Weibo Corporation (NASDAQ: WB) is set to report its third-quarter 2019 earnings results on Thursday before the market opens. The top line will be benefited from advertising and marketing while gaming could hinder growth. The bottom line, meanwhile, will be hurt by higher costs and expenses arising from the investments in the creation of content.

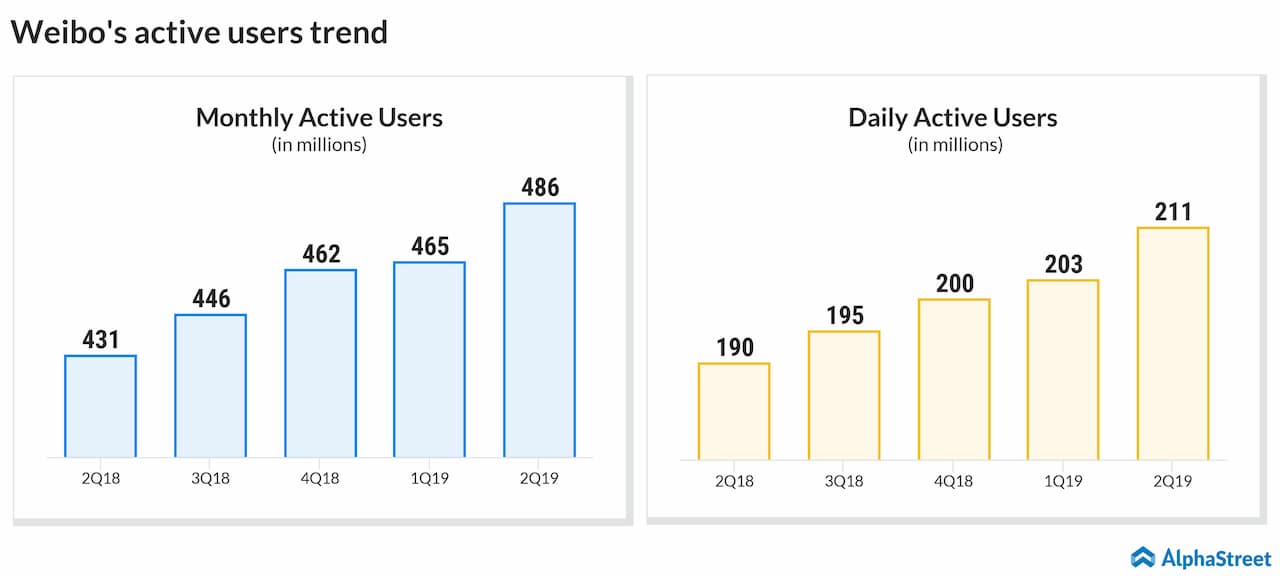

For the third quarter, Weibo estimates net revenues to increase 6-9% year-over-year on a constant currency basis. The company has been relishing an increase in engagement by the users. However, this is likely to decline in the future as users are shifting from microblogs to specific social media platforms such as WeChat and ByteDance.

The company will also be impacted by the soft advertising market, falling engagement, and competitive pressure from private short-video platform players. The cost optimization has been a crucial part of Weibo since the past year as the company is looking into ways to achieve improved margins.

Also, Weibo has been struggling to catch the attention of the people as there remained a decelerating trend seen for the Weibo main app. The company has been facing immense competition from short-form videos platform ByteDance and Kuaishou while TikTok is turning into the fastest growing media app in China in terms of active users.

Both the platforms are likely to turn public next year. This is likely to hinder the growth of Weibo in the social media platform. The people have turned towards short-form video as it can deliver a more robust and entertaining content than microblogs. This can be seen from the diminishing trend of the Weibo microblog and in turn, hurt the engagement metrics and revenue growth.

Read: Baidu Q3 earnings review

Analysts expect the company’s earnings to decline by 2.70% to $0.73 per share while revenue will rise by 1.70% to $468.07 million for the third quarter. The company has surprised investors by beating analysts’ expectations in all of the past four quarters. The majority of the analysts recommended a “buy” rating with an average price target of $53.25.

For the second quarter, Weibo posted a 27% drop in earnings due to higher costs and expenses despite a 1% rise in total revenues. The growth in the live streaming business drove the top line higher and partially offset a decline in gaming revenue and unchanged advertising and marketing revenues.

Listen to on-demand earnings calls and hear how management responds to analysts’ questions