Shares of Dollar General Corporation (NYSE: DG) stayed red on Tuesday. The stock has gained 9% over the past three months. The discount retailer is scheduled to report its earnings results for the second quarter of 2025 on Thursday, August 28, before market open. Here’s a look at what to expect from the earnings report:

Revenue

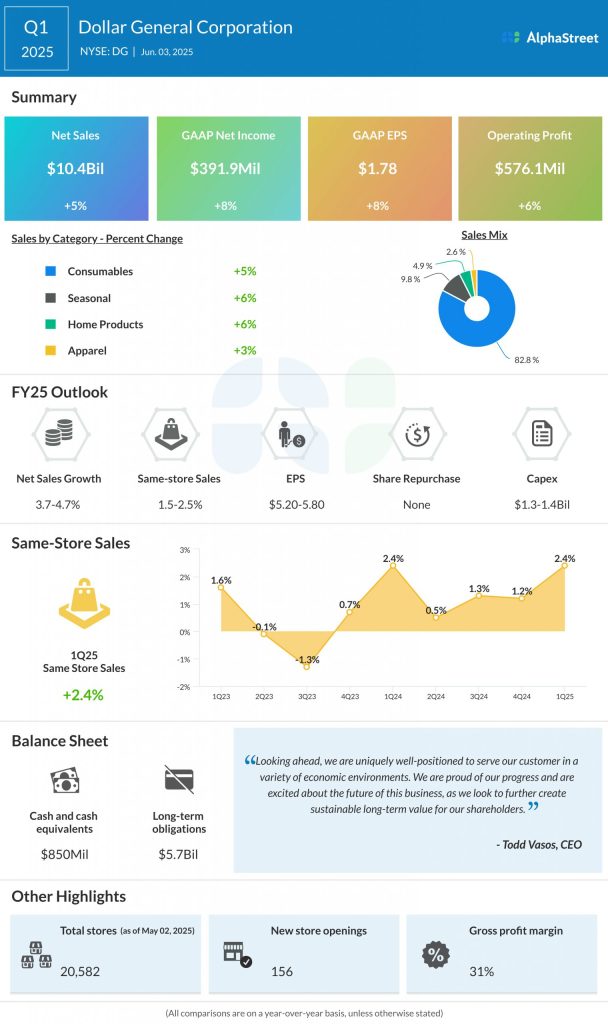

Analysts are projecting revenue of $10.68 billion for Dollar General in the second quarter of 2025, which suggests a growth of over 4% versus the same period a year ago. In the first quarter of 2025, net sales increased 5% year-over-year to $10.4 billion.

Earnings

The consensus target for earnings per share in Q2 2025 is $1.57, which implies a decline of over 7% from the prior-year quarter. In Q1 2025, EPS increased 7.9% YoY to $1.78.

Points to note

Dollar General, as a discount store, is expected to benefit from the trend of consumers looking for value in a dynamic economic environment. The dollar store has seen continued strength in the consumables category and this momentum is expected to continue in the to-be-reported quarter. In addition to the strength in consumables, the company can be expected to benefit from a pickup in non-consumable categories as well.

Although DG’s core customer might be financially constrained, it has been gaining business from middle and higher-income customers which is a benefit. This provides opportunity for further share gains.

Dollar General is expected to benefit from the investments in its store base, both in new stores and store remodels. Its current remodel programs, Project Renovate and Project Elevate, are progressing well and while these remodels cost significantly less than new stores, they are also anticipated to deliver better returns than new stores. It is also seeing strong performance from its pOpshelf stores.

DG’s efforts to improve its digital capabilities are also expected to yield benefits. It is making progress with its mobile app, website, and delivery options. Its vast store footprint is an advantage in its delivery efforts and provides opportunity for meaningful growth.