For PayPal Holdings (NASDAQ: PYPL), 2019 has been a fruitful year as far as its overall performance is concerned. The stock witnessed a steady growth during the period. Electronic payment service is one of the fast-growing businesses across the world and PayPal looks well prepared to tap the opportunity.

With more and more consumers and merchants going digital, the uptrend will continue in the coming years. The trend is evident from the faster pace at which e-commerce sales grew this year, compared to conventional retail sales. The superior consumer experience being offered by PayPal, facilitating convenient navigation on the platform, gives it an edge over competitors like Shopify (SHOP).

Outlook

The management is looking for double-digit revenue growth in the final three months of the year, betting on the recent expansion into the Chinese market. A statement issued by CEO John Rainey, after completing the acquisition of China-based payment technology provider GoPlay recently, indicates that more buyouts are in the pipeline.

As the number of people using the PayPal network increases, there will be a corresponding growth in the number of merchants wanting to join the platform. From an investment perspective, PayPal is reasonably priced, compared to Shopify which has a higher valuation. The stock, which retreated from its peak earlier this year, has ample room for further growth. Analysts, in general, have aptly assigned buy rating on it, with a price target of $126.

More Deals

The management is expected to continue with the strategy of expanding through multiple partnerships, with focus on the company’s core business of electronic payment service. Meanwhile, PayPal will have to keep investing in infrastructure, in line with the rapid evolution of the industry, which will likely restrict margin growth in the coming quarters.

Solid User Growth

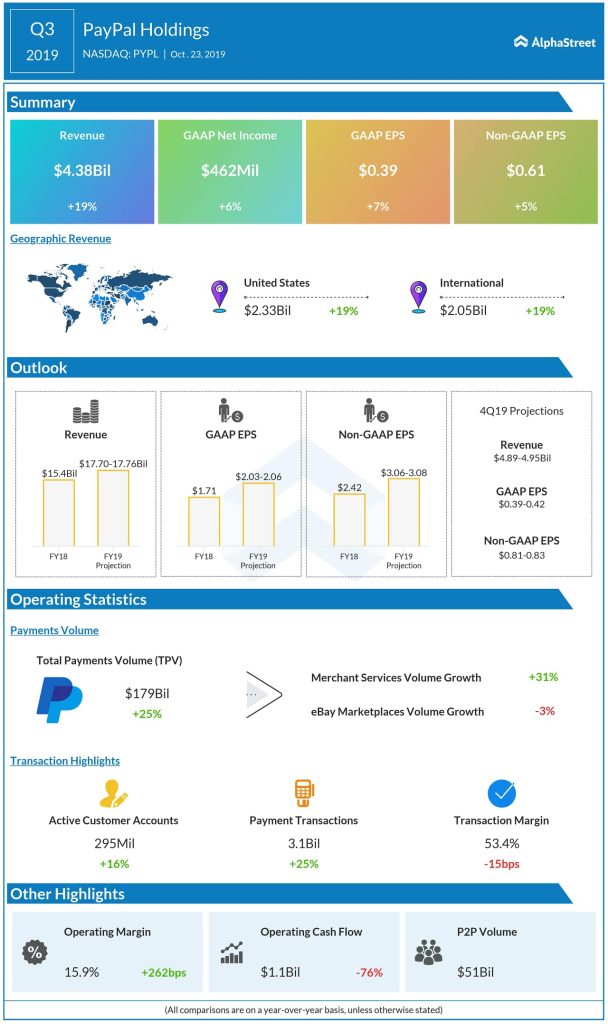

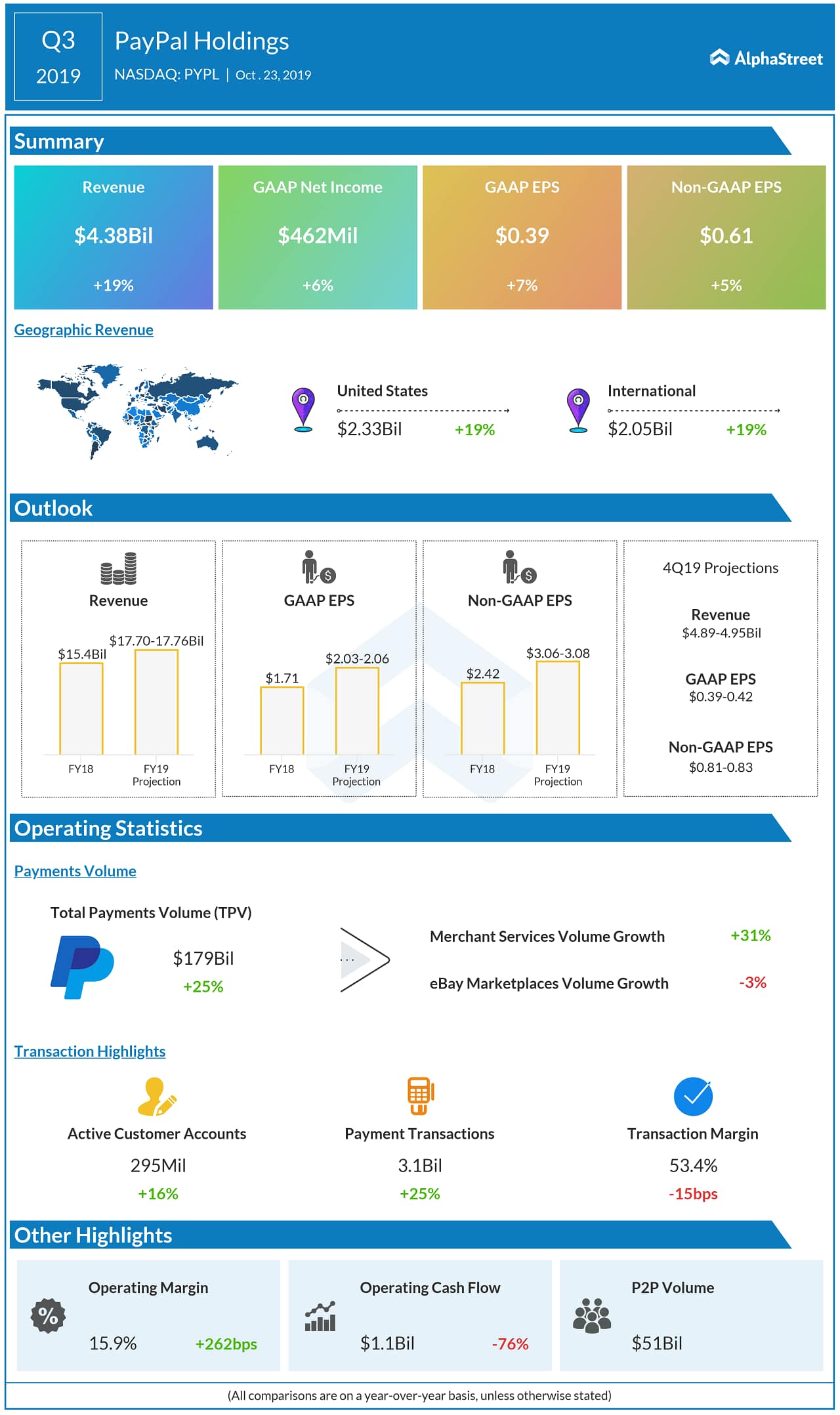

The number of active accounts rose by 16% to 295 million in the third quarter, while payment transactions and total payment volume increased to 3.1 billion and $179 billion respectively. As a result, revenues and earnings topped expectations.

Also see: PayPal Q3 2019 Earnings Conference Call Transcript

PayPal is one of the few firms that managed to increase market value consistently over the years. The stock gained 25% since the beginning of the year.