The American housing market has been resilient to the coronavirus-related disruption, and more recently the economic uncertainties. While inflation and interest rate hikes are putting pressure on sales, homebuilder Lennar Corporation (NYSE: LEN) is witnessing stable demand amid tight supply.

The Miami-headquartered construction company’s stock has been performing quite well ahead of next week’s earnings, and it reached an all-time high last week. Earlier, LEN recovered in the second half of last year after a slump and shifted to growth mode. Extending the uptrend, it made stronger gains this year and constantly stayed above the long-term average.

The stock

Lennar has raised its dividend almost every year in the past, though moderately, and offers a yield of 1.5% now. But it might not be the right time to buy the stock now, due to the relatively high valuation. The market will be closely following Wednesday’s earnings report and the management’s comments, looking for updates on the market trends and the company’s future plans.

Prospective buyers tend to put their purchases on hold, concerned about economic uncertainties, but the high demand due to the short supply of new housing units indicates that the market would bounce back once external conditions become favorable. And, sales would stabilize once issues like supply chain disruption, high raw material costs, and labor shortage improve.

Market Trend

While sales fluctuations can be attributed to the cyclical nature of the housing industry to some extent, in the long term the market is expected to thrive on positive factors like the rising population and the relatively strong mortgage market. It should be noted that Lennar’s gross margins and cash flows have been quite healthy, lately.

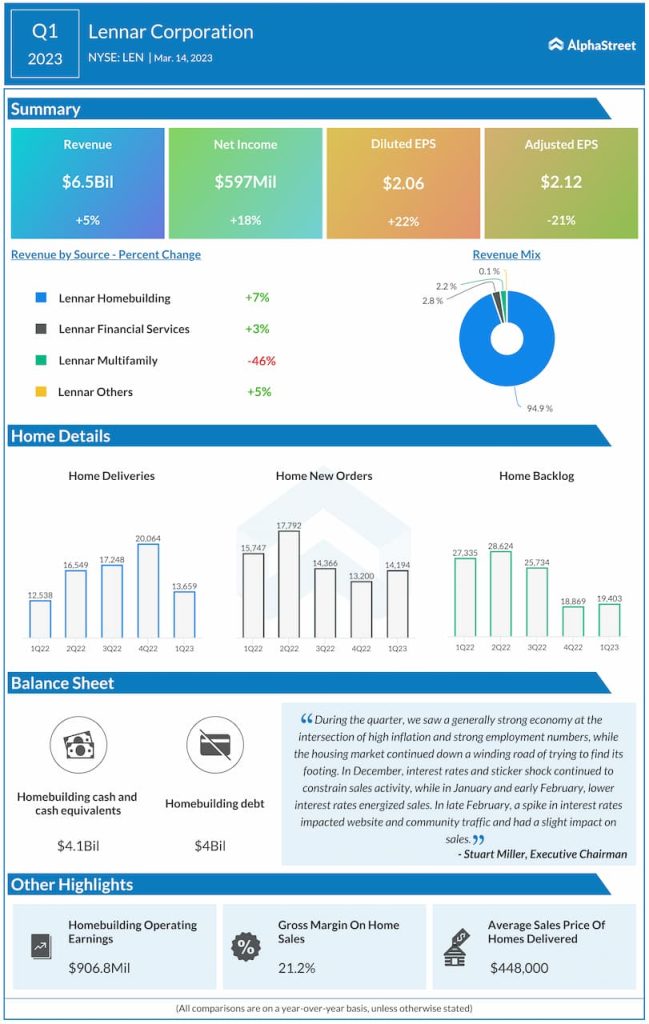

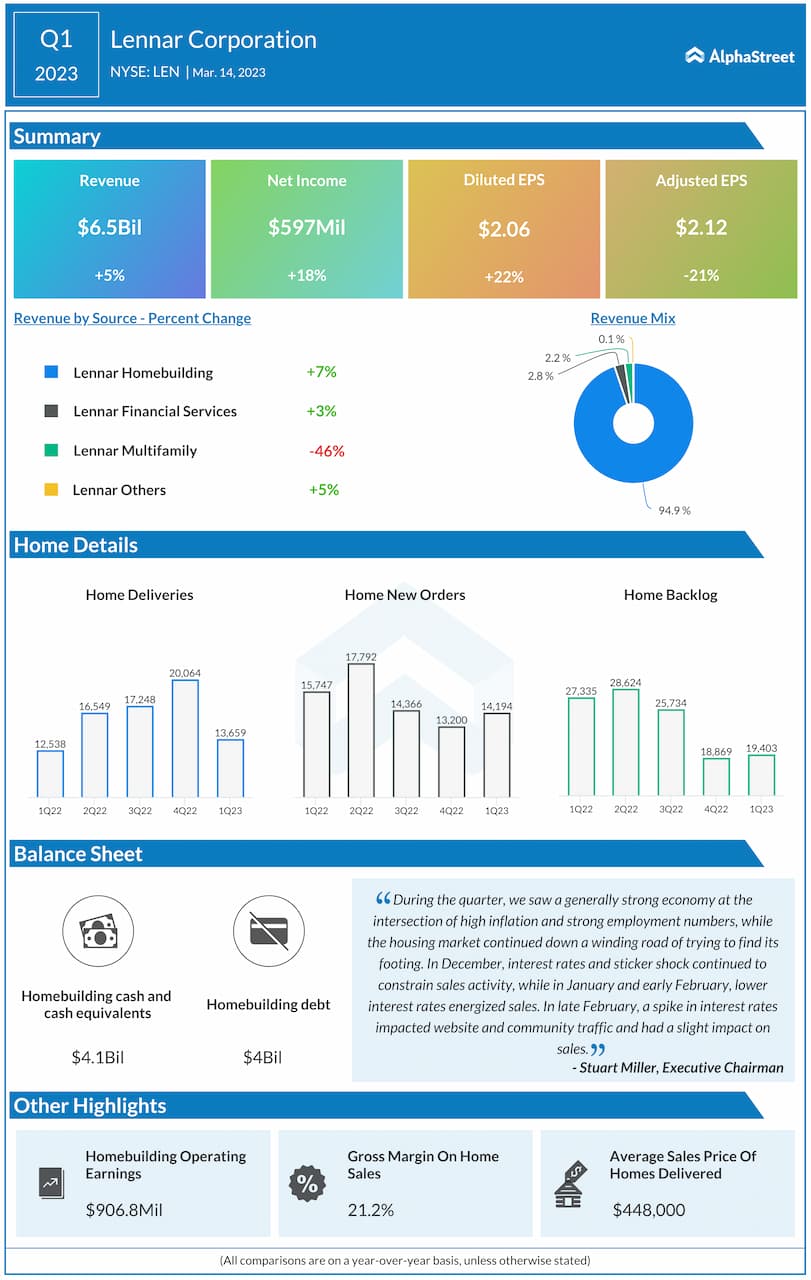

From Lennar’s Q1 2023 earnings call:

“With volume and production as our constant and margin as our shock absorber, we manage with certainty through volatility and stay focused on our mission. If market conditions deteriorate, we compromise margin through price and/or incentives, but we generate strong cash flow. If conditions improve, we improve the margin and bottom line while also generating strong cash flow. Our primary focus is on cash flow. We maintain our volume to move through the limited legacy land that we have, which is at legacy prices while keeping our production machine working efficiently and rationalizing costs.”

Q2 Report on Tap

Lennar will be reporting second-quarter results on Wednesday, at 5:00 PM ET. Analysts’ consensus estimate is for a 49% fall in earnings to $2.31 per share in the latest quarter when revenue is expected to decline by double-digits to $7.17 billion. In the past, Lennar’s earnings performance has been impressive, with quarterly numbers topping expectations consistently for more than a year.

In the first quarter, adjusted profit dropped despite a modest increase in revenues to about $6.5 billion. The bottom line came in at $2.12 per share, down 21% year-over-year. The main business segments, including Homebuilding which accounts for around 95% of total revenues, grew in the February quarter. Revenue, however, fell short of expectations.

Lennar’s stock has maintained an uptrend so far this year. It opened Monday’s session higher and made modest gains in the early hours.