The semiconductor industry is a rapidly growing business segment that currently thrives on the digital transformation wave. The demand for memory chips and other semiconductor products increased over the years, but the cyclical nature of the business often creates uncertainty. Currently, chipmakers like Micron Technology, Inc. (NASDAQ: MU) are going through a rough patch despite the high demand.

The Boise-based memory chip giant’s lackluster fourth-quarter report is reflective of the slowdown the sector is experiencing, and the sharp fall in earnings and revenues came as a disappointment for investors. But the company’s stock bounced back quickly from the post-earnings dip, paring a part of the recent losses. It looks like MU is on the recovery path, and experts see the uptrend extending into next year and the stock moving close to its long-term average.

The Stock

It would be unfair to judge the stock’s growth potential on the basis of short-term challenges. Micron has managed to come out with relatively strong quarterly earnings over the past several years, with the numbers regularly beating estimates.

Micron Technology Q4 2022 Earnings Call Transcript

Also, the company’s balance sheet and cash position are healthy, though free cash flow might come under pressure from investments being done to overcome the market challenges. It’s a fact that the stock has come down to attractive levels, but one should stay patient and the investment approach should be cyclical to take advantage of the opportunity. While MU is as compelling a buy as ever, the volatile market conditions and economic uncertainties should be taken into consideration before buying/selling.

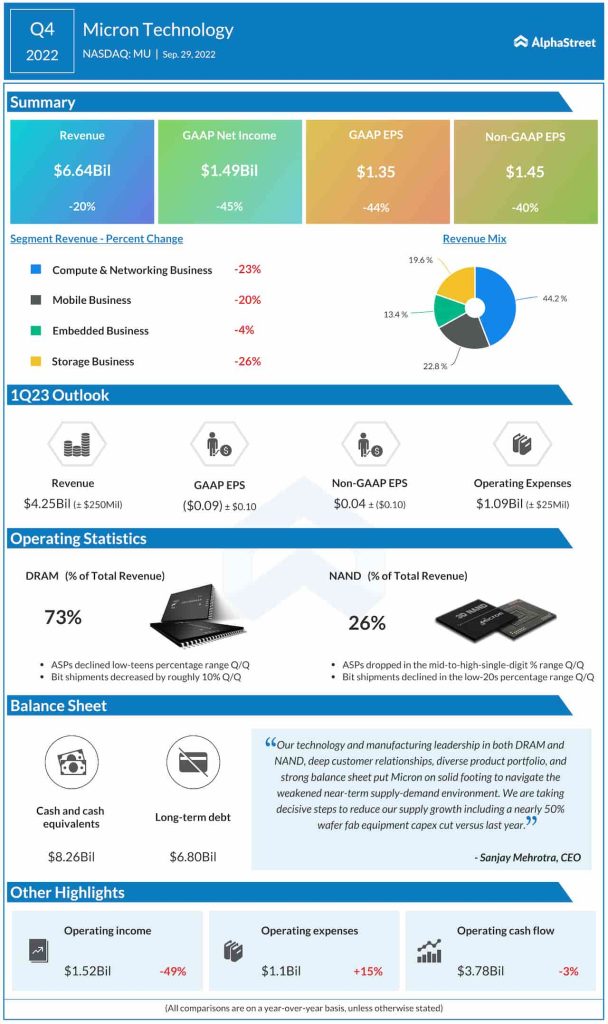

In the final three months of fiscal 2022, all four operating segments contracted, resulting in a 20% fall in revenues to $6.64 billion. Consequently, adjusted profit dropped 40% annually to $1.45 per share. The bottom line was also hurt by a double-digit increase in operating expenses. Earnings surpassed estimates, while revenues missed. DRAM products accounted for nearly three-fourths of total sales.

Road Ahead

It is almost certain that the Fed’s monetary policy would remain tight in the near future. Micron’s management is taking steps to ease the impact of inflation on financial performance, with a focus on cutting costs like high-value investments in semiconductor fabrication equipment. The cautious outlook for the first quarter, projecting near-breakeven earnings and a sharp fall in revenues, dampened market sentiment. The recovery will be slow and the high inventory levels would cause memory prices to decline.

From Micron’s Q4 2022 earnings conference call:

“Calendar 2022, industry bit demand growth for DRAM is now expected to be in the low-to-mid single-digit percentage range, and for NAND, slightly higher than 10%. An unprecedented confluence of events has affected overall demand, including COVID-related lockdowns in China, the Ukraine war, the inflationary environment impacting consumer spending, and the macroeconomic environment influencing customers’ buying behavior in multiple segments.“

Where to invest as the semiconductor industry enters a new era

MU traded higher throughout Friday’s session, after recovering from the dip that followed the earnings release. The stock has lost around 35% in the past six months.