Kin Insurance is a leading insurance technology company specialized in high-risk residential areas. The direct-to-consumer business model and use of advanced technology allow the company to offer affordable pricing without compromising coverage. Founded in 2016 by a team of financial technology entrepreneurs, Kin partners with national and regional home service providers to serve customers effectively.

In an exclusive Q&A with AlphaStreet, co-founder and chief executive officer Sean Harper spoke about the company’s business strategy and expansion plans. Here’s the full interview:

What differentiates Kin Insurance from competitors, other than the focus on high-risk markets?

There are a few salient points that illustrate why Kin is a great company with a high ceiling. First, we’re the only pure-play direct-to-consumer insurtech focused on the growing homeowners insurance market. Even though homeowners insurance is a virtual product, it’s oddly sold through retail stores.

At Kin, we’re more discerning about which customers are good for us; we target customers strategically using creative online and direct mail campaigns, which helps us achieve a lower loss ratio compared to more established insurers.

Second, we’re high tech, whereas our legacy peers are on average >100 years old and wrestling with tech from a decidedly different age. Our tech allows us to: deliver a better user experience and be precise about who we’re marketing to; gather and analyze more data for underwriting and pricing, which helps keep prices and the loss ratio low; and provide an efficient, customer-friendly automated claims service.

Third, we have a financial model called a reciprocal exchange, that’s better for a tech company like ours. We operate an insurance company that has a credit rating and is regulated just like any other insurance company, but it’s owned by our customers who have a vested interest in the business.

ALSO READ: Our goal in 2022 is to keep advancing in all key aspects: SQL founder Rani Kohen

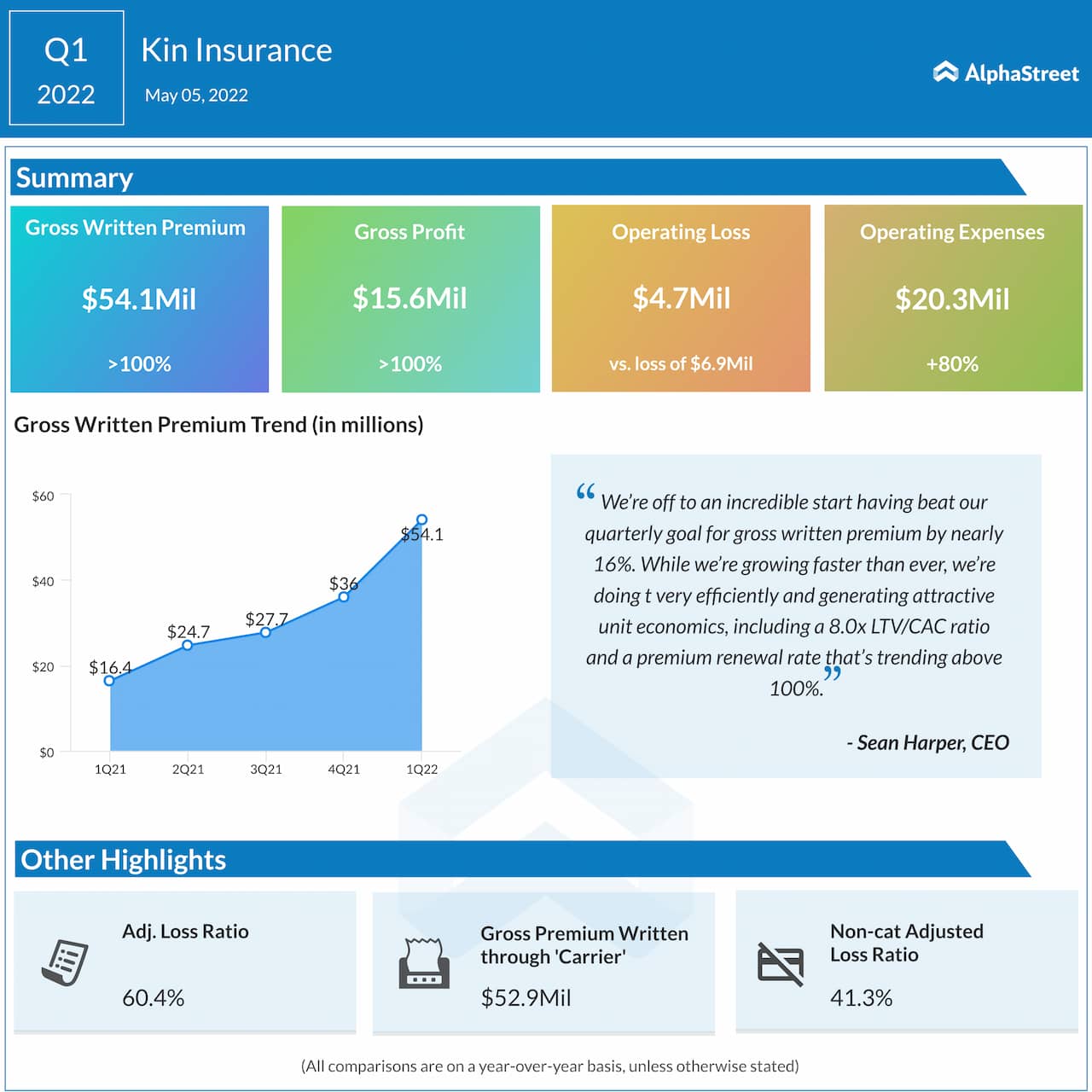

Finally, our unit economics are very strong, including an 8.0x LTV to CAC ratio. Our CAC is extremely efficient because we target customers that fit our underwriting profile, and we focus on customer satisfaction to drive conversion and organic referrals. Our premium renewal rate this year is trending >100% (97% in 2021) and drives higher lifetime value along with the efficient CAC. Also, 100% of our customers have a direct relationship with us.

Do you expect the positive momentum seen in Q1 to continue in the coming quarters, and how do you look at your profitability goals now?

We’ve benefited from the hard work of every employee at Kin to break all-time records for new business production and premium retention rates in Q1, while significantly improving our unit economics. Kin’s early success will enable us to focus more on decreasing our loss ratio and accelerate our path to profitability.

Furthermore, our competitors are having a very hard time maintaining sustainable businesses in catastrophe-exposed states, which is creating abundant opportunities for us. The most successful companies are the ones that have good fundamentals and can adapt, so we’re going to monetize this opportunity by hitting our premium target and crushing our profitability metrics, the most important of which is loss ratio.

What is your growth strategy for the long term, and how do you see the home insurance market evolving in these uncertain times?

The home insurance industry needs to be able to quickly respond to changes in climate, tech, and consumer preferences. However, legacy insurers have been slow to respond to change, instead relying on decades-old tech and primarily selling through expensive agent distribution channels. The results are unhappy customers, bloated cost structures, and low profit-margin insurance companies.

Kin has created a better way. We’re making home insurance more convenient and affordable by cutting out administrative and agent-related expenses. Customers receive a direct, frictionless experience through our technology platform, which instantly draws on thousands of data points to evaluate the risk profile of each home and price policies accurately. This is particularly important for homes that are hard to insure, including those that are impacted by severe weather events caused by climate change. Kin, equipped with good algorithms and quality data, can operate in high-risk places and help customers prepare for the worst and recover quickly when it happens.

ALSO READ: Trxade is increasing the breadth of product offerings: CEO Suren Ajjarapu

Our strategy remains focused on growing in catastrophe-exposed states, where the insurance market is fragmented; either the legacy carriers don’t have a major presence or the smaller carriers have very little brand recognition.

Lastly, where do you see Kin Insurance five years from now?

We recently acquired an inactive insurance carrier that has licenses in 43 states. We are recapitalizing that carrier and converting it into a reciprocal exchange, which will give us the ability to serve customers in most of the remaining states which constitute, in aggregate, the $110 billion home insurance market. Beyond that, with our financial metrics and unit economics holding strong, we’re focused on becoming profitable and reaching $1 billion in premium in the next few years. We have the capital needed to achieve the scale we want, the right structure to drive profitable growth, and a solid business to generate shareholder value over the longer term.