Shares of The J.M. Smucker Co. (NYSE: SJM) were down over 4% on Wednesday after the company reported its earnings results for the first quarter of 2025 and lowered its guidance for the full year. The top line matched estimates while the bottom line beat expectations. However, the company cut its guidance as it continues to face a challenging consumer environment.

Earnings beat, sales in-line

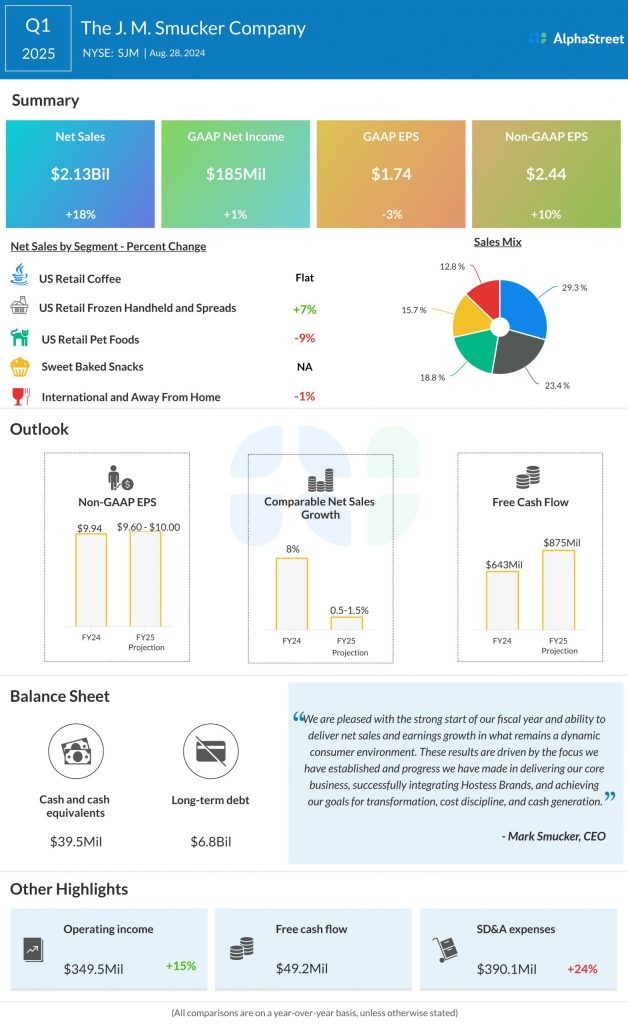

Net sales increased 18% year-over-year to $2.13 billion in Q1 2025, in line with estimates. Comparable sales increased 1%. GAAP EPS fell 3% to $1.74. Adjusted EPS rose 10% to $2.44, beating projections of $2.17.

Inflationary pressures impact demand

In Q1, sales in the US Retail Coffee segment remained flat compared to the prior-year period, as lower pricing was offset by favorable volume/mix. The coffee category continues to be impacted by inflation, and in response to higher green coffee costs, SJM plans to roll out another list price increase in October. Despite these near-term pressures, the company expects the coffee category to remain resilient.

Sales in US Retail Frozen Handheld and Spreads rose 7%, helped by gains in Uncrustables sandwiches and the Jif brand. Uncrustables net sales grew by 24% at the total company level. Net sales for the Jif brand increased 4% in the quarter, helped by the recent launch of Jif Peanut Butter & Chocolate Flavored Spread.

US Retail Pet Foods sales fell 9% in Q1. Sales growth in Meow Mix cat food was offset by declines in Canine Carry Outs and Pup-peroni dog snacks, as the dog snacks category continues to be impacted by a reduction in discretionary spending caused by inflationary pressures. The Milk-Bone brand benefited from growth in soft and chewy snacks.

The Sweet Baked Snacks segment delivered lower-than-expected sales in the first quarter, as inflationary pressures and reduced discretionary income impacted the sweet baked goods category and caused a reduction in convenience store foot traffic. Long-term, snacking trends remain favorable.

Guidance cut

Against the backdrop of a dynamic consumer environment, SJM lowered its guidance for the full year of 2025. Inflationary pressures and lower discretionary income are negatively impacting the dog snacks and sweet baked goods categories. The outlook also reflects the anticipated impacts of demand elasticity within the coffee portfolio due to price increases taken in response to higher than expected green coffee costs.

The company now expects net sales to increase 8.5-9.5% from the prior year. The earlier expectation was for a growth of 9.5-10.5%. Comparable sales are expected to increase 0.5-1.5% as opposed to the previous outlook of 1.5-2.5%. Adjusted EPS is now expected to be $9.60-10.00 versus the prior range of $9.80-10.20.