Over the years, Alibaba Group Holding Limited (NYSE: BABA) has remained a dominant player in the Chinese tech industry, but it also faced challenges like economic uncertainties and regulatory crackdowns that caused growth to slow down. The tech firm, which is often referred to as China’s Amazon, continues to diversify and invest in the business, on the strength of its healthy balance sheet and cash flows.

This week, Alibaba’s stock opened at $85.34, which almost matches its value a year earlier. In between, it was a rollercoaster ride for the shares, marked by a series of highs and lows. Considering the low valuation and the ongoing e-commerce recovery, it would be a good idea to keep an eye on the stock as it looks poised for a rebound. Analysts covering BABA unanimously recommend buying it, citing the solid growth prospects.

Back on Track

The resurgence of coronavirus infections in various parts of China delayed reopening there, but things are improving fast and the country’s economy has hit the recovery path, thanks to improvements in consumer/business sentiments, easing supply chain issues and manufacturing recovery. Moreover, all the main industries are witnessing fast-paced digital transformation that bodes well for the company.

When AI-based chatbot ChatGPT took the technology sector by storm a few months ago, Alibaba was among the first tech firms to announce a rival product. Earlier this month, the company revealed plans to launch AI-powered chatbot Tongyi Qianwen and integrate it into its products.

“With the lifting of COVID-related measures and off-peak wave, everything is now quickly getting back on track. In general, consumer confidence and business confidence are rising. Logistics has resumed normal operations with the entire supply and manufacturing chains becoming active. Digital transformation across different industries and sectors has accelerated significantly. Against this backdrop, our various businesses are showing positive trends,” said Alibaba’s CEO Daniel Zhang in a recent statement.

Financials

Alibaba will be publishing its fourth-quarter results on May 18, before the market opens. As per analysts’ estimates, revenues increased by 6.6% to $30.21 billion in the final three months of 2023, which is slightly bigger than the growth achieved in the prior quarter. The earnings forecast is $1.35 per share, up 14% from last year.

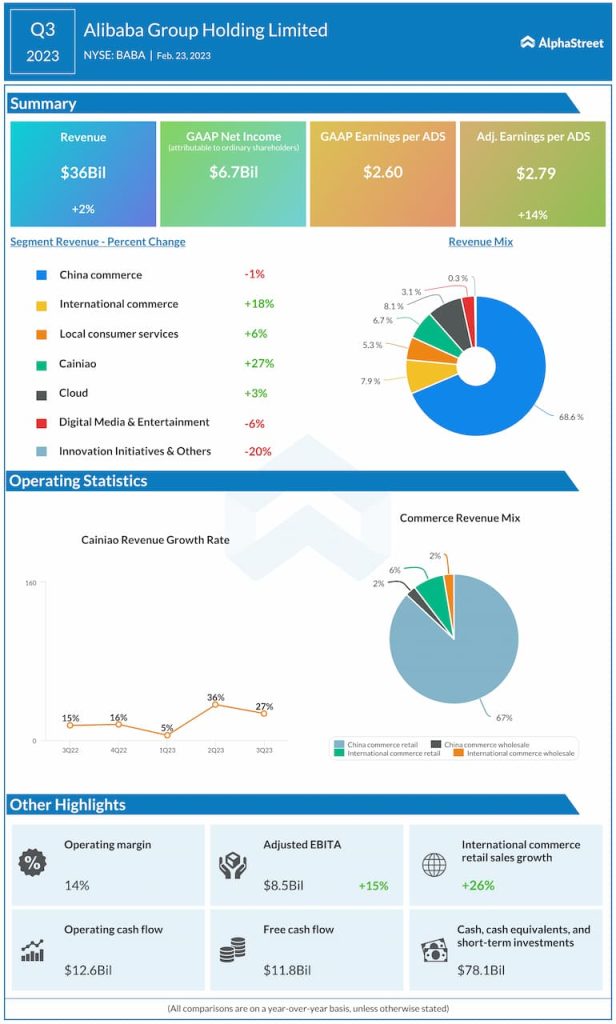

In the third quarter, the top line rose to $36 billion, benefitting from sales growth in the non-core areas of the business, but weakness in the core China Commerce segment restricted the growth rate to 3%. Commerce revenue accounted for about 67% of the total. Earnings per American Depository Shares, on an adjusted basis, increased 14% to $2.79. The operating margin was 14%.

Shrugging off the recent weakness, shares of Alibaba regained a part of their lost strength and moved up in recent sessions. On Monday afternoon, they traded up 3%.