Shares of Home Depot (NYSE: HD) have gained 13% over the past 12 months. The home improvement retailer is scheduled to report its earnings results for the fourth quarter of 2024 on Tuesday, February 25, before market open. Here’s a look at what to expect from the earnings report:

Revenue

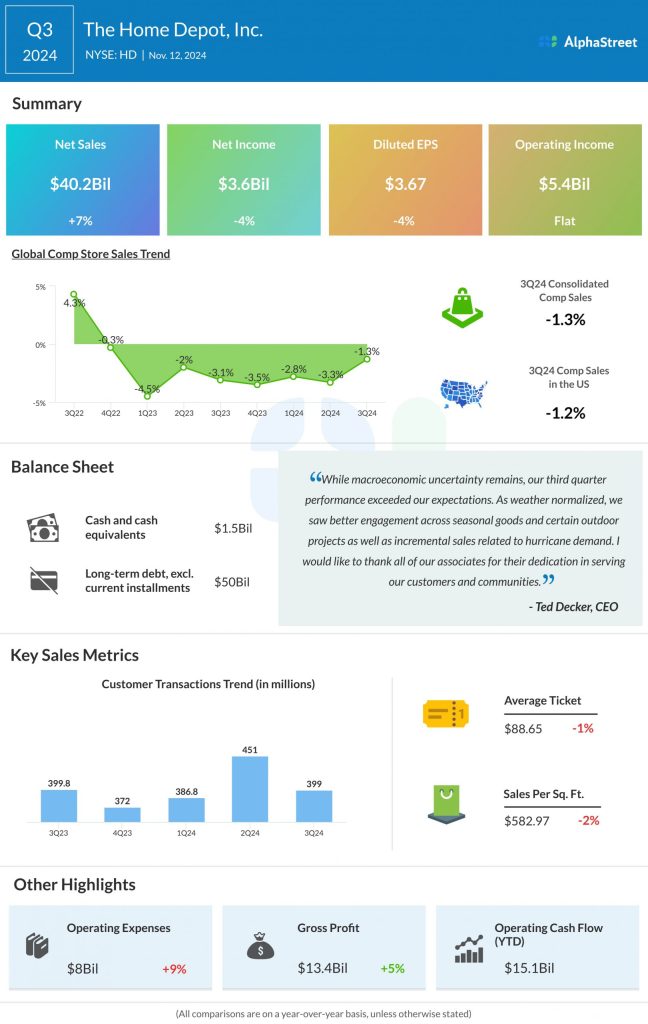

Analysts are projecting revenue of $38.8 billion for the fourth quarter of 2024, which indicates a growth of over 11% from the same period a year ago. In the third quarter of 2024, sales increased nearly 7% year-over-year to $40.2 billion.

Earnings

The consensus estimate for Q4 2024 earnings per share is $3.02, which compares to EPS of $2.82 reported in Q4 2023. In Q3 2024, EPS fell 4% year-over-year to $3.67.

Points to note

Last quarter, Home Depot’s sales benefited from favorable weather, which drove engagement across seasonal goods and outdoor projects. It also saw incremental sales from hurricanes. The company anticipates hurricane-related demand to continue in the fourth quarter. This demand is expected to reflect in the top line.

At the same time, larger remodeling projects may continue to face pressure from higher interest rates and macroeconomic uncertainty. In Q3, comp transactions were down 0.6% while comp average ticket was down 0.8%. Big-ticket comp transactions, which are ones over $1,000, were down 6.8% YoY. Larger discretionary projects, such as kitchen and bath remodels, witnessed softer engagement.

Home Depot continues to see strength in its Pro customer segment. Last quarter, Pro sales were positive and outpaced the do-it-yourself, or DIY customer. The company’s investments in its Pro Ecosystem, which is now in 17 US markets, are expected to continue yielding benefits. The acquisition of SRS, which gives access to the specialty trade Pro customer, provides cross-sale opportunities and competitive advantages.

The company’s continued investments in its stores, product assortment, and digital capabilities are also expected to yield benefits.