It is not surprising that web hosting company GoDaddy, Inc. (NYSE: GDDY) witnessed a spike in subscriptions after the shelter-in-place orders came. Like many of its peers in the tech space, the company is cashing in on the rapid adoption of digital technology across sectors – a trend that is likely to continue.

[irp posts=”68180″]

Rarely do we see so many experts recommending a stock as in the case of GoDaddy — almost everyone following it. Analysts overwhelmingly recommend buying, and the stock‘s outstanding performance justifies that. Going by the average target price, it is pretty close to breaking through the $100-mark, after nearly doubling the value since the COVID-driven selloff a few months ago.

Strong Buy

Most investors would find the present value attractive, especially those looking for long-term engagement. It is worth noting that the Maryland-based domain name registrar’s return on equity was quite high last year, and the healthy cash flow would allow it to further increase shareholder value. Also, bookings and revenue per user have grown consistently over the years.

Enterprises with a limited online presence now want to expand their digital prowess. It goes without saying that having a website gives companies a significant advantage, at a time when e-commerce growth and the prevalence of remote work are transforming the way businesses operate.

Digital Push

Once considered a drawback, small businesses that account for the lion’s share of GoDaddy’s clientele have turned out to be boon for the company, thanks to the huge capital they represent. It is quite natural for lower-tire companies to turn to non-traditional avenues to generate revenue, and the internet is the best platform for that. In other words, it has become impossible to do business in many sectors without online support. The management thinks GoDaddy is well-positioned to tap the opportunity.

Concerns Linger

On the flip-side, there are concerns that the company’s pricing model is not customer friendly – something that needs to be addressed considering the increasing competition in the field of web hosting. In a sign that even high-demand areas like internet services are not immune to the pandemic, GoDaddy recently laid off certain members of its sales team as part of an organizational restructuring.

Meanwhile, the marketing strategy remains intact and the management plans to continue investing in its marketing efforts while also upgrading the products by incorporating new features like video streaming and online shopping. Synergies from the recent buyout of Neustar’s domain registry arm should support those initiatives. Being the largest WordPress host, GoDaddy has added new capabilities to the former’s ecosystem, thereby creating a win-win situation.

Record Additions

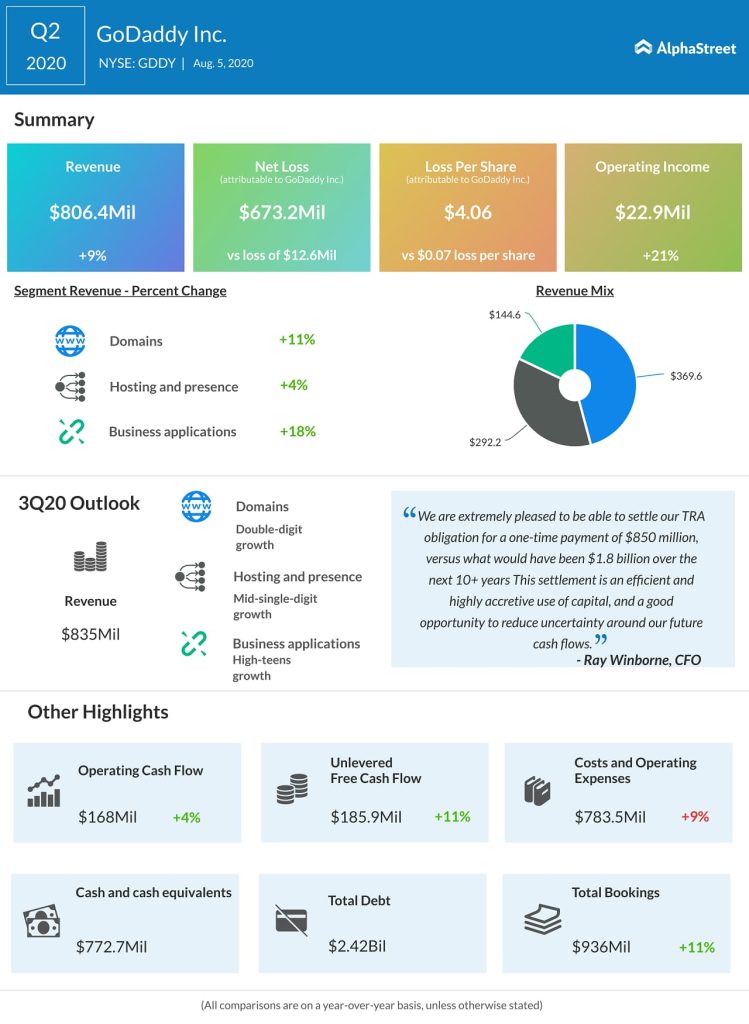

The company ended the most recent quarter with more than 20 million paying customers, aided by record new additions. That, combined with flat churn rates and stable subscription renewals, resulted in double-digit revenue growth across business units. The top-line increased by 9% and beat estimates. Since the momentum gathered steam in the final weeks of the quarter, the management issued future guidance that exceeds expectations. However, the impressive revenue performance did not translate into profit, due to a one-time payment related to a tax settlement.

“We saw growth in Domains. So it’s not really about one product or the other. We’re seeing growth across all products, and it’s a function of the demand environment and the marketing spend and the value that our products bring to our customers on sort of everyday basis,” said chief executive officer Aman Bhutani during the earnings conference call.

Read management/analysts’ comments on GoDaddy’s Q2 2020 earnings

The stock’s recent performance has been in line with, or even better than, that of the technology sector. After rebounding quickly from the March mayhem, the shares have risen above the pre-crisis levels and are currently hovering near the record highs seen a couple of years ago. They have gained 14% in one month alone.