PayPal Holdings Inc. (NASDAQ: PYPL) has been a dominant player in the payments market, and the business got a major boost from the mass shift to digital payments during the pandemic. Taking a cue from the growing competition and changing trends in the payments landscape, the company is ramping up its platform and introducing new features to enhance customer experience.

PayPal delivered stable revenue performance in the first half, continuing the long-term trend, but profitability has remained under pressure due to weak margins. PYPL has been among the worst-performing Wall Street stocks lately. The recent market selloff added to the troubles of the stock which entered a losing streak after hitting an all-time high two years ago.

Stock Falls

The shares lost a dismal 81% during that period and are currently trading below the 52-week average. Though PayPal’s Q2 earnings topped expectations, investors were worried about the sequential decline in user numbers and weaker-than-expected operating margins, which triggered a stock selloff. The low valuation offers a good buying opportunity because the payment industry is expected to expand steadily in the coming years. Prospective buyers might not get a chance to own the stock at a lower price in the near future.

PayPal delivered peak performance during the pandemic when people shifted to digital payments en masse, but growth slowed as the market started opening. The company announced a major headcount reduction early this year that affected around 7% of its total workforce, as a cost-cutting measure in the wake of the economic downturn.

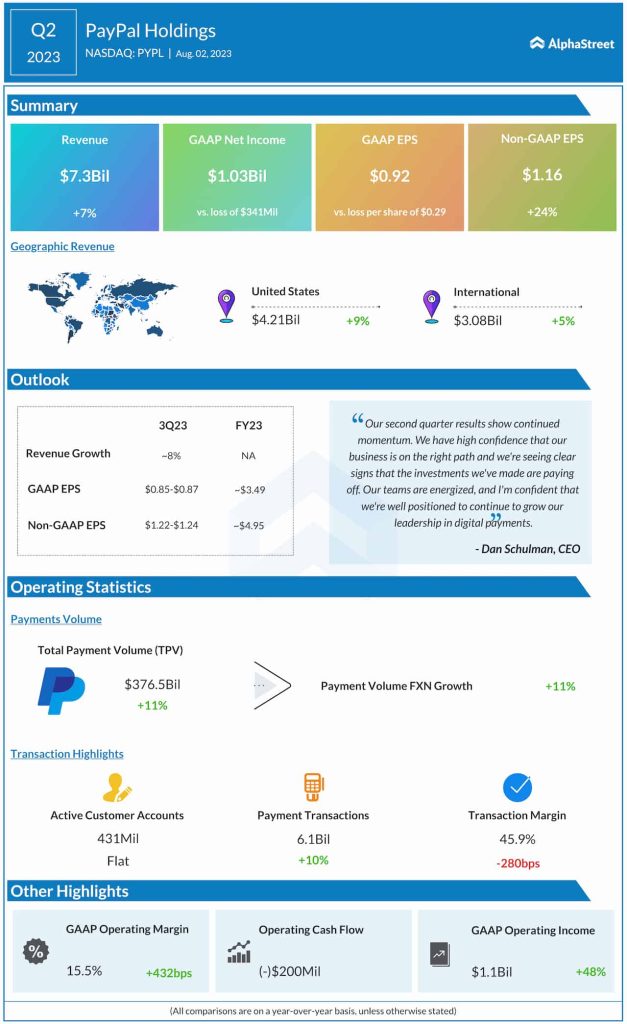

Mixed Results

The company’s key financial metrics – earnings and revenues – beat estimates for the fifth consecutive quarter, and it ended the first half of 2023 on a positive note. Second-quarter profit, adjusted for special items, increased by a quarter to $1.16 per share. That reflected a 7% growth in revenues to $7.3 billion – revenue rose in both domestic and international markets. Total payment volumes climbed 11% annually to $376.5 billion. For the September quarter, the management predicts an 8% revenue growth, which would translate into adjusted earnings of $1.22-$1.24 per share. The estimate for full-year adjusted profit is approximately $4.95 per share.

From PayPal’s Q2 2023 earnings call:

“As we look ahead to the rest of 2023 and into 2024, we expect to drive meaningful productivity improvements. Our initial experiences with AI and continuing advances in our processes, infrastructure, and product quality, enable us to see a future where we do things better, faster, and cheaper. These overall cost savings come even as we significantly invest against our three strategic priorities. We know exactly what we need to do as we look towards 2024. And as you can see in our results, we are beginning to see the fruits of our labor.”

New CEO

Recently, the company appointed Alex Chriss as the new president and chief executive officer. Alex succeeds Dan Schulman who will be retiring effective December 31, 2023. Schulman will remain on the company’s board until the next annual meeting of stockholders to be held in May 2024.

The market was not impressed by PayPal’s Q2 report early this month, and the stock suffered a fall soon after the announcement. Extending the downtrend, PYPL traded sharply lower in the early hours of Thursday’s session.