Unlike some of its peers in the tech industry, Intel Corporation (NASDAQ: INTC) has not been able to withstand the challenge posed by coronavirus, which came at a time when the chipmaker was going through a rough patch. Stiff competition and lack of innovation have taken the sheen off the once-hailed Intel model.

A Bad Year

Currently, INTC is one of the worst-performing tech stocks that traded below the $50-mark quite often this year. The recent trend has left analysts skeptical about the stock’s future prospects and the majority of them recommend holding it, though the average target price points to a modest uptick. The company has underperformed the industry and lost several billion dollars in market value. On Tuesday, the stock got a respite and made handsome gains after Intel’s management expressed its resolve to address the issues facing the company, in response to concerns raised by an activist investor.

The virus outbreak has derailed the company’s growth initiatives, highlighting the need for more effective measures to stay relevant in the rapidly changing industry. Rivals like Advanced Micro Devices (AMD), which got a major boost earlier this year after Intel delayed its 7-nanometer chips, and Asian counterpart Taiwan Semiconductor Manufacturing Company have been making steady inroads into the global semiconductor market. Also, Intel’s top customers like Apple, Inc. (AAPL) and Microsoft Corp. (MSFT) are drifting to suppliers who offer cheaper solutions.

Long-term Prospects

While its earlier efforts to build a competitive solution for 5G did not yield the desired results, the largely-untapped market for the high-speed wireless technology offers opportunities the company can count on. The answer to Intel’s problems lies in shifting focus to cloud-based solutions, rather than banking on its prowess in conventional microprocessor and data center technology. That said, its fundamentals remain strong — with an impressive balance sheet and cash flow — making the stock a good long-term bet.

We are actively executing against a diversified growth strategy and now have several multi-billion dollar businesses fueled by data and the rise of artificial intelligence, 5G network transformation and the intelligent autonomous edge. We built these businesses by positioning the Company to grow share in the largest market opportunity in our history, in a world where everything increasingly looks like a computer. Our ambitions are much greater and to realize them, we must play a larger role in our customers’ success.

ADVERTISEMENTRobert Swan, chief executive officer of Intel

Weak Q3

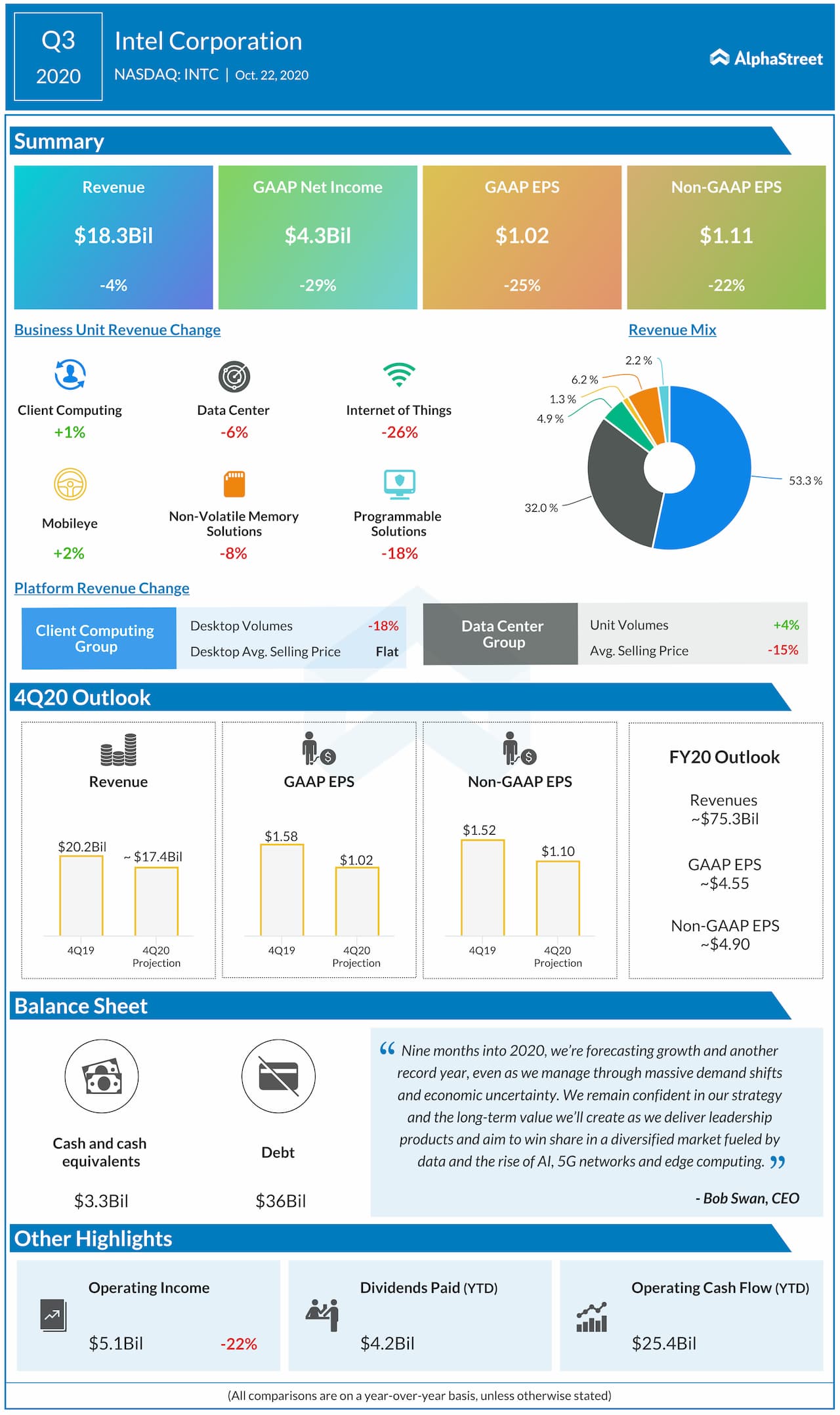

In the most recent quarter, the company’s finances came under pressure from COVID-related headwinds, reversing the uptrend seen in the first half. In what could be a major disappointment for investors, earnings dropped in double-digits to $1.11 per share in the third quarter, reflecting a 4% decrease in revenues to $18.3 billion. But the results came in above the market’s prediction. While the core Client Computing segment stayed largely unaffected, the other divisions contracted.

Read management/analysts’ comments on Intel’s Q3 earnings

Initial estimates indicate that the downtrend continued in the final months of the fiscal year, owing to the demand shifts and economic uncertainty. The management currently expects fourth-quarter earnings and revenues to be below the prior-year levels.

Stock Falls

Intel’s stock decreased by about 17% in 2020, going through several ups and downs. The shares traded lower during Wednesday’s regular trading, after closing the previous session at $49.39.