Southwest Airlines Co. (NYSE: LUV) is slated to report third quarter 2019 earnings results on Thursday, October 24, before the market opens. Analysts estimate the company will report earnings of $1.08 per share which is flat compared to the prior-year period. Revenue is expected to inch up by 1% to $5.64 billion.

Like its peers, Southwest’s third quarter results will be impacted by the 737 Max groundings. The airline is tackling higher costs and lower capacity due to the groundings. However, strong customer demand and a higher passenger yield will help provide a cushion.

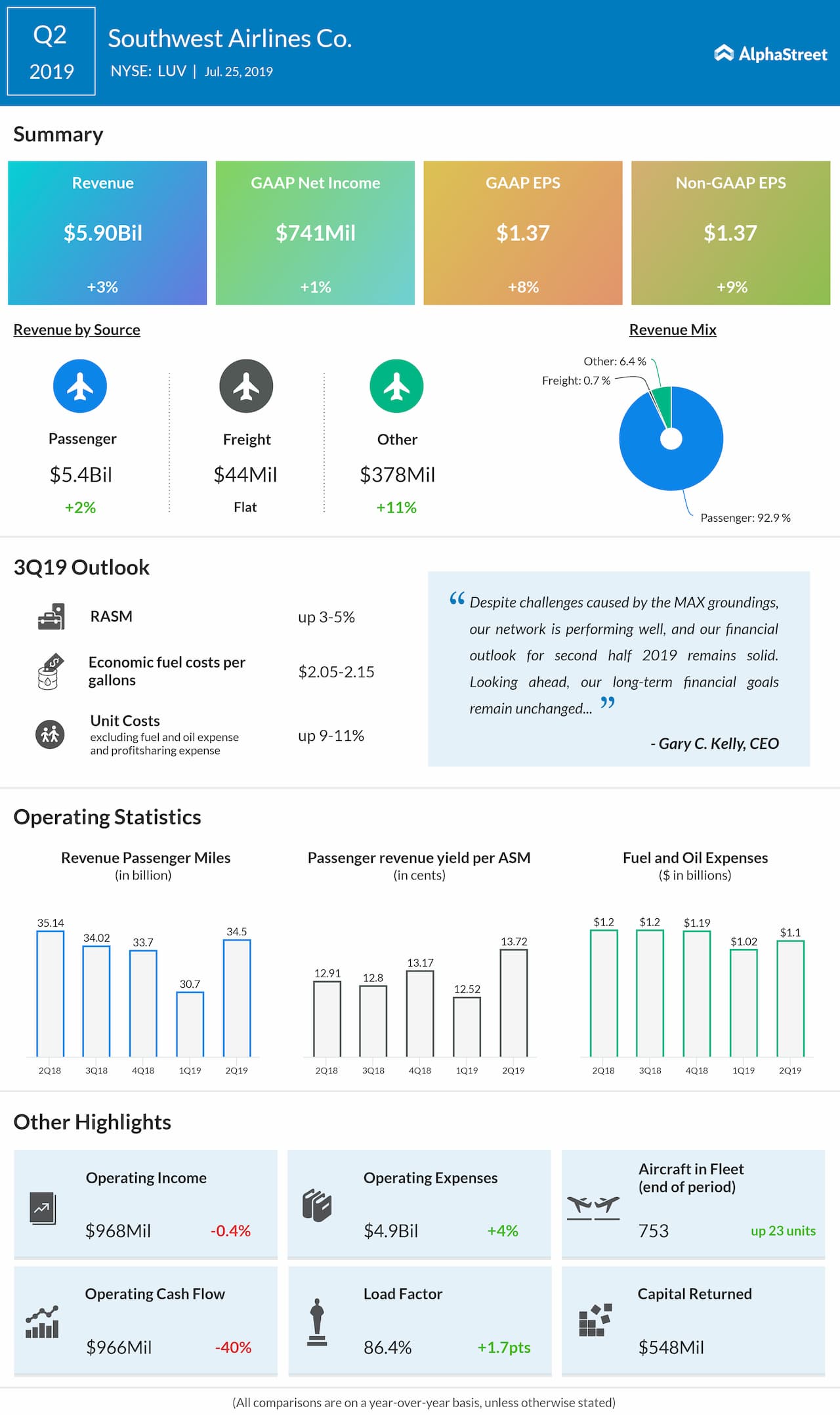

Last quarter, Southwest saw a 6.8% increase in unit revenues, and the company expects strong unit revenue growth in the third quarter. The company will also benefit from lower fuel costs. Unit revenues are expected to increase 3-5% in the third quarter while unit costs, excluding fuel, are projected to rise 9-11%.

Capacity is expected to drop 2-3% and fuel efficiency is expected to decrease 1-2% year-over-year due to the Max groundings in the third quarter. Economic fuel costs are estimated to be $2.05-2.15 per gallon.

In the second quarter of 2019, Southwest beat earnings estimates but missed the mark on revenue. Revenues rose 3% to $5.90 billion but was below the estimated $5.94 billion. Adjusted EPS grew 9% to $1.37. Capacity dropped 3.6% while unit costs increased 7.5%.

For the full year of 2019, Southwest expects unit costs (CASM), excluding fuel, oil and profit-sharing expenses, to increase 8-10% year-over-year. Capacity is estimated to drop 1-2%.

Shares of Southwest have gained 12% year-to-date. The stock was down 1% in afternoon trade on Tuesday.