Like most tech companies, DocuSign, Inc. (NASDAQ: DOCU) successfully leveraged the widespread adoption of digital technology in the last two years but the momentum slowed in recent months and the e-signature firm is currently enhancing its go-to-market capabilities to boost sales.

The San Francisco-headquartered company’s stock is trading at the lowest level in more than two-and-half years, with most of the losses coming this year. The stock, one of the worst affected by the recent sell-off, further declined after last week’s earnings report. The mixed first-quarter results and the management’s weak outlook call for caution as far as investing in DOCU is concerned, though the stock is expected to make strong gains in the long term – experts see double-digit growth in 12 months.

Hold It?

It is not a good time to either buy or sell the stock, rather keeping an eye on it would help investors take the right decision at the right time. The fact that the company does not pay dividends, and dilutions due to heavy stock-based compensations make it less attractive. But DocuSign is unlikely to disappoint long-term investors since the digital shift is likely to accelerate further irrespective of market challenges. Having gained about 70% of the e-signature market share, supported by a rapidly growing subscriber base, DocuSign’s long-term prospects look bright.

Read management/analysts’ comments on quarterly reports

The company recently launched what it calls CLM Essentials, which allows customers to get started with Contract Lifecycle Management in a hassle-free manner. It has also expanded the global strategic partnership with Microsoft Corp. (NASDAQ: MSFT) to offer new DocuSign Agreement Cloud integrations and capabilities across Microsoft’s business solutions. DocuSign is on track to further expand the portfolio in the coming months with additional offerings. In an effort to balance growth and profitability, the management is streamlining the business through initiatives like slowing down hiring.

“We’re confident in our strategy and path to becoming a $5 billion revenue company. DocuSign continues to be the clear market leader in the electronic signature space, and we are excited about our progress in defining the broader Agreement Cloud category as well. Our dedication to innovation and our investments in attracting high-caliber talent position us to build upon our leading market share,” said DocuSign’s CEO Dan Springer at the post-earnings meet.

The economic uncertainty from the Ukraine war and other macro challenges, including elevated inflation, is putting pressure on sales, especially in Europe where the company has a strong presence. Another challenge facing the company is growing competition from Adobe Sign and HelloSign, which is owned by Dropbox, Inc. (NASDAQ: DBX).

Mixed Results

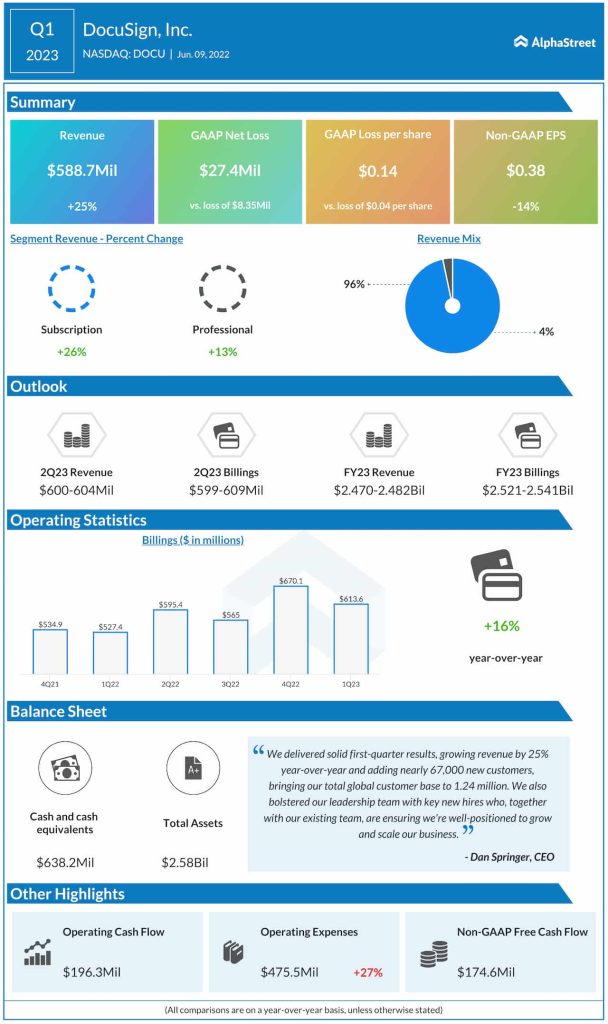

After beating estimates in every quarter since mid-2019, DocuSign’s earnings missed expectations in the most recent quarter. Unadjusted profit slipped to $0.38 per share in the first quarter of 2023 from $0.44 per share last year. On the other hand, revenues rose to $589 million amid strong billings growth, supported by a double-digit increase in the core subscription business. However, the management sees sales growth decelerating in the coming quarters.

Should you buy Oracle stock ahead of next week’s earnings?

DocuSign’s stock closed the last trading session slightly above $60, which is down 80% from the all-time highs of September 2021. The current valuation is also far below the long-term average.