Shares of Pinterest Inc. (NYSE: PINS) were down 3% on Monday. The stock has dropped 38% year-to-date and 69% over the past 12 months. While the general sentiment around the stock is rather pessimistic, not all are willing to give up on it. Here are a few points to keep in mind if this stock is on your radar:

Pros

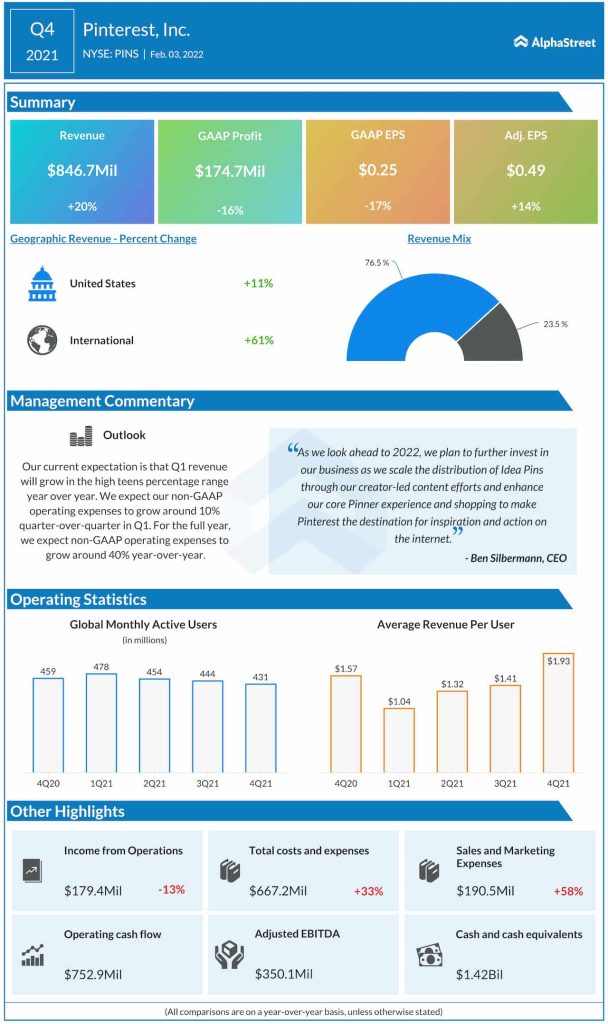

Pinterest’s revenue for the fourth quarter of 2021 grew 20% year-over-year to $847 million and surpassed market expectations. The top line growth was driven by strong demand from retail advertisers. Revenues in the US grew 11% while international revenue rose 61% YoY, driven by growth in average revenue per user (ARPU). The company managed to grow revenue despite a decline in users.

Global ARPU grew 23% YoY to $1.93, driven mainly by advertising demand. US ARPU increased 25% YoY to $7.43 while international ARPU rose 62% to $0.57. The company is working on expanding its advertiser base in regions outside the US. It is also rolling out its shopping feature in international markets and believes there is scope for meaningful growth here. In Q4, catalog uploads were up over 400% YoY in international markets.

On an adjusted basis, earnings were up 15% YoY to $339 million, or $0.49 per share. Looking ahead, the company expects revenue in the first quarter of 2022 to grow in the high teens percentage range year-over-year.

Cons

The biggest cause of concern for Pinterest is its ongoing decline in users. At the end of Q4, global monthly active users (MAUs) stood at 431 million, which reflected a decline of 6% from the prior-year quarter. In the US, MAUs dropped 12% YoY to 86 million while international MAUs decreased 4% YoY to 346 million.

This decline was mainly due to the easing of pandemic restrictions and people going back to their normal routines, as well as lower search traffic due to the changes that Google made to its algorithm in November. Pinterest is also facing tough competition from other video apps in terms of engagement.

In the US, MAUs coming to Pinterest from desktop and mobile web declined around 30% YoY while those coming from mobile apps declined around 6% YoY. The decline in Pinterest’s global MAUs has been ongoing for the past couple of quarters and this is a key reason why analysts have a pessimistic outlook on the company’s prospects.

However, during Q4, engagement trends began to normalize. On its conference call, the company stated that the propensity of Pinners to adopt use cases like home decor or cooking in Q4 2021 was similar to the trends seen in Q4 2019.

Looking ahead, the company believes the pandemic unwind will be a less meaningful engagement headwind as it moves through 2022, particularly after mid-March when it will begin to lap the widespread easing of restrictions. However, engagement headwinds from algorithm changes and competing platforms are more persistent and could disrupt normal seasonal trends. As of February 1, US MAUs were around 86.6 million and global MAUs were around 436.8 million.

While some analysts continue to retain optimism towards this stock, others prefer to take a more cautious approach.

Click here to read the full transcript of Pinterest’s Q4 2021 earnings conference call