Shares of Lamb Weston Holdings, Inc. (NYSE: LW) stayed red on Friday. The stock has dropped 21% over the past three months. The frozen potato products supplier is slated to report its first quarter 2025 earnings results on Tuesday, October 1, after markets close. Here’s a look at what to expect from the earnings report:

Revenue

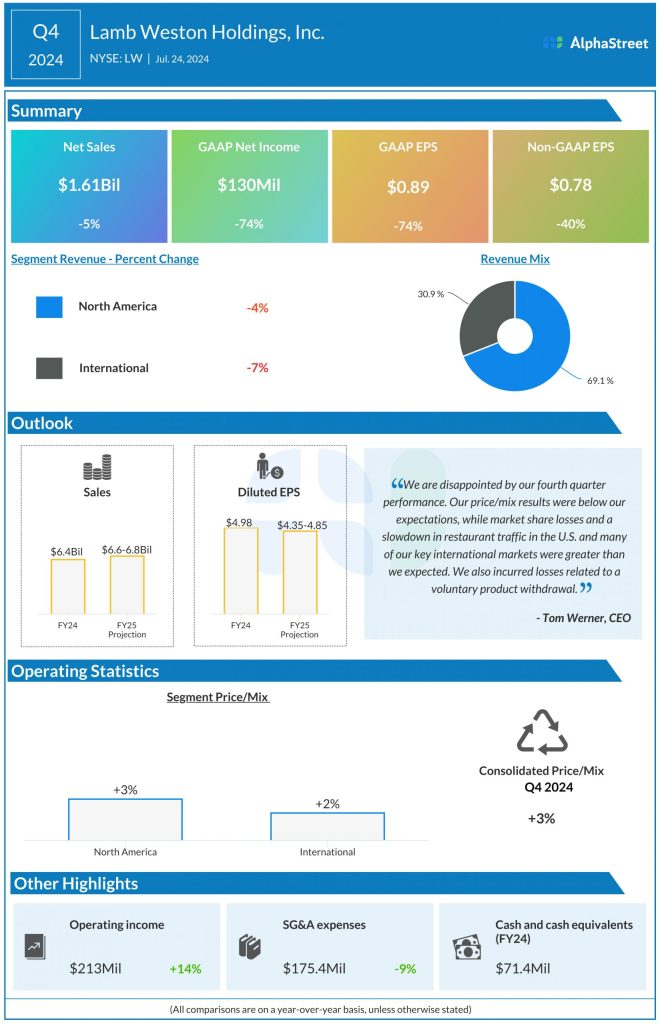

Lamb Weston forecasts sales for the first quarter of 2025 to be down mid-to-high single digits compared to the same period a year ago. Analysts are estimating sales of $1.56 billion for the quarter, which compares to sales of $1.66 billion reported in the year-ago period. In the fourth quarter of 2024, net sales declined 5% year-over-year to $1.61 billion.

Earnings

The consensus estimate for EPS in Q1 2025 is $0.71. This compares to adjusted EPS of $1.63 reported in Q1 2024. In Q4 2024, adjusted EPS fell 40% YoY to $0.78.

Points to note

Lamb Weston has been navigating a challenging environment as menu price inflation has led to softness in global restaurant traffic and frozen potato demand. This has led to an increase in available capacity in North America and Europe. This supply-demand imbalance is expected to continue through the most part of fiscal year 2025.

Lamb Weston’s volume fell 8% in Q4 2024, mainly due to market share losses, the exit from certain lower-price and lower-margin business in Europe, soft restaurant traffic trends in North America and key international markets, and a voluntary product withdrawal. Sales and volumes declined across the North America and International segments as well.

LW expects the operating environment to remain pressured in fiscal year 2025 by economic headwinds. The company anticipates volumes to decline during the first half of the year due to continued impacts from share losses and softness in restaurant traffic as consumers adjust to higher menu prices.

The French fry-maker expects volumes to pick up in the second half of the year as it laps the impacts of the ERP transition and voluntary product withdrawal from last year. Volume improvement is expected to be supported by customer contract wins in the US and international markets, and the regaining of some lost market share.

In Q1 2025, Lamb Weston expects volume to be down mid-single digits, impacted by share losses, soft restaurant traffic, and the voluntary product withdrawal. The first quarter is expected to record the highest impact from share losses and soft traffic, after which it will begin to ease going through the rest of the year.

Price/mix is anticipated to be down low-to-mid-single digits as the benefit from pricing is offset by the impact of unfavorable mix and targeted investments in price and trade support in North America. Margins in Q1 are expected to be pressured by higher cost per pound, unfavorable mix, and investments in price and trade support.