Shares of Dollar General Corporation (NYSE: DG) plunged 12% on Thursday after the company missed expectations for its second quarter 2023 earnings results and lowered its guidance for the full year. The stock is down 44% year-to-date. Here are the key takeaways from the Q2 report:

Results miss expectations

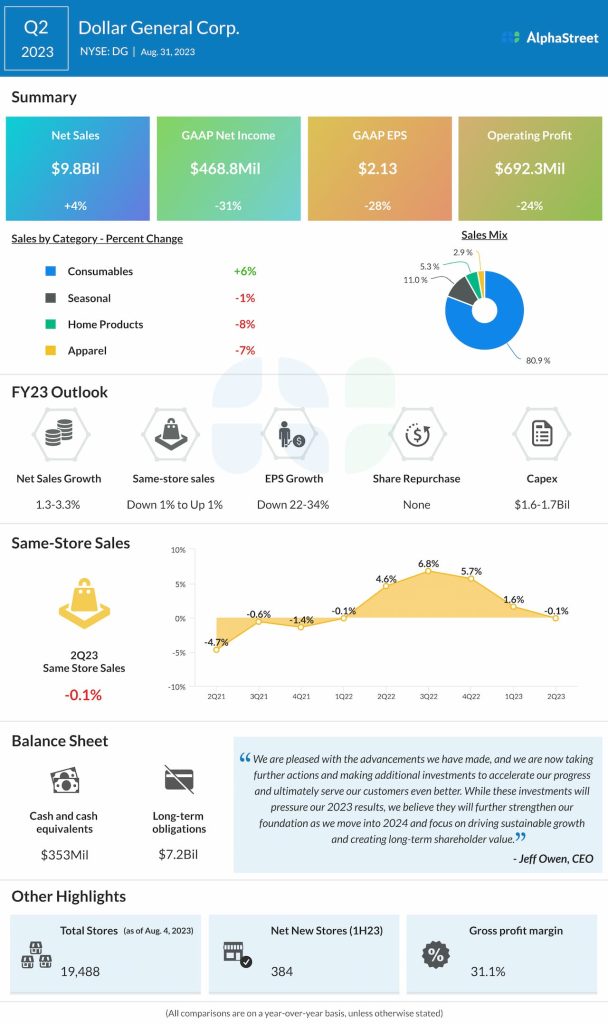

In Q2 2023, Dollar General’s net sales increased 3.9% year-over-year to $9.8 billion, but fell short of the estimates of $9.9 billion. The growth was driven mainly by positive sales contributions from new stores, but was partly offset by a decline in same-store sales and the impact of store closures.

Same-store sales declined 0.1% due to a drop in customer traffic, which was partly offset by an increase in average transaction amount. Net income decreased 30.9% to $468.8 million while EPS fell 28.5% to $2.13, missing the consensus target of $2.46.

Category performance and margins

The discount retailer saw sales growth in consumables during the quarter while the remaining categories – home, apparel and seasonal all witnessed declines. Sales in consumables grew 6% while home products, apparel and seasonal recorded decreases of 8%, 7% and 1% respectively.

The consumables category making up a larger part of sales coupled with lower inventory markups and higher shrink as well as markdowns led to a drop of 126 basis points in gross profit margin, which stood at 31.1%.

Operating profit declined 24.2% to $692.3 million while SG&A expenses increased 10% to $2.35 billion in the quarter. At the end of Q2, Dollar General had a total store count of 19,488. The company plans to open 990 new stores, remodel 2,000 stores and relocate 120 stores in FY2023.

Guidance cut

Dollar General anticipates softer sales and a rise in inventory shrink during the second half of 2023. In addition, the company is taking actions to speed up its inventory reduction efforts and investing in areas like retail labor to better serve customers. These actions and investments are expected to result in an incremental operating profit headwind of up to $170 million in the back half of the year.

Taking these factors into account, Dollar General lowered its guidance for the full year of 2023. It now expects net sales to grow 1.3-3.3% versus its previous expectation of 3.5-5.0% growth. Same-store sales growth is expected to range between a decline of approx. 1% to growth of 1% compared to the prior expectation of growth of 1-2%. EPS is now expected to range between $7.10-8.30, which would reflect a YoY decline of 22-34%.