Shares of Home Depot (NYSE: HD) stayed red on Wednesday. The stock has gained 8% over the past three months. The company delivered a generally positive performance for the second quarter of 2025, and it remains confident in its ability to manage the current macroeconomic environment, which led it to reaffirm its outlook for the full year.

Sales and earnings growth

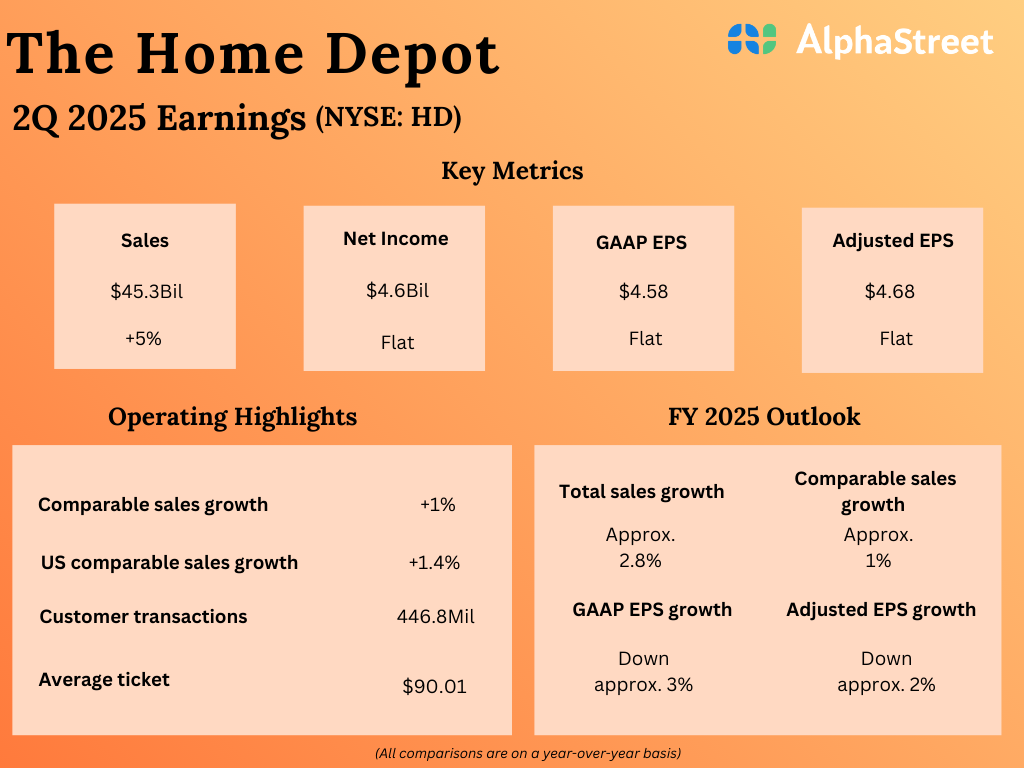

In the second quarter of 2025, Home Depot’s sales increased 4.9% year-over-year to $45.3 billion. Comparable sales increased 1%. While GAAP earnings per share dipped slightly to $4.58 in Q2 compared to the prior-year period, EPS, on an adjusted basis, rose to $4.68.

Business performance

In Q2, comparable sales in the US increased 1.4%. The business gained momentum as customers engaged in smaller home improvement projects, but larger discretionary projects remained pressured.

During the quarter, comp average ticket increased 1.4%, driven by higher ticket items and core commodity inflation, but comp transactions were down 0.4%. Big-ticket comp transactions, or those over $1,000, were positive 2.6%. The company delivered positive comps across most of its merchandising departments. Comp sales were positive in both the Pro and DIY customer segments, with strength in Pro-heavy categories as well as seasonal categories for DIY.

HD is making progress in expanding its digital capabilities. In Q2, digital sales increased around 12% YoY. The company has seen a rise in engagement and sales helped by fast delivery of products. It continues to invest in AI and other capabilities to improve its customer experience and drive growth.

Home Depot is also benefiting from its acquisitions. The acquisition of SRS has helped it gain access to the specialty trade Pro customer, develop its Pro ecosystem, and gain cross-selling opportunities. SRS has delivered better-than-expected performance along with growth and revenue synergies.

The company is optimistic about the pending acquisition of GMS, a distributor of specialty building products such as drywall and ceilings. This acquisition is expected to be complementary to SRS’ business and is expected to broaden SRS’ distribution footprint across the US and Canada. This acquisition is expected to boost HD’s offerings for its Pro customers.

Outlook

Home Depot reaffirmed its outlook for fiscal year 2025. The company expects total sales growth of approx. 2.8%, and comparable sales growth of approx. 1% for the comparable 52-week period. GAAP EPS is expected to decline approx. 3% while adjusted EPS is expected to decline approx. 2% versus FY2024.