Shares of Target Corporation (NYSE: TGT) rose over 1% on Thursday. The stock has dropped over 11% in the past one month. The company delivered mixed results for the first quarter of 2024, as earnings missed estimates while revenue came in line. Here’s a look at the retailer’s performance in Q1:

Quarterly numbers

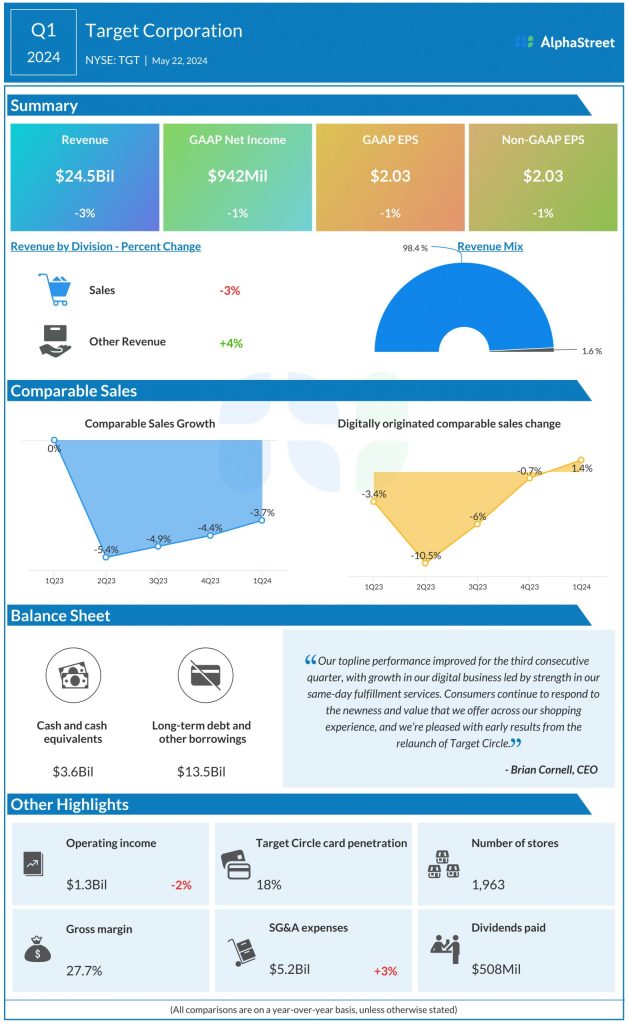

Target delivered mixed results for the first quarter of 2024 and both its top and bottom line numbers declined year-over-year. Total revenue decreased 3.1% to $24.5 billion, but were in line with estimates. The company reported GAAP EPS of $2.03. Adjusted EPS of $2.03 was down 1% from last year and below projections.

Business performance

In Q1, Target’s comparable sales declined 3.7%, driven by a 1.9% drop in traffic. Average transaction was also down 1.9%, as customers remained cautious in their spending, especially on discretionary purchases.

On its quarterly conference call, Target said that consumers have remained resilient against a challenging backdrop of high prices and interest rates, which has nevertheless taken a toll on budgets and savings. In such an environment, customers continue to search for value and in order to aid them, the retailer said it cut prices on a large number of items in its food and essential categories.

During the first quarter, Target saw continued softness in discretionary categories such as home and hardlines, as well as softening trends in frequency categories, with lower unit volume and less benefit from pricing versus a year ago. In this tough environment, the beauty category delivered low-single digit growth, helped by gains in skincare and personal care. The company expects discretionary trends to remain pressured in the short term but to normalize over time.

Target saw an increase in digital sales in Q1, driven by same-day services, Drive Up, in-store pickup and same-day delivery. Same-day services recorded high-single-digit growth, led by Drive Up, which saw growth in the low teens.

Gross margin improved by 140 basis points to 27.7% in Q1, helped by cost improvements that more than offset higher markdowns, and favorable category mix. The increase also included 20 basis points of benefit from inventory shrink. On its call, Target said it continues to believe that shrink rates are positioned to reach a plateau this year.

Outlook

For the second quarter of 2024, Target expects comparable sales to increase 0-2%, and GAAP and adjusted EPS to range between $1.95-2.35. For the full year, the company continues to expect a 0-2% growth in comparable sales, and GAAP and adjusted EPS of $8.60-9.60.