Shares of Alaska Air Group Inc. (NYSE: ALK) were up over 1% on Tuesday. The stock has gained 23% year-to-date. The company is scheduled to report its earnings results for the second quarter of 2023 on Tuesday, July 25, before market open. Here’s a look at what to expect from the earnings report:

Revenue

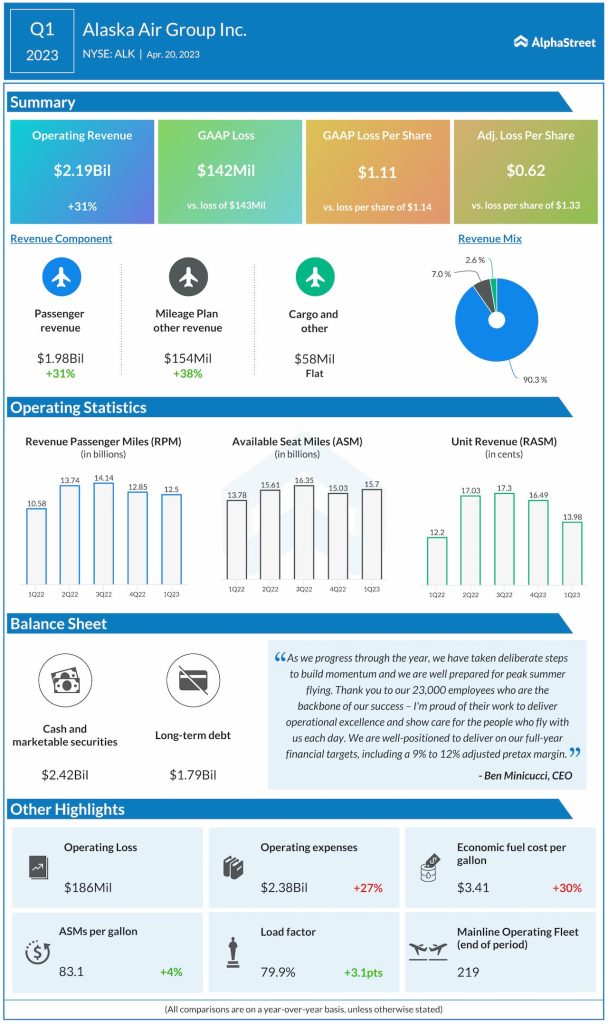

Alaska expects its total revenue for the second quarter of 2023 to be up 2.5-5.5% from the same period last year. Analysts are projecting revenue of $2.77 billion which would represent a growth of 4% from the year-ago period. In Q1 2023, total operating revenue increased 31% year-over-year to $2.19 billion.

Earnings

The consensus estimate is for EPS of $2.68, which compares to EPS of $2.19 in the prior-year period. In Q1, the company reported an adjusted net loss of $0.62 per share.

Points to note

Alaska can be expected to benefit from strong demand for travel. In spite of the loss delivered in the first quarter, the company appears optimistic on improving its performance in the second quarter. Leisure travel remains very strong while business travel continues to pick up. Alaska sees further opportunity for improvement in corporate travel as companies return to office.

In Q1 2023, traffic was up 19% while capacity was up 14% YoY. Load factor came in at 80%. Revenue per available seat mile rose 15% while CASMex was down 1%. Fuel price was $3.41 per gallon. For Q2, Alaska expects fuel price per gallon to come between $2.95-3.15. Capacity is expected to be up 6-9% YoY while CASMex is expected to be up 1-3%.

Alaska can also be expected to benefit from strong premium and loyalty performance. First and Premium Class revenues rose 35% and 33% YoY, respectively, in Q1 on higher paid load factors and fares. Bank cash remuneration also remained strong, increasing 17% YoY in Q1.