For Tesla Inc. (NASDAQ: TSLA), expanding production capacity and launching new vehicle models has been a continuous process that enabled it to emerge as the largest electric vehicle maker. But currently, the company is focused on making its vehicles more affordable by reducing prices amid concerns of demand being hit by interest rate hikes and rising competition.

Tesla’s stock tanked this week despite the EV giant reporting strong numbers for its latest quarter, reflecting the market’s concerns over the company’s shrinking margins due to recent price cuts. TSLA has lost about 12% since the announcement, after making consistent gains in recent weeks. At the same time, the value has more than doubled since the beginning of the year. The company has hinted at continued margin pressure in the near term as it might go for more price cuts to sustain demand.

The Stock

That’s not good news for the stock because a lot of investors would be making their buying and selling decisions based on short-term outlook on the company’s performance. Meanwhile, margins are expected to bounce back as market conditions improve – possibly as early as in the back half of the year — because the demand for Tesla vehicles remains strong including the recently launched Cybertruck.

The first Cybertruck was rolled out from the Texas plant earlier this month — an ambitious project by CEO Elon Musk to reshape the truck industry. Recently, Musk exuded confidence in meeting the target of shipping around 1.8 million vehicles this year. When it comes to market share, Tesla is far ahead of its nearest rival, and that puts it in an advantageous position. Also, the company’s technological prowess makes it a frontrunner in the incorporation of advanced AI systems in automobiles, especially in the robot-taxi segment of the business.

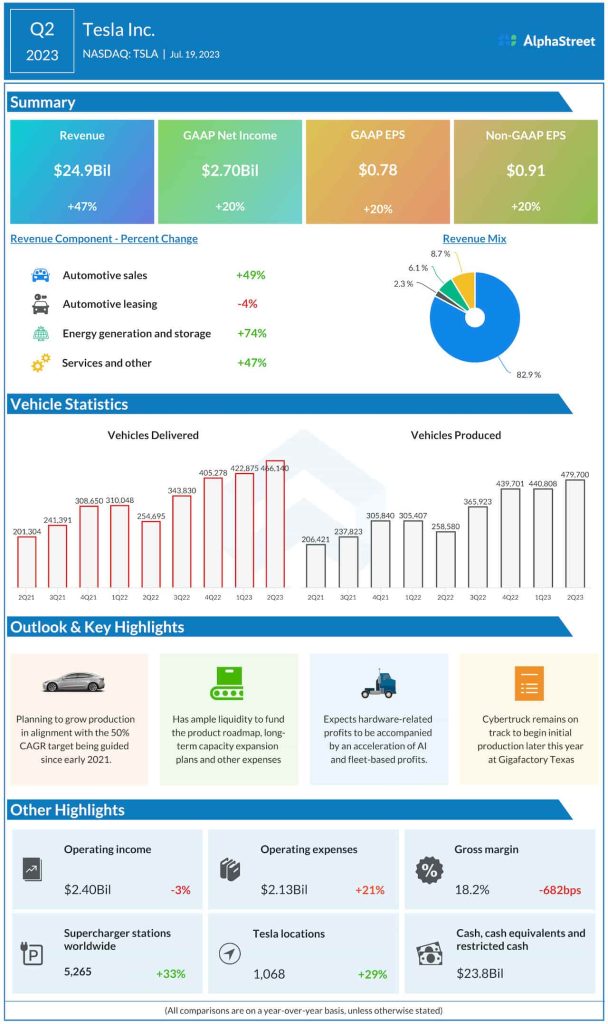

Record Production

Interestingly, Tesla’s revenues jumped 46% in the second quarter but its gross margin slipped to 18.2%, marking the third decline in a row. Total vehicle production and deliveries rose to record highs of 479,700 units and 466,140 units respectively. The energy and services segments also performed well during the quarter. Earnings and revenues also beat estimates by wide margins. Operating income declined modestly, mainly due to costs related to production ramps, the Cybertruck project, and AI initiatives, as well as the impact of unfavorable foreign exchange rates.

From Tesla’s Q2 2023 earnings conference call:

“If we look specifically at our automotive business, our gross margin showed a modest reduction and remained healthy, despite action taken to further improve vehicle affordability early in the quarter. We recognized — we realized per unit cost improvements in nearly every category, including material cost and commodities, manufacturing costs, and logistics, while also continuing to rapidly increase the build rate in our Austin and Berlin factories. For our energy business, we improved margins and gross profit driven by cost reductions and deal economics, particularly with Megapack.”

Extending the post-earnings downturn, shares of Tesla traded down 2% on Friday afternoon, after closing the previous session lower.