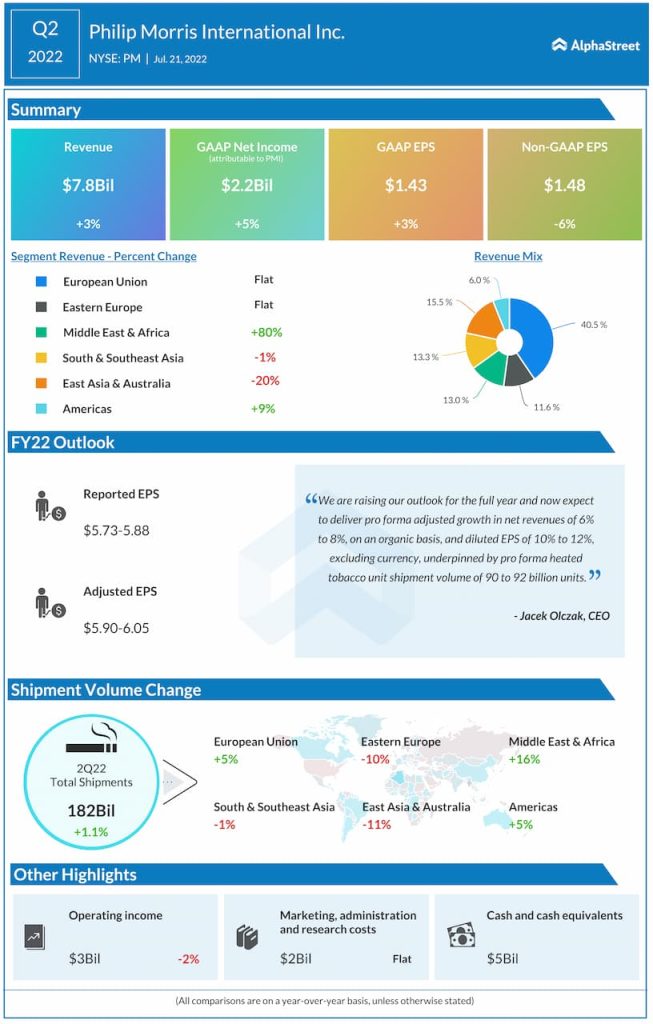

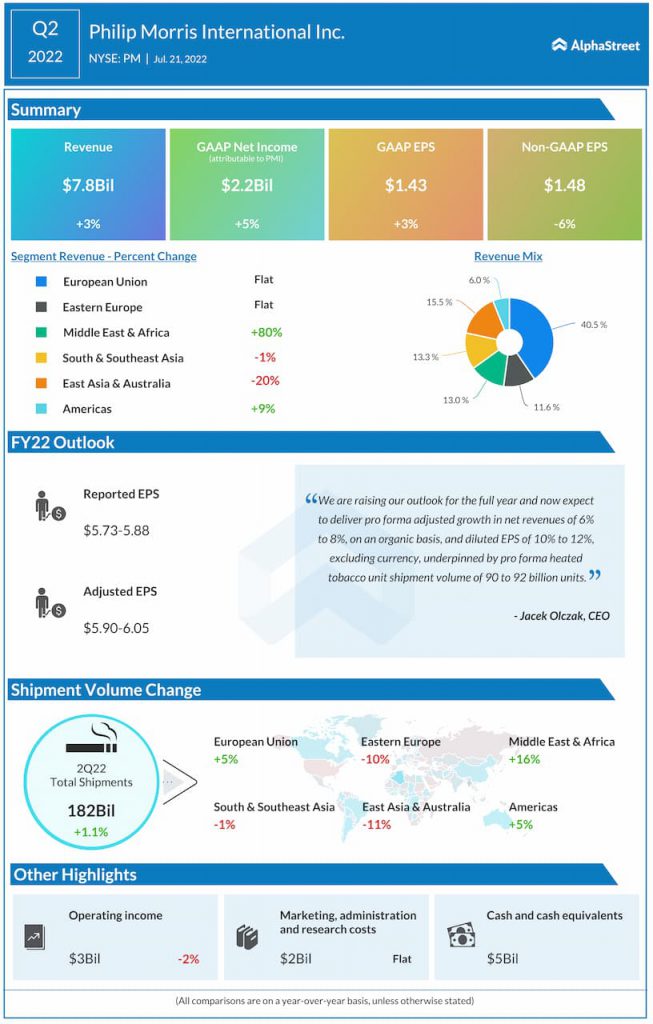

Shares of Philip Morris International Inc. (NYSE: PM) were down 1% on Thursday. The stock has dropped over 9% year-to-date. Although the tobacco industry has felt the pinch of inflation, the addictive nature of cigarettes has kept demand relatively stable for Philip Morris’ products. The company is also benefiting from its investments in smoke-free products such as IQOS. Here’s a look at the company’s expectations for the near term:

Revenue

In the second quarter of 2022, Philip Morris recorded a growth of 6.2% in its pro forma adjusted net revenues on an organic basis. This was driven by pro forma total shipment volume growth of 3%, helped by a 2.4% increase in cigarettes and a 7.4% increase in heated tobacco units.

Pro forma adjusted net revenue per unit rose by 3% on an organic basis, reflecting a higher proportion of heated tobacco units in the sales mix and higher pricing. Pro forma pricing for combustible products increased by 3.5% in Q2.

For the full year of 2022, pro forma adjusted net revenues are expected to grow approx. 6-8% on an organic basis. For the third quarter of 2022, pro forma net revenue is expected to grow in mid-single digits on an organic basis.

Profitability and margins

In Q2, Philip Morris delivered reported EPS of $1.43, which was up 3% year-over-year. Adjusted EPS amounted to $1.48 while pro forma adjusted EPS totaled $1.32, reflecting currency-neutral growth of 3.8% and 5.6% respectively.

Pro forma adjusted operating income margin declined by 1.9 points on an organic basis during the quarter, mainly due to investments in the smoke-free portfolio, supply chain disruptions, cost inflation, and a tough comparison to the prior year which included substantial productivity savings.

For the third quarter of 2022, pro forma adjusted EPS is expected to range between $1.23-1.28. For the full year, reported EPS is expected to be $5.73-5.88 while adjusted EPS is estimated to be $5.90-6.05. Pro forma adjusted EPS, excluding currency, is projected to range between $6.09-6.20, representing a YoY increase of 10-12%.

Pro forma adjusted operating income is expected to be flat to up 50 basis points on an organic basis, mainly due to a favorable shift in the product mix from cigarettes to smoke-free products as well as continued investments in the smoke-free portfolio. Gross margin is expected to be lower due to growth in IQOS device volumes, the higher initial cost of IQOS ILUMA devices, higher logistics costs, investments in the smoke-free portfolio, and higher inflation.

Volumes

For full-year 2022, Philip Morris expects pro forma total cigarette and heated tobacco unit shipment volume growth of approx. 1.5-2.5%. Pro forma heated tobacco unit shipment volume is expected to be 90-92 billion units.