Credit card behemoth Visa, Inc. (NYSE: V) this week reported mixed results for the June quarter, with earnings matching expectations and sales slightly missing the view. Both numbers grew in double digits year-over-year, reflecting strong growth in payments and cross-border volumes. While consumer spending, in general, remains stable, it is estimated that spending among lower-income customers will be under pressure from high inflation, which doesn’t bode well for the company.

Visa’s current stock price is broadly unchanged from the level seen at the beginning of the year, though it climbed to an all-time high in March. After that, the stock entered a downward spiral and lost significant momentum ahead of the earnings. It rallied soon after the announcement but pulled back soon. From an investment perspective, the low price is a positive and the stock remains a compelling investment.

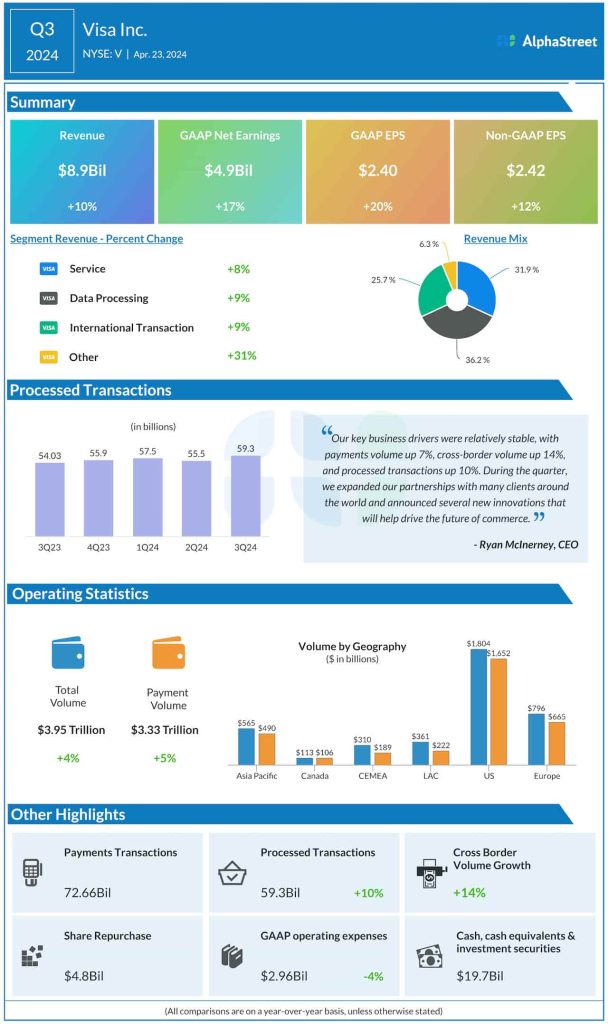

Mixed Outcome

In the third quarter of 2024, adjusted earnings rose sharply by 12% to $2.42 per share from $2.16 per share in the comparable period last year. Unadjusted net income rose to $4.87 billion or $2.40 per share in Q3 from $4.16 billion or $2.0 per share a year earlier. The bottom line benefitted from a 10% increase in revenues to $8.9 billion. Revenue grew across all operating segments. Payments volume and cross-border volume increased by 5% and 14% respectively during the three months. Earnings came in line with estimates while sales missed, after beating consistently in the trailing nine quarters.

From Visa’s Q3 2024 earnings call:

“One area of strong revenue growth this quarter was in card benefits, where we enable our clients to offer unique value propositions tailored to their customer base in travel, entertainment, restaurants, insurance, and more. Strong issuance in premium cards across most of our regions has fueled this growth in the third quarter. For example, in Latin America, travel benefits have grown with over 370,000 unique visits to our Visa Infinite airport lounge in Brazil, representing customers from a number of leading issuers.”

Outlook

The management expects payment volume and processed transactions to grow at a similar rate in the fourth quarter. On an adjusted basis, Q4 revenue is seen increasing in the low double digits, which represents an improvement from the Q3 growth rate of 10%. In the September quarter, adjusted earnings per share is expected to increase at the high end of low-double-digits. For the whole of fiscal 2024, the company projects adjusted EPS growth in the low teens.

Shares of Visa traded up 1% on Thursday afternoon. The stock, which has gained about 7% in the past twelve months, slipped below its long-term average this week.