount store’s expectations for the remainder of the year:

Sales

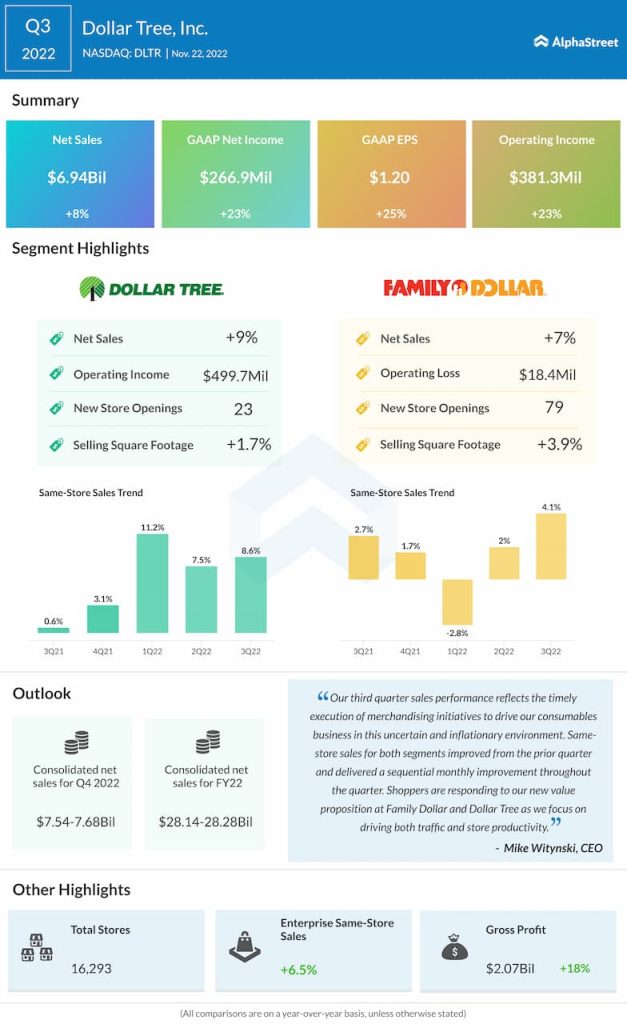

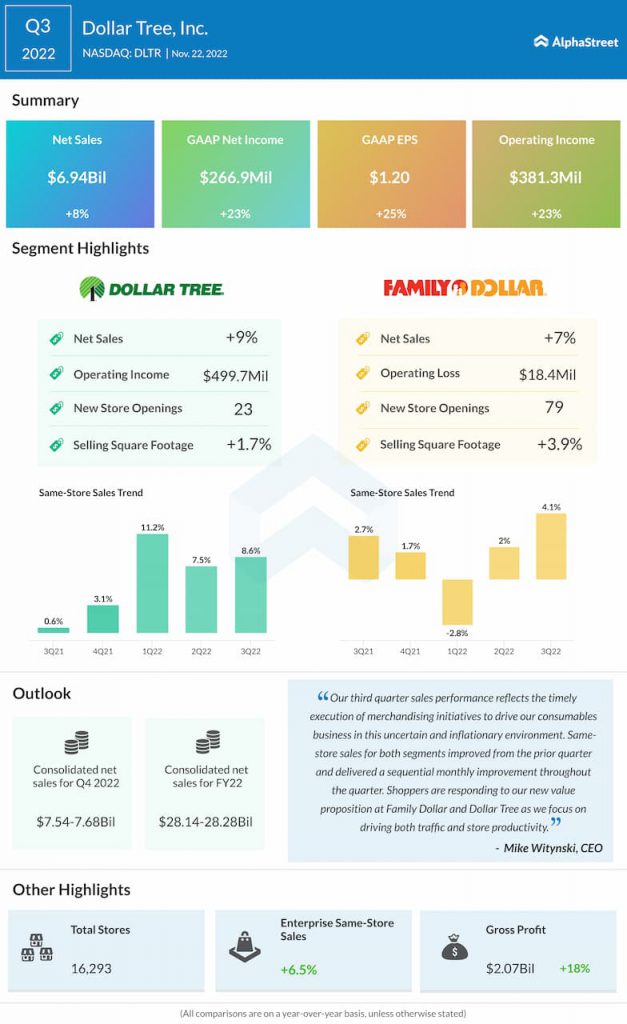

Dollar Tree generated consolidated net sales of $6.94 billion for the third quarter of 2022, which was up 8.1% from the same period a year ago. Net sales at the Dollar Tree segment increased 9% to $3.7 billion while at the Family Dollar division, it grew 7% to $3.1 billion versus last year.

Enterprise same-store sales increased 6.5% in the quarter. Dollar Tree same-store sales rose 8.6% while Family Dollar same-store sales grew 4.1%. Both segments witnessed sequential monthly improvement in same-store sales throughout the quarter. In the Dollar Tree division, consumables comps surpassed discretionary comps. Consumables comps were up 9.3%. In the Family Dollar segment, consumables comp rose 4.7%.

The company increased its sales outlook for the full year of 2022. Consolidated net sales are now expected to range between $28.14-28.28 billion versus the previous outlook of $27.85-28.10 billion. Comparable store sales are expected to increase in the mid-single digits for the year. This includes a high-single digit increase in the Dollar Tree segment and a low-single digit increase in the Family Dollar segment.

For the fourth quarter of 2022, consolidated net sales are expected to range between $7.54-7.68 billion while same-store sales are expected to increase in the mid to high single digits.

Profitability

In Q3 2022, Dollar Tree’s net income increased 23% to approx. $267 million and EPS increased 25% to $1.20. Total gross margin improved 240 basis points to 29.9%. Dollar Tree segment gross margin improved 520 basis points due to higher initial mark-on and lower freight costs, but was partly offset by a greater penetration of low-margin consumables and product cost inflation. Family Dollar gross margin fell 100 basis points, mainly due to product mix shift and product cost inflation.

Looking ahead, the company expects strength in consumables to pressure near-term margins. For the full year of 2022, EPS is expected to be in the lower half of the previously provided outlook range of $7.10-7.40.