Shares of Macy’s, Inc. (NYSE: M) gained over 1% in mid-day trade on Wednesday after falling earlier in the day despite the company delivering better-than-expected results for the third quarter of 2025. Revenue and earnings beat estimates and the retailer raised its guidance for the full year of 2025. However, a cautious outlook for the fourth quarter took a toll on the stock.

Results beat estimates

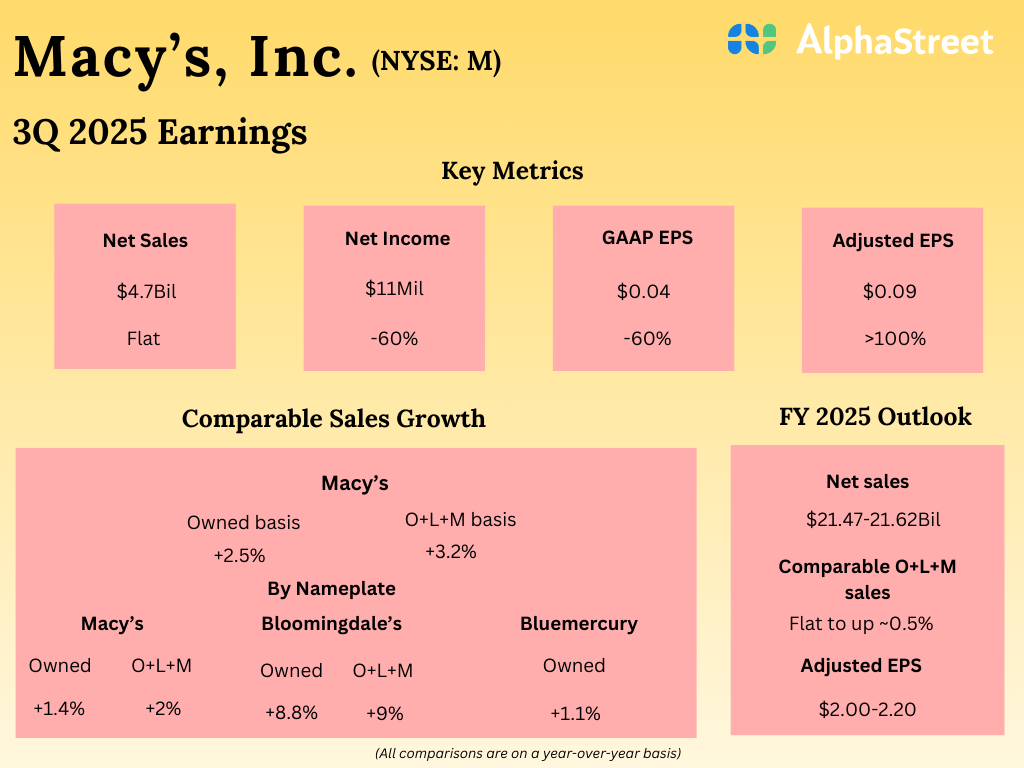

Macy’s Q3 2025 net sales of $4.71 billion decreased slightly from the year-ago period but surpassed its own guidance range as well as analysts’ projections. Analysts were looking for sales of $4.53 billion for the quarter. The company posted adjusted earnings of $0.09 per share, which more than doubled from EPS of $0.04 reported last year, and beat analysts’ estimates of a loss of $0.15 per share.

Nameplate strength

In Q3, Macy’s comparable sales increased 2.5% on an owned basis and 3.2% on an owned-plus-licensed-plus-marketplace (O+L+M) basis, helped by strong performance across nameplates. Comparable sales for the company’s go-forward business were up 2.7% on an owned basis and 3.4% on an O+L+M basis.

Although net sales for the Macy’s nameplate were down 2.3% in Q3, its comparable sales rose 1.4% on an owned basis and 2% on an O+L+M basis. Go-forward business comparable sales were up 1.7% on an owned basis and 2.3% on an O+L+M basis. Comparable sales for Macy’s Reimagine 125 locations grew 2.3% on an owned basis and 2.7% on an owned-plus-licensed (O+L) basis.

Net sales for the Bloomingdale’s nameplate increased 8.6% in the third quarter. Comparable sales were up 8.8% on an owned basis and 9% on an O+L+M basis, marking its highest comps in 13 quarters. Net sales for the Bluemercury nameplate grew 3.8%, with comparable sales growth of 1.1% on an owned basis.

Within Macy’s and Bloomingdale’s, the company saw strong performance in categories such as fine jewelry, ready-to-wear men’s apparel, shoes, watches and handbags. It benefited from improvements in brand curation and omni-channel capabilities. The retailer sees significant opportunities for Bloomingdale’s to grow in existing markets, expand brand distribution, increase digital penetration, and open additional small format and outlet locations.

Guidance hike

Macy’s raised its guidance for the full year of 2025. The company now expects net sales to range between $21.47-21.62 billion and comparable O+L+M sales to be flat to up 0.5%. Comparable O+L+M sales for the go-forward business is now expected to be flat to up 1%, and adjusted EPS is now expected to be $2.00-2.20.

The retailer anticipates consumers to be more choiceful in the fourth quarter of 2025. It expects net sales of $7.35-7.50 billion and adjusted EPS of $1.35-1.55 for the holiday quarter. However, comparable O+L+M sales is expected to be down 2.5% to flat in Q4. For the go-forward business, comparable O+L+M sales is expected to be down 2% to flat.